The defence pivot: Decoding Singhania’s high-conviction bets

Sunil Singhania, the founder of Abakkus Asset Manager Pvt Ltd and one of India’s most tracked super investors, is doubling down on India’s defence narrative. As India targets a Rs 50,000 cr export milestone by 2029, Singhania’s portfolio reveals a strategic concentration in two specific players.

After following Singhania’s portfolio and his moves for the past few years now, I could say that he is not one to make decisions on the fly and this inclination towards the defence sector is possibly a deeply researched one.

First is a long-term core holding partnering defence majors like HAL and BEL along with some global aerospace heavyweights, while the second is a fresh small-cap entry riding the naval indigenization wave.

Let us dive into these two stocks to try and find out what is it that could have caught Singhania’s attention.

Dynamatic Technologies: From precision parts to Tier-1 aerospace major

Incorporated in 1973, Dynamatic Technologies Ltd (DTL) is engaged in the manufacturing of hydraulic gear pumps and automotive turbochargers. They serve clients across Aerospace, automotive and hydraulic industries.

With a market cap of Rs 6,988 cr, the company has transitioned from being a precision component supplier to a Tier-1 strategic partner for the world’s largest aerospace and defence OEMs. Its defence connections are deep, spanning from indigenous fighter jets to global stealth and transport platforms.

Sunil Singhania, through the Abakkus Funds, has held a stake in the company since filing for the quarter ending September 2021. Currently holds a 2.9% stake in the company worth Rs 204 cr, making it one of the biggest holdings in the company.

But what is catching the attention of investors like Singhania is probably the fact that the company is one of the few private Indian companies integrated into the inner circle of global defence and aerospace manufacturing.

Dynamatic is in an exclusive partnership with the L&T-Bharat Electronics Ltd (BEL) consortium for India’s Advanced Medium Combat Aircraft (AMCA) program. DTL is the exclusive partner for complex aerostructures and sub-systems for this prestigious 5th-generation stealth fighter.

The company also has a long-term MoU with Hindustan Aeronautics Limited (HAL) for the manufacturing of the front fuselage for the LCA Tejas Mk1A and Mk2. They are scaling production to deliver assemblies for over 20 aircraft per year.

Plus, Dynamatic has also collaborated with BEL to indigenize the Vertical Launch Unit (VLU) for the LRSAM (Long Range Surface-to-Air Missile) program.

No wonder the company has held Singhania’s attention and investments for over 5 years now.

However, when it comes to financials, the company has seen a rocky terrain in the last few years.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | 5-Year CAGR |

| Sales/Rs Cr | 1,230 | 1,118 | 1,253 | 1,316 | 1,429 | 1,404 | 3% |

| EBITDA/Rs Cr | 159 | 127 | 172 | 184 | 162 | 160 | 0.2% |

| Profits/Rs Cr | 39 | -22 | 15 | 43 | 122 | 43 | 2% |

As we can see, the company saw a huge drop in FY25, after seeing good growth in the preceding years.

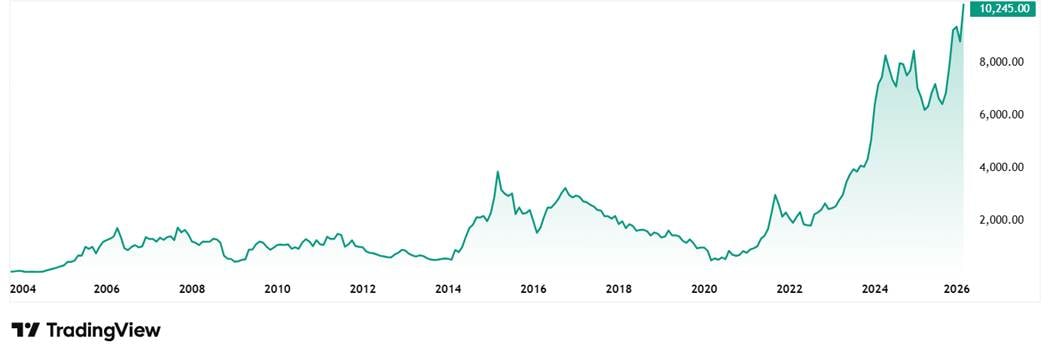

The share price of Dynamatic Technologies Ltd was around Rs 901 in February 2021 and as on 23rd February 2026 it was Rs 10,290, which is a 1,042% jump in 5 years. Rs 1 lakh invested in the company 5 years ago would have been close to Rs 11.5 lakhs today.

The stock is currently trading at a PE of a big 149x, and the current industry PE is 29x, which tells us that the market believes Dynamatic is no longer a Hydraulics & Pump company; it is being valued as a Defence Tech company.

In what could be a big signal of its intent to play a larger role in Ministry of Defence (MoD) procurement and strategic programs, Dynamatic in December 2025, appointed retired Air Chief Marshal V.R. Chaudhari, who is the former Chief of the Air Staff, to its board.

The company is also moving into prime contractor territory with its own IP. It has developed indigenous drones named Cheel, Kaatil, and Patang. These are being positioned for the Indian Armed Forces under the “Make in India” initiative, focusing on agility and affordability.

Dynamatic is also currently executing an order for 8 Vertical Launch Units for the Navy, with deliveries which began in August 2025. Plus, it is working on comprehensive Border Management & Physical Security Systems, leveraging its hydraulics and security divisions.

DCM Shriram: A legacy player’s pivot to armored vehicles & UAV

Carrying the legacy of the original Delhi Cloth & General Mills Co. Ltd. (DCM), which was founded in 1889, DCM Shriram Industries Ltd was Incorporated in 1989.

With a current market cap of Rs 479 cr, the company has aggressively pivoted from its traditional sugar and chemical roots to become a serious contender in the “Make in India” defence ecosystem, through its specialized divisions, DCM Shriram Defence and DCM Shriram International.

DCM Shriram is one of the few private Indian players with a full industrial license to manufacture armoured vehicles. It manufactures ZEBU Carmel & Carmel Lite, indigenous Light Bullet Proof Vehicles (LBPV) designed for high-intensity counter-insurgency and border operations. These vehicles are built to withstand 7.62mm SLR, AK-47 fire, and hand grenade blasts.

The company has also developed a robust Drone Stack with indigenous flight controllers and airframes, moving away from Chinese components. It operates a dedicated line for these UAVs, positioning itself for the Indian Army’s massive upcoming Drone Fed requirements.

Singhania just bought a 2.9% stake in the company worth Rs 16 cr as per the filings for the quarter ending December 2025.

Let us look at the financials of the company to see, what could have caught Singhania’s attention.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | 5-Year CAGR |

| Sales/Rs Cr | 1,795 | 1,943 | 2,123 | 2,351 | 2,083 | 2,052 | 3% |

| EBITDA/Rs Cr | 147 | 151 | 142 | 142 | 224 | 199 | 6% |

| Profits/Rs Cr | 96 | 65 | 66 | 60 | 115 | 101 | 1% |

The decline in the figures for FY25 could be due to a drop in Rayon/Fibre segment volumes. Also, the entity split into three separate companies (DCM Shriram Industries, DCM Shriram Fine Chemicals, and DCM Shriram International) which often leads to one-time professional fees and a temporary diversion of management focus from core operational efficiency.

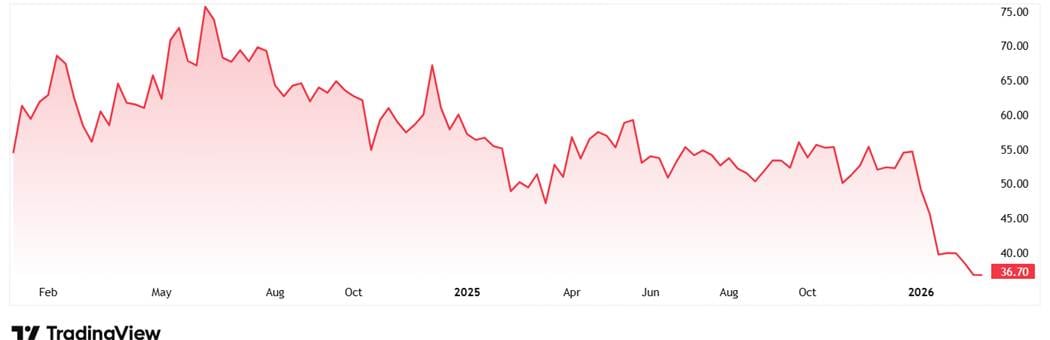

The share price of DCM Shriram Industries Ltd was around Rs 55 in January 2024 after company was listed individually post demerger and as on 23rd February 2026 it was Rs 37. So, the stock has seen a correction since the demerger.

The company’s share is trading at a current PE of 8x, and the industry median is 11x. The 10-year median PE for the company is 4x while the industry median for the same period is 10x.

One red flag is the post-demerger family control tightening. In December 2025, Two Independent Directors, Meenakshi Behara, Suman Jyoti Khaitan resigned pursuant to the reconstitution of the board, as part of the implementation of the Sanctioned Scheme of Arrangement. On the same day Sr MD & CEO Alok B. Shriram and WTD Urvashi Tilakdhar also resigned.

Sons Uday Shriram (Dy MD) and Rohan Shriram (WTD) were then inducted and their father, Madhav B. Shriram was redesignated MD & CEO with salary hike to Rs 7.5 lakhs per month + 5% Profit Before Tax commission.

The Singhania playbook: Is it time to mirror the ‘smart money’ in defence?

When an investor like Sunil Singhania places big bets in Defence, the market takes notice. While Dynamatic Technologies represents a high-premium bet on global aerospace and Defence integration and Tier-1 status, DCM Shriram Industries offers a value-oriented play on a legacy company’s pivot toward armored mobility and UAVs.

Together, these picks signal a move away from simple component manufacturing toward high-IP ownership within the “Make in India” framework. But both companies face distinct hurdles that calls for a scrutiny.

Dynamatic’s staggering 149x P/E ratio suggests the market has already priced in several years of flawless execution, leaving very little margin for the rocky terrain seen in its recent EBITDA and profit margins.

On the other hand, DCM Shriram’s attractive valuation is shadowed by the recent exodus of independent directors and the tightening of family control following its demerger.

As India moves towards its target of Rs 50,000 cr defence export by 2029, how these two stocks fare in the long and short term will be an interesting ride to watch. A good idea would be to add these stocks to watchlist and keep a vigilant eye on them.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.