")

The Indigenisation Super-Cycle: Why India’s ‘Silent’ Suppliers are Moving Up the Value Chain

As the world speculates on whether it is on the verge of a full-blown war, thanks to the geopolitical tensions between Iran, Israel, and the United States, investors are looking at the Defence sector differently.

When it comes to India’s Defence Capabilities, the spotlight usually stays fixed on the giants like Mazagaon Docks and HAL. Investors often view them as the only safe harbours in a sector defined by massive capital and complex regulations. However, beneath the surface of these multi-billion-dollar contracts, a few small-cap contenders are quietly making significant inroads.

Two such lesser-known smallcap stocks have found an audience in smart investors due to the structural “moats” they have dug around their operations. In the defence industry, a moat isn’t built with cash alone, but with high switching costs, specialized R&D, and proprietary certifications that take years to earn. By mastering critical subsystems that larger firms find too specialized to produce in-house, these companies have effectively insulated themselves from competition.

As the Ministry of Defence ramps up its indigenisation list, the transition from being a mere vendor to a strategic partner is where the real value lies. For these two companies, the power in their stock isn’t derived from market hype, but from their structural pivot and the 70% self-reliance targets set by the government.

Let us look at these stocks to see if they have it in them to be the next multibagger.

Lloyds Engineering Works: Owning Mission-Critical Components of India’s Navy

Established in 1974, Lloyds Engineering Works is primarily engaged in the design, Manufacturing, and Commissioning of heavy equipment, machinery & systems for the HydroCarbon Sector, Oil & Gas, Steel Plants, Power Plants, Nuclear Plant Boilers, and Turnkey Projects.

With a market cap of Rs 5,231 cr as on 7th March 2026, the company as undergone a massive transformation, moving from a standard equipment manufacturer to a “design-to-execution” solutions provider with a primary focus on the Atmanirbhar Bharat initiatives in Defence and Nuclear power.

In July 2025, the company deepened its partnership with FINCANTIERI S.p.A. (Italy) a global shipbuilding giant to indigenously manufacture Controllable Pitch Propeller (CPP) Systems and Shafting Systems for the Indian Navy. A move that targets a critical gap in India’s naval supply chain, as these high-tech components were previously imported

Also, in December 2025, the company incorporated Lloyds Advance Defence Systems Limited, a wholly owned unit designed to spearhead entries into AI, robotics, autonomous systems, and advanced weaponry across land, air, and sea.

Lloyds has also secured an order of over Rs 20 cr from Cochin Shipyard in May 2025 for Fin Stabilizer systems for Next-Generation Missile Vessels.

It is quite apparent that the company is slowly making a mark in the defence sector. But the big question is if it has the operational strength to be the next possible multibagger? Let us look at the stand-alone financials to try and find out.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | 5-Year CAGR |

| Sales/Rs Cr | 114 | 70 | 50 | 313 | 624 | 756 | 46% |

| EBITDA/Rs Cr | -3 | -10 | 5 | 53 | 101 | 123 | Turnaround |

| Net Profits/Rs Cr | 2 | 0 | 6 | 37 | 80 | 100 | 119% |

And for the 3 quarters of FY26 ending in December 2025, the company has logged Rs 640 cr in sales, Rs 98 cr in EBITDA and Rs 80 cr in Net profits.

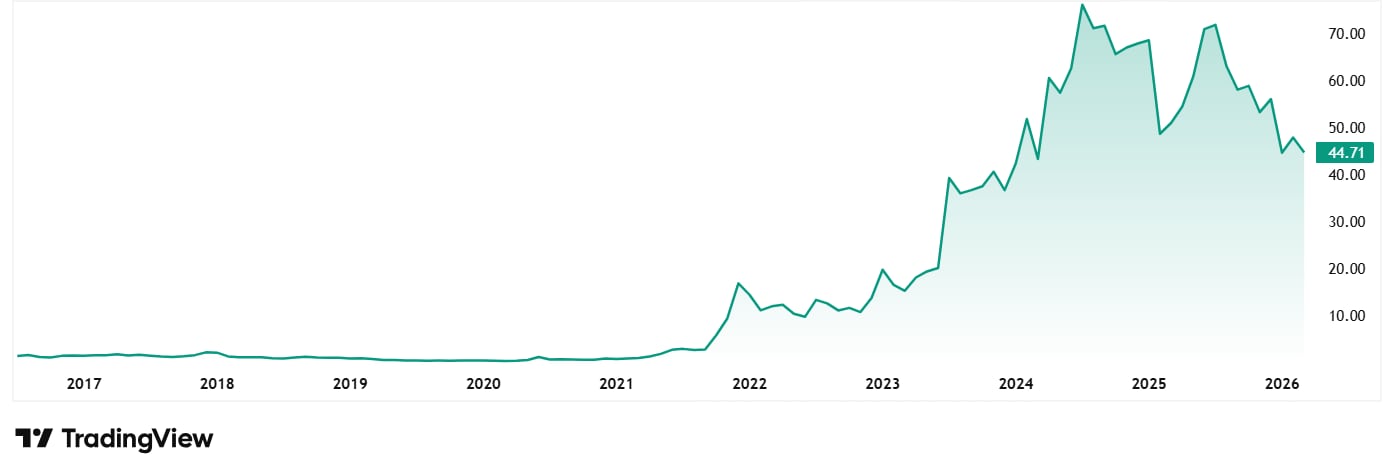

The share price of Lloyds Engineering Works Ltd was around Rs 1 in March 2021 and as of closing on 7th March 2026 it was Rs 46, which is a 4,500% jump in 5 years.

The Precision Play: Engineering Moats in Submarine Systems

At the current price, the stock is trading at a discount of 46% from its 52-week high, which is also its all-time high, of Rs 85. This fall was triggered by a combination of promoters selling their stakes and and high valuations leading to a sell rating by many among other factors. While profits grew by 118%, slower cash collections and a shift toward safer investments weighed on the price.

The stock is trading at a PE of 54x, while the current industry median is 28x, which suggests the stock is significantly undervalued relative to its profits potential.

Not only Defence, but the company is also building a niche for itself by being an active contributor to India’s Nuclear ambition, as a long-standing supplier to the Nuclear Power Corporation of India (NPCIL), providing Heavy Water Vapour Recovery systems for projects at Kakrapar (KAPP 3 & 4) and Rajasthan (RAPP 7 & 8).

Plus, the company also holds an MOU with BARC for Multi-Effect Distillation with Thermo Vapour Compression (MED-TVC) desalination technology, which is critical for nuclear power plants requiring high-purity water systems.

As per the recent investor presentation from February 2026, the company has signed an MoU with FlyFocus (Poland) to jointly develop and introduce advanced FPV drones and next-gen UAV systems for defence & security applications, with exclusive rights for Indian deployment.

Lloyds Engineering Works has evolved from a legacy fabricator into a strategic linchpin of India’s sovereign capabilities, with a robust Rs 1,665 cr standalone order book anchoring its next phase of growth. While the recent 46% price correction reflects broader market jitters and valuation cooling, the fundamental “design-to-execution” pivot remains intact, evidenced by a solid Net Profit CAGR and pioneering entries into naval propulsion and UAV systems.

Syrma SGS Technology Ltd – The Elcome Acquisition Moat

Incorporated in 2004, Syrma SGS Technology Limited is a Chennai-based engineering and design company engaged in electronics manufacturing services (EMS).

With a market cap of Rs 14,685 cr as on 7th March 2026, the company provides integrated services and solutions to original equipment manufacturers (OEMs) from the initial product concept stage to volume production through concept co-creation and product realization.

In late 2025, Syrma made its most significant strategic move by acquiring a 60% stake in Elcome Integrated Systems for Rs 235 cr, and through Elcome it also acquired Navicom Technology International, which specializes in maritime electronics.

With that, Syrma is now moving into Box Builds for the military, manufacturing entire electronic systems (like navigation radars and fire detection systems) rather than just individual board. The company has also achieved AS9100 Aerospace certification, allowing it to supply directly to global and domestic aerospace OEM.

Syrma is also investing Rs 1,595 cr in a new facility in Andhra Pradesh for PCB and Copper Clad Laminate (CCL) manufacturing. Which means it is moving backward into the supply chain, and instead of just assembling components, it will now make the base materials (CCLs), making India’s electronics supply chain more resilient.

Let us look at the financials to see if the company has what it takes to sustain and grow with all these big changes.

| FY | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 | 5-Year CAGR |

| Sales/Rs Cr | 862 | 886 | 1,267 | 2,048 | 3,154 | 3,787 | 35% |

| EBITDA/Rs Cr | 135 | 102 | 129 | 192 | 203 | 323 | 19% |

| Net Profits/Rs Cr | 92 | 69 | 79 | 123 | 124 | 184 | 15% |

And for the 3 quarters of FY26 ending in December 2025, the company has logged sales of Rs 3,354 cr, an EBITDA of Rs 361 cr and Rs 226 cr in Net profits, hinting at a much stronger end to FY26

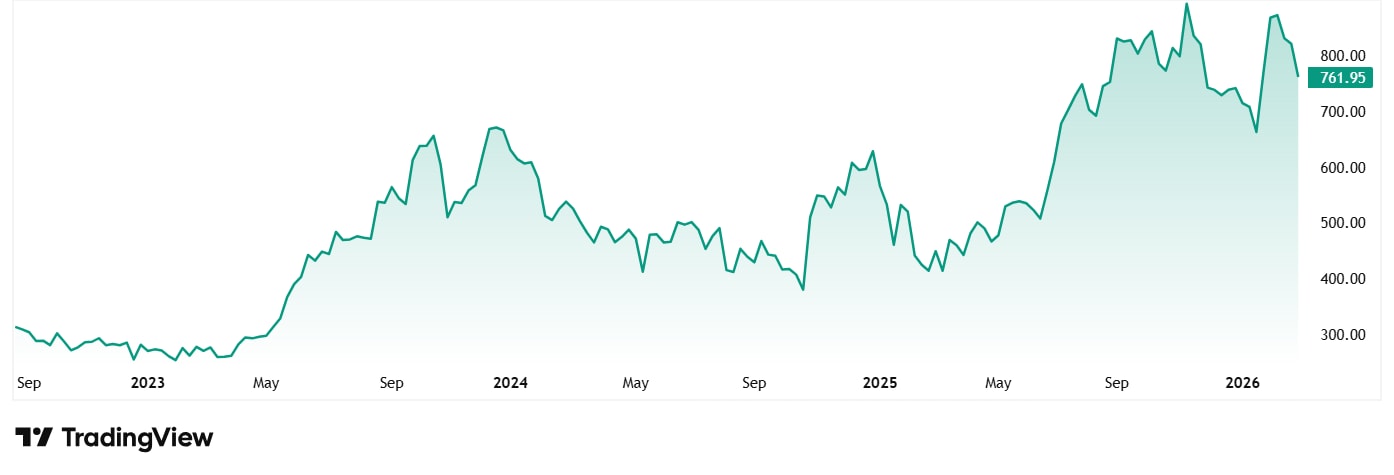

The share price of Syrma SGS Technology Ltd was around Rs 310 when listed in August 2022 and as of closing on 7th March 2026 it was Rs 762, which is a 145% jump.

As for the valuation, the stock of the company is trading at a PE of 52x and the industry median currently is 28x.

The Solar Entry

In October 2025, Syrma (49%) partnered with Premier Energies (51%) to acquire Ksolare Energy, a specialist in Solar Inverters. This move is specifically designed to capitalize on the PM Surya Ghar Muft Bijli Yojana (the national rooftop solar scheme). Inverters are the most technologically complex part of a rooftop solar setup, and Syrma will now manufacture these locally. By manufacturing solar inverters and power electronics in India, Syrma is directly contributing to the “Atmanirbhar” goal of reducing reliance on Chinese power electronics.

Syrma is evolving from a simple assembler into a high-tech “Atmanirbhar” powerhouse. By acquiring Elcome and investing Rs 1,595 crore in new facilities, it now builds entire navigation systems for the military. While its 52x PE is higher than the industry average, a 145% price jump since listing and solid profits show strong market trust. As it starts making solar inverters to replace Chinese imports, Syrma is securing a vital spot in India’s green and defense future.

Power Up Your Portfolio: The Small-Cap Pivot to Sovereignty

The days when India’s defence narrative was written solely by state-owned giants seem to be becoming a thing of the past. As the global geopolitical climate remains volatile, investor attention is shifting toward players like Lloyds Engineering and Syrma SGS, who are quietly moving up the value chain.

By trading simple assembly for complex intellectual property, whether in naval propulsion or high-end maritime electronics, these companies are building the kind of structural moats that usually belong to blue-chip giants. For investors, the current landscape offers a tale of two trajectories.

Lloyds has navigated a significant price correction, yet its transformation into a design-to-execution specialist suggests the underlying engine is still working well. On the other hand, Syrma’s aggressive move into backward integration and solar electronics reflects a company no longer content with being just a middleman.

It will be a fascinating ride to watch how these two underdogs move in the months and years to come. Add them to a watchlist and keep an eye on them if you don’t want to miss out on any big happenings with them.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.