")

For most investors, BLS International is a simple story. More people travel abroad, more visa applications get processed and the company earns more money. Fewer people travel and growth slows.

That explanation worked for years. It may not work anymore.

While visa processing remains its largest business, BLS has quietly built a second engine through digital public services. Aadhaar enrolment, banking correspondent services, financial distribution and citizen services now contribute a meaningful share of revenue. In Financial Year 2026 (FY26), the business more than doubled, helping the company deliver record revenue of Rs 2,998 crore and record Profit After Tax (PAT) of Rs 724 crore.

BLS International 1-Year Share Price Chart

More than a visa outsourcing company

BLS International is among the world’s largest providers of visa and consular services. Governments outsource activities such as accepting visa applications, collecting biometric information, verifying documents and managing visa application centres, allowing them to focus on the actual decision of whether to grant a visa.

Over the years, the company has expanded well beyond that niche. Today, it also offers digital citizen services, banking correspondent services, Aadhaar enrolment, assisted e-governance and financial distribution. The expansion reflects a broader trend, with governments increasingly outsourcing routine public-facing services instead of building these capabilities internally.

Offering End-to-End Visa & Consular Services

The shift is already visible in the numbers. The Visa and Consular Services business contributed Rs 1,840 crore in revenue in FY26, while Digital Services generated Rs 1,158 crore, up 114.4% year-on-year from Rs 540 crore. That means nearly two-fifths of BLS’ revenue now comes from businesses unrelated to visa processing, giving the company a broader growth base than many investors may realise.

The numbers support the changing story

BLS reported consolidated revenue of Rs 2,998 crore in FY26, up 36.7% from Rs 2,193 crore a year earlier. Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA) stood at Rs 819 crore, translating into a margin of 27.3%, while Profit After Tax (PAT) increased to Rs 724 crore with a margin of 24.1%.

Management attributed the strong performance to higher visa application volumes, improved revenue per application, multiple contract wins and the consolidation of Aadifidelis. While the company’s overall EBITDA margin moderated from 28.7% in FY25 to 27.3% in FY26 because of the changing business mix, the Visa and Consular Services segment continued to improve profitability, with segment EBITDA margin expanding to 40.1% from 34.5% a year earlier.

The March quarter reflected a similar trend. Revenue increased 17.6% year-on-year to Rs 815 crore, while EBITDA margin remained largely stable at 25% and PAT margin improved to 22.9% from 21% in the corresponding quarter last year. Despite geopolitical uncertainty affecting international travel, the company continued to report healthy profitability.

The visa business is still doing the heavy lifting

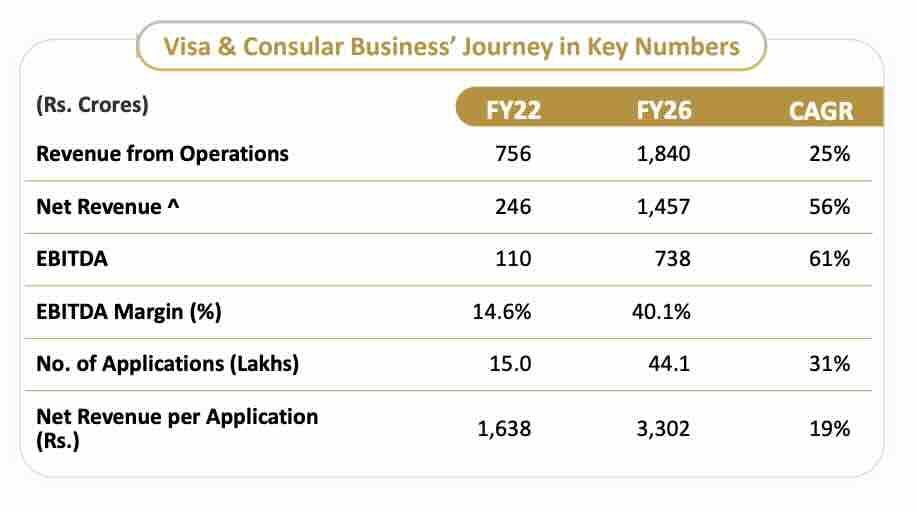

Diversification may be the bigger story, but the traditional visa business continues to be BLS’ biggest earnings driver. Revenue from Visa and Consular Services increased 11.3% to Rs 1,840 crore during FY26.

More importantly, segment EBITDA climbed nearly 30% to Rs 738 crore, with margins improving to 40.1% from 34.5% in FY25. The improvement was driven by more than just higher travel demand.

Visa applications increased to 44.1 lakh from 37.5 lakh, while net revenue earned per application rose to Rs 3,302 from Rs 2,903. Management attributed this to stronger pricing in recently won contracts and higher adoption of value-added services by applicants.

Source: Company Presentation

That is encouraging because it suggests earnings growth is coming not only from processing more applications but also from earning more on each application.

A second growth engine is gathering pace

The biggest change during FY26 came from the Digital Services business.

Revenue from the segment more than doubled to Rs 1,158 crore from Rs 540 crore in FY25. Growth was supported by the Aadifidelis acquisition, banking correspondent services, loan distribution and assisted digital services.

The digital business operates with lower margins than visa outsourcing. Even so, it broadens BLS’ addressable market and reduces dependence on international travel cycles. As this business grows, investors will closely watch whether scale benefits can offset the lower profitability and support consolidated margins.

Winning contracts remains critical

Unlike a manufacturing company, BLS does not need to build large factories before it grows. Its growth depends on winning and renewing government contracts.

The company added several important contracts during FY26. These included a Rs 2,055 crore order from the Unique Identification Authority of India (UIDAI) for Aadhaar Seva Kendras, a three-year contract from the Ministry of External Affairs to operate Indian Visa Application Centres in China, a five-year global visa outsourcing contract from Slovakia and visa outsourcing mandates from Cyprus across multiple countries.

It also secured a Bihar government project for Permanent Enrolment Centres and renewed its attestation and apostille services contract with the Ministry of External Affairs.

Management indicated that the UIDAI project is still in its initial rollout phase. More than 200 centres are expected to be established over the next one to one-and-a-half years, meaning the full revenue benefit will come gradually rather than immediately.

For FY27, management refrained from giving numerical guidance. Instead, it said the company continues to bid for multiple domestic and international tenders, while many governments are outsourcing visa services for the first time. That provides a healthy opportunity pipeline, although contract wins remain inherently uncertain.

A strong balance sheet provides flexibility

One of BLS’ biggest strengths is its balance sheet.

Net cash increased to Rs 1,434 crore as of March 31, 2026, from Rs 928 crore a year earlier. The company also generated operating cash flow of Rs 903 crore during FY26, giving it ample financial flexibility for acquisitions, technology investments and expansion.

Debt remains modest with a debt-to-equity ratio of 0.17, leaving little immediate concern about leverage.

High returns continue

The company’s profitability is reflected in its return ratios.

According to Screener.in, Return on Equity (ROE) stands at 32.7% and Return on Capital Employed (ROCE) at 29.3%. These are among the strongest return ratios in the listed business services space and indicate that the company continues to generate healthy profits without relying heavily on debt.

The board also recommended a final dividend of Rs 0.50 per share in addition to the interim dividend already paid during FY26, taking the total dividend payout for the year to more than Rs 100 crore.

Risks remain

The transformation story is promising, but investors should not ignore the risks.

The business continues to depend heavily on winning and renewing government contracts. Competitive bidding can pressure pricing, while delays in tender awards may affect growth.

Visa processing also remains exposed to geopolitical developments and international travel demand. Management acknowledged that conflicts can temporarily reduce travel volumes, although it believes the impact usually evens out over longer periods because of the company’s diversified geographic presence.

Another monitorable is the Digital Services business. Although it is growing rapidly, its margins remain well below those of the visa business. If digital services become a larger part of revenue, investors will watch whether consolidated profitability remains resilient.

Finally, the pace of the UIDAI rollout and the successful integration of Aadifidelis will determine how quickly these newer businesses begin contributing meaningfully to earnings.

Valuation

At the current market price of around Rs 240, BLS International trades at a Price-to-Earnings (P/E) multiple of about 14.4 times. That is well below its five-year average of around 36.8 times.

The discount suggests investors remain cautious about whether recent growth can be sustained. A steady flow of contract wins, successful scaling of digital services and continued improvement in margins could determine whether the market eventually assigns the company a higher valuation.

The bottom line

For years, BLS International’s fortunes were closely tied to global travel. That relationship still matters, but it no longer tells the entire story.

The company is gradually building a broader government services platform that combines a highly profitable visa outsourcing business with faster-growing digital public services. If it can continue winning contracts, scale its newer businesses without sacrificing profitability and maintain its strong balance sheet, BLS may eventually be valued less like a travel-linked outsourcing company and more like a diversified public services platform. That is the shift investors should watch through FY27.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Manvi Aggarwal has been tracking the stock markets for nearly two decades. She spent about eight years as a financial analyst at a value-style fund, managing money for international investors. That’s where she honed her expertise in deep-dive research, looking beyond the obvious to spot value where others didn’t. Now, she brings that same sharp eye to uncovering overlooked and misunderstood investment opportunities in Indian equities. As a columnist for LiveMint and Equitymaster, she breaks down complex financial trends into actionable insights for investors.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article. The website managers, its employee(s) and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.