As digital infrastructure scales rapidly, data centres are emerging as a multi-layered capex cycle. A McKinsey analysis finds that global data centre infrastructure spending is expected to exceed US$ 1.7 trillion (₹158 lakh crore) by 2030, driven by demand for Artificial Intelligence, cloud, and high-performance computing.

This expansion is not linear. Data centre campuses are now evolving from tens of megawatts to gigawatt-scale facilities, significantly increasing their energy and infrastructure intensity. This translates into a structural opportunity across power equipment, pipes, and high-voltage components, where each incremental capacity addition triggers parallel demand.

Against this backdrop, this article discusses three companies that supply critical components across the data centre value chain.

#1 Pitti Engineering Holds 90% Market Share in Data Center Components

Pitti Engineering is one of India’s largest manufacturers and exporters of electrical laminations, as well as a manufacturer of machined castings and fabricated components. A key differentiator for the company is its deep vertical integration. The company handles everything from tooling and lamination assemblies to machined castings and fabrication.

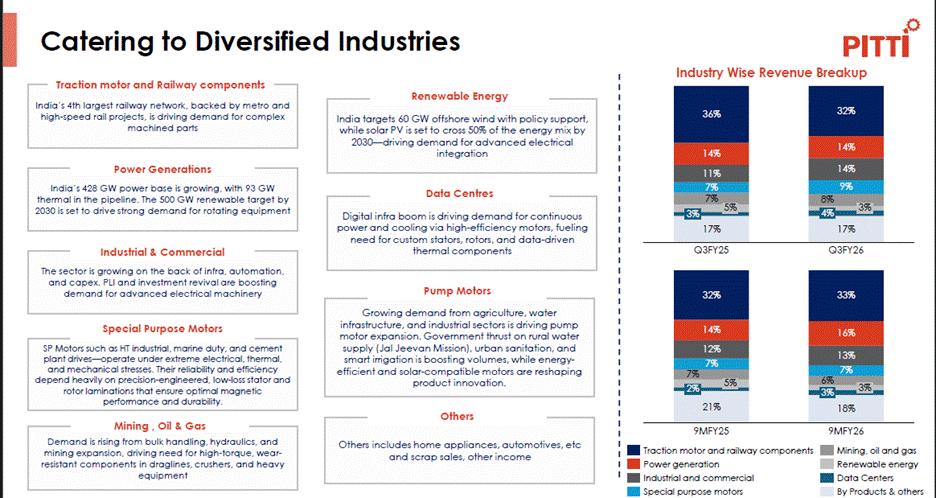

A Dominant Moat in the Data Center Supply Chain

The data center segment is an extremely fast-growing market for Pitti Engineering, driven by the global boom in digital infrastructure. The critical need for continuous power and cooling via high-efficiency motors is driving demand for Pitti’s custom stators, rotors, and data-driven thermal components.

The Cummins Connection: 90% Market Share

The company’s key customer in this space is Cummins Generator Technologies. Pitti commands a dominant market position, holding an estimated 90%-plus market share for these specific products with this customer. These units have an average sale value of ₹4.5-5 lakh per unit. Its customer takes around 45-60 days to convert these parts into a fully assembled generator.

The 3% Data Center Revenue-Share

Additionally, parts for the European and US data center markets are mostly supplied through the customer’s operations within India. The segment has shown encouraging momentum, with its contribution to Pitti’s revenue increasing from 2% in 9MFY25 to 3% in 9MFY26. Pitti realised around ₹18 crore in revenue from the segment in Q3.

Revenue-Mix

Vertical Integration: Scaling to ₹120 Crore Revenue

Management is highly confident in the data center segment’s potential to outpace the broader industry’s growth over the medium term. Over the next 12-18 months, Pitti forecasts robust growth of 25-30% in this vertical, with annual revenue of ₹100-120 crore at the upper end of the estimates. This would entail supplying an average of about 150 units per month.

9MFY26 Financial Performance: Margins Expand by 110 Bps

From a financial standpoint, revenue increased 14.2% year-on-year to ₹1,412 crore in 9MFY26. EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) increased 22.4% to ₹234 crore, with margin rising by 110 bps to 16.6%. Net Profit increased by 5.9% to ₹91.2 crore.

Pitti 1-Year Share Price Trend

#2 Yash Highvoltage Supplies Bushings to Global Grids

Yash Highvoltage designs and produces a highly critical, niche component for the global power sector: transformer bushings. A transformer bushing serves as a critical, insulated gateway that safely facilitates the flow of high-voltage and high-current electricity into and out of a power transformer.

It supplies bushings to the transmission and generation sector, including utilities, original equipment manufacturers (OEMs), renewable energy projects, and data centers.Since data centers require an uninterrupted power supply, it is imperative that they be rigorously tested, deemed reliable, and formally approved for use by the end user.

Global Grid Upgrades: Targeting a ₹16,000-Crore Addressable Market

Furthermore, it cannot be easily replaced. This expansion of data centers is a primary driver of the rapid increase in energy demand. This is creating stress on existing power transmission and distribution infrastructure worldwide. As a result, global electrical grids must be upgraded and expanded.

This translates into long-term demand for power transformers and their critical connection components, such as high-voltage transformer bushings. In fact, Yash is targeting data centers as key end-customers within its broader global expansion strategy.

To capitalize on this opportunity, Yash adopts a two-pronged market strategy. It does not rely solely on EMs that manufacture transformers, or on consultants who design electrical systems. Instead, it secures approvals for its products from data centers and solar power operators.

Through this, Yash ensures that its products are incorporated into and utilized within the infrastructure projects being built. Yash is aggressively expanding its manufacturing capabilities. Yash is establishing a new greenfield facility to produce bushings up to 550 kV and expanding capacity at its existing plant.

Its current product line addresses a market of about ₹10,000-₹12,000 crore. The new 550 kV facility will expand the total addressable market to at least ₹15,000-16,000 crore, positioning them perfectly to support the high-voltage transformers needed for data centers globally.

The US Strategy: Yash HV USA Inc. and Direct Customer Engagement

Yash Highvoltage has also launched a dedicated sales and marketing office, Yash HV USA Inc., in the US. This strategic expansion brings it closer to one of the world’s largest data center and power markets, allowing it to directly engage with American customers. The company’s financial growth is also strong.

H1FY26 Financial Audit: 110% EBITDA Growth and Revenue Visibility

Revenue increased 78.6% year-on-year to ₹102 crore in H1FY26, driven by the order book execution. EBITDA increased 110% to ₹23 crore, with margin rising by 341 bps to 22.8%. Net Profit increased by 119.4% to ₹14 crore. As of H1FY26, Yash’s order book stood at over ₹300 crore, providing revenue visibility for the next 1.5 years. Yash reports half-yearly financials.

Yash Highvoltage 1-Yr Share Price Trend

#3 Welspun Corp is Winning the US gas pipeline Race

Welspun Corp manufactures a wide variety of pipes, steel products, and water storage solutions. Operating major manufacturing hubs in India, the US, and Saudi Arabia, Welspun supplies critical materials for the energy, infrastructure, and real estate sectors.

The AI Power Link: Why Data Centers Need Dedicated Gas Pipelines

A surge in the construction of AI data centers increases demand for energy infrastructure. Because data centers consume massive amounts of electricity, each facility requires its own dedicated power plant to ensure an uninterrupted power supply.

These dedicated power plants, in turn, rely on natural gas, creating an urgent and massive demand for new natural gas pipelines. Against this backdrop, pipe manufacturers like Welspun Corp are now operating directly within the value chain of the booming AI data center industry.

US Market Expansion: 9,000 Miles of Infrastructure Growth

In the US, the business environment is currently highly bullish. Midstream firms are planning or actively building approximately 9,000 miles of pipelines to meet the power demands driven by both these data centers and LNG exports.

About 8 to 9 major pipeline projects are being actively discussed or slated for construction to support these energy needs. Furthermore, pipelines constructed specifically for AI data centers require heavy-wall-thickness pipes, which is driving demand for specialized LSAW (Longitudinal Submerged Arc Welded) products.

The demand is evident from Welspun’s existing spiral mill in Little Rock, which is fully booked until FY28. Management expects this mill to operate at 85% to 90% capacity utilization. To capture more of this market, it is upgrading its ERW capabilities to a 24-inch mill and bringing a new LSAW mill online by the end of the year.

The opportunities presented by data centers are also materializing in India. Management views initiatives regarding nuclear energy for data centers as a major growth catalyst for the domestic market. This is expected to open up several new avenues for the Welspun Specialty Solutions division, which supplies high-quality seamless steel pipes and tubes.

Q3FY26 Financial Audit: Adjusted PAT Jumps 52.5% Amid Record Order Book

Revenue increased 25% year-on-year to ₹4,532 crore in Q3FY26, driven by the execution of a robust order book. EBITDA increased 35% to a record-high level of ₹645 crore. Adjusted net profit (excluding an exceptional gain of ₹378 crore in Q3FY25) grew 52.5% to ₹453 crore. Order book stood at a record high of ₹23,600 crore, providing clear revenue visibility for over a year.

Welspun Corp 1-Yr Share Price Trend

Sector Comparison: Efficiency vs. Valuation

Yash Highvoltage’s return ratios (Return on Capital Employed and Return on Equity) are the strongest among all three, followed by Welspun Corp and Pitti. In terms of valuation, Pitti is trading at a discount to its historical and industry median multiples. Welspun is trading at a discount to its industry multiples, yet remains in line with its historical median.

Yash continues to trade at a premium compared to its peers.

| Valuation Comparison (X) | |||||

| Company | P/E | 5Y Median P/E | Industry Median P/E | RoCE (%) | RoE (%) |

| Pitti | 22.7 | 24.4 | 27.3 | 17.0 | 17.8 |

| Yash Highvoltage | 43.8 | 42.3 | 24.3 | 28.5 | 22.6 |

| Welspun Corp | 14.9 | 14.3 | 18.7 | 21.2 | 18.6 |

The data centre opportunity extends well beyond digital infrastructure into power, cooling, and transmission ecosystems. As capacity scales to gigawatt levels, demand for electrical equipment, pipes, and high-voltage components will accelerate. Companies positioned in these layers stand to benefit, though execution will remain key.

It’s worth keeping these stocks in your watchlist.

Disclaimer

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.