")

There’s a popular saying in the market: ‘Bull markets climb a wall of worry’. This is absolutely true. The 2,600+ points Sensex rally today is a reminder of the market’s ability to ignore all the negatives that might be thrown its way.

You see, only a massive change in sentiment can derail the momentum in the market. Not even the war could keep the markets down for so long and the markets are back on track to their recovery mode.

This is because the Indian stock market, which used to be driven by FIIs earlier, is now being driven by retail investors.

The sentiment can change quickly, like it did today, as that is how retail minds work. Their faith in India Inc. remains uninterrupted and domestic institutional investors (DIIs) keep pouring money in.

Now that Trump has signaled a ceasefire in the war, markets could recover sooner than expected and during this time, momentum stocks could lead the charge.

Momentum stocks are shares experiencing strong, sustained price trends, driven by market sentiment, volume, and high velocity.

Keeping that in mind, let’s look at 5 momentum stocks that could sustain the uptrend if the positive sentiment prevails.

#1 BSE

First on the list is BSE.

Bombay Stock Exchange (BSE) is Asia’s oldest stock exchange and one of the fastest-growing market platforms today.

It provides a high-speed ecosystem where investors and institutions trade shares, bonds, and derivatives every day. Most people know BSE because of its flagship index, the Sensex, but the business goes much deeper than that.

BSE runs BSE StAR MF, India’s largest mutual fund distribution platform, which handles close to 90% of the industry’s transactions. It’s also a market leader in SME listings, helping smaller companies raise capital and grow.

Over the last few years, BSE has strengthened its position as a core market infrastructure institution. All of these efforts have trickled down to its financial numbers.

In the past 5 years, BSE’s sales and net profit have compounded at an annual rate (CAGR) of 40% and 70%, respectively. This is a mean feat.

Its return on equity (ROE) and return on capital employed (ROCE) have averaged 12% and 16%, during the same time period.

Going forward, it has strong tailwinds expected to support growth. The management is focused on bringing more participants into the market and increasing liquidity.

A key part of this strategy is deeper engagement with foreign portfolio investors (FPIs) and large institutions, especially in monthly and longer-duration derivative contracts, where volumes can scale sustainably over time.

To meet rising demand from high-frequency and institutional traders, BSE is also expanding its co-location infrastructure to around 500 racks, improving speed, capacity, and operating leverage.

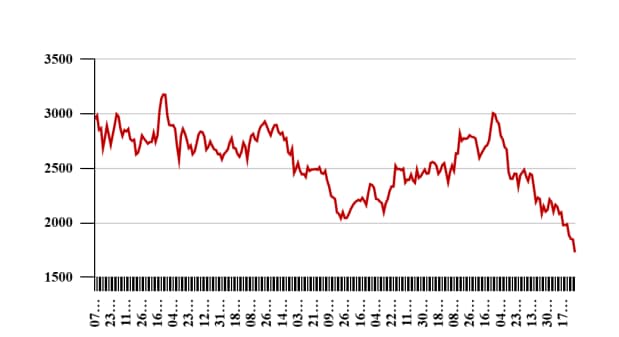

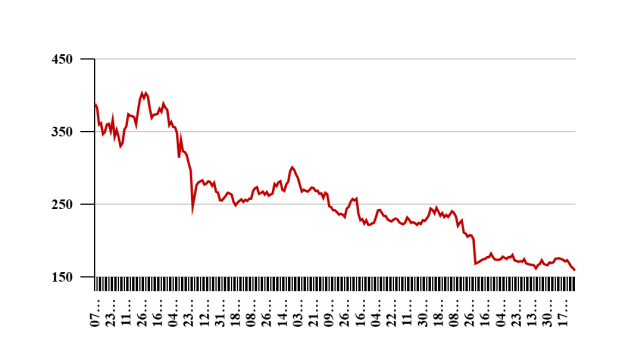

BSE Share Price

Data Source: BSE

#2 Avanti Feeds

Second on the list is Avanti Feeds.

Operating since 1993, Avanti Feeds manufactures and sells shrimp feed, and exports processed shrimp. It also has four windmills in Karnataka.

The company has synergies from Thai Union Group, which holds around 24.2% stake in the company. Thai Union is among the world’s largest shrimp, fish and pet food manufacturers and processed seafood producers, with a strong marketing and sales network worldwide.

This strategic partnership provides Avanti with the technical know-how in feed formulation leading to an industry-leading feed conversion ratio, and in shrimp processing, and access to its global marketing network.

Thai Union benefits from spreading its reach across key seafood producing nations.

Coming to Avanti Feeds’ financials, the company’s sales and net profit have grown at a CAGR of 6% and 8% over the past 5 years.

Its return ratios during the same time have been strong, with an average ROE and ROCE of 17% and 23% respectively.

The sentiment turned in favor of the company earlier this year after a landmark trade agreement in February 2026. Effective US tariffs on Indian shrimp were slashed from nearly 50% (which included punitive duties from 2025) down to just 18%.

At 18%, India now has a more favourable rate than its rivals, Vietnam and China. Since Avanti Feeds gets about 70% of its export revenue from the US, this deal improves realisations and profit margins.

While the reduction is positive, the industry remains vulnerable to sudden US policy shifts. Avanti Feeds also faces the primary challenge of rising input costs so investors should keep that in mind.

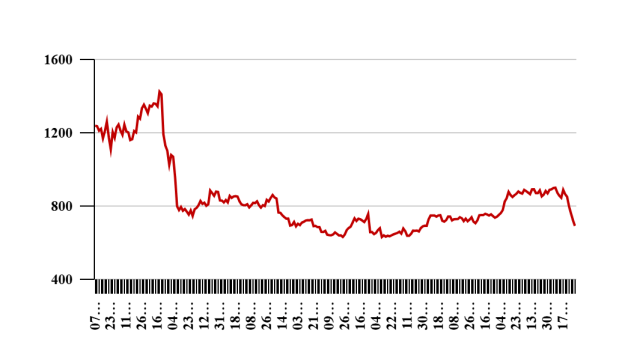

Avanti Feeds Share Price

Data Source: BSE

#3 ICICI Prudential AMC

Third on the list is ICICI Prudential AMC.

The company operates as an investment manager to ICICI Prudential Mutual Fund, along with a growing alternatives platform covering Portfolio Management Services (PMS), Alternative Investment Funds (AIFs), and offshore advisory mandates.

It has carved out a formidable moat. Despite the entrance of over a dozen new AMCs in the last decade, ICICI Prudential AMC has maintained its dominance by perfecting a strategy of deep physical penetration and aggressive digital adoption.

Unlike many of its competitors that rely on broad volume, ICICI Prudential leads in the industry’s most profitable niches, holding a staggering 26.3% market share in equity-oriented hybrid schemes and a leading 13.6% in active equity.

This leadership is fortified by its parentage. It leverages ICICI Bank’s vast network of over 7,200 branches, a luxury that independent players cannot match.

By combining this physical reach with a digital infrastructure that now handles over 95% of purchase transactions, the entity has created a barrier to entry based on scale and customer acquisition efficiency that few can replicate.

No wonder then, that it has reported high return on capital employed (ROCE) over the years. The latest ROCE stands at 103% while 3-year average ROCE stands at 96%.

Over the past 5 years, the company’s sales and net profit have grown at a compounded annual growth rate (CAGR) of 20%, respectively.

Going forward, the company is expanding in top cities and also investing in digital platforms, AI-led customer engagement, and fintech partnerships.

It has also planned to launch new products around passive funds and higher-margin alternatives, alongside international growth via IFSC GIFT City.

With the ongoing retail revolution in India, where household savings are shifting from physical assets like gold and real estate toward equities, ICICI Prudential is well placed.

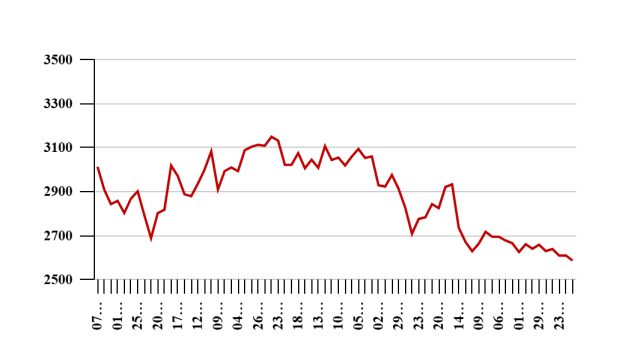

ICICI Pru AMC Share Price

Data Source: BSE

#4 Care Ratings

Fourth on the list is Care Ratings.

The company is a knowledge-based analytical group offering a range of financial services, centered around credit ratings, research, advisory and sustainability.

It provides advanced, Gen-AI risk intelligence solutions to banks and financial institutions via its proprietary platform, EdgeAvira.ai. These solutions cover credit risk modelling, regulatory reporting (Basel, IFRS), and data governance.

The company differentiates itself within the Indian financial ecosystem through market leadership, regulatory recognition, and technological focus.

It is India’s second-largest rating agency and also the first Indian credit rating agency to enter the global rating space, launching CareEdge Global IFSC.

Coming to Care Ratings’ financials, over the past 5 years, its sales and net profit have grown at a CAGR of 11% respectively.

The ROE and ROCE have averaged 15% and 20% during the same time.

Going forward, the company is expected to benefit from the steady expansion of India’s credit market, supported by rising investment needs in a growing economy.

It’s strengthening its business by scaling high-growth non-rating business segments such as analytics, advisory, and ESG, which are becoming more profitable.

Additionally, the company is pushing efforts through GIFT City and new operations in Africa, which are expected to diversify revenue and expand international presence.

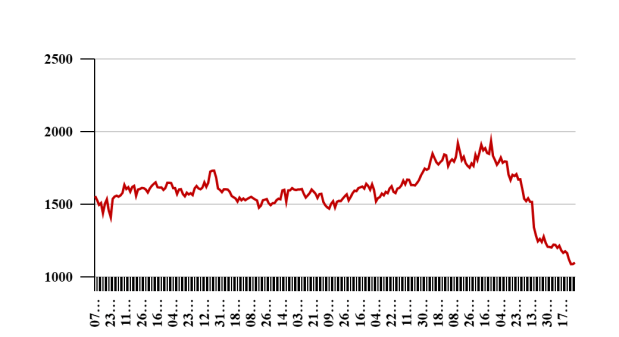

Care Ratings Share Price

Data Source: BSE

#5 Bajaj Consumer Care

Last on the list is Bajaj Consumer Care.

Incorporated in 2006, Bajaj Consumer is a part of the Shishir Bajaj group. The company is a leading manufacturer of light hair oil under the brand ADHO.

It has presence in other hair oil categories through Bajaj Brahmi Amla, Bajaj Coco Jasmine and Bajaj Kailash Parbat brands.

The company’s manufacturing facilities are located in Himachal Pradesh, Uttarakhand, and Assam. It recently completed acquisition of 100% stake in Banjara’s in May 2025 for Rs 1.2 billion (bn).

Coming to Bajaj Consumer’s financials, its revenue has grown at a CAGR of 3% over the past 5 years, while profits have almost halved during the same period.

Notwithstanding recent headwinds, its fundamentals remain intact. The 5-year average ROE and ROCE stand at 21% and 25%, respectively.

The company is expanding its product portfolio and market reach. The recent acquisition is expected to strengthen its capabilities in the personal care segment.

Bajaj Consumer Care is also focused on increasing its presence in emerging markets to diversify its revenue streams and capitalise on new opportunities.

Bajaj Consumer Share Price

Data Source: BSE

Conclusion

Many investors consider momentum investing strategy to be counterintuitive, but it’s actually quite simple.

If there are stocks that are outperforming the market when the market is falling, then think about how strongly investors believe in them. They are buying these stocks even when they are selling other stocks.

That shows the potential of keeping a close watch on momentum stocks. They can deliver significant outperformance.

That said, investors should evaluate the company’s fundamentals, corporate governance, and valuations as key factors when conducting due diligence before making investment decisions.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary