")

India is ageing faster than most people realise. The number of senior citizens is expected to rise to around 23 crores by 2036, making up nearly 15% of the population, according to the Press Information Bureau. This is a sharp jump from about 10 crores in 2011. By 2050, this number could go even higher. This shift is not gradual anymore. It is happening in front of us.

The government has already started preparing for this change. Schemes like Atal Pension Yojana, Indira Gandhi National Old Age Pension Scheme, and expanded healthcare coverage under Ayushman Bharat are aimed at improving financial and medical security for the elderly. There is also focus on senior citizen welfare funds, care infrastructure, and digital access. The idea is simple. Help people live longer with dignity and some level of financial stability.

These steps are important. But they cannot do everything on their own. As incomes rise and families become nuclear, people are taking more responsibility for their own retirement. This is where private players come in. Managing long-term savings, offering pension products, and converting savings into steady income represents a large opportunity. The shift from informal support to structured retirement planning is clearly underway.

The stocks selected here are closely linked to this shift. They are not generic financial names. They either manage long-term savings or help turn that savings into income after retirement. The focus is on businesses that benefit directly from rising retirement planning, strong inflows, and long-term money. Companies with broader or unrelated exposure have been kept out to keep the idea clear and focused.

#1 HDFC Asset Management Company: The SIP Powerhouse Anchoring India’s Retirement Savings

Incorporated in 1999, HDFC Asset Management Company provides fund management services.

HDFC Asset Management Company reported a steady quarter. Growth was supported by strong inflows and continued traction in SIPs. Total revenue for Q3 FY26 stood at Rs 1,074 crore, up 15% year-on-year (YoY). Profit after tax came in at Rs 770.1 crore. This was up 20% YoY. Margins remained stable, helped by cost control and operating leverage.

The business continues to benefit from a structural shift in savings. More money is moving from physical assets to financial products. Systematic investment plan (SIP) flows remain strong. Monthly SIP inflows are at record levels. The company has seen steady investor additions across regions. Total asset under management (AUM) crossed Rs 9 trillion. Equity assets form a large share. This reflects preference for long-term wealth creation.

Expanding the Perimeter: Alternative Assets and Institutional Mandates

New growth areas are also picking up. PMS AUM crossed Rs 5,000 crore during the quarter. The company secured large institutional mandates. It also raised about Rs 1,300 crore in its structured credit fund. The alternatives platform is being built gradually. The focus is on institutions and high-net-worth investors. Management has indicated that scale is the priority here. Margins may remain lower in the near term.

The company is also expanding beyond mutual funds. It is strengthening portfolio management services (PMS), alternative investment fund (AIF) and international offerings. GIFT City is part of this strategy. Product launches will remain selective. The approach is to deepen existing capabilities. Expansion will be driven by conviction, not volume.

HDFC AMC is well placed in the retirement savings space. SIP flows are long-term in nature. Pension-linked mandates like Employees’ Provident Fund Organisation (EPFO) add to this stability. Retail participation is also rising. This aligns with India’s ageing trend. More individuals are building retirement corpus through market-linked products.

Growth outlook still looks healthy. More money is moving into financial products, and digital channels are helping reach a wider set of customers. Investor participation is also picking up.

At the same time, some regulatory changes could affect pricing. This may put pressure on margins in the near term. The company is trying to offset this by keeping a tight control on costs. The idea is to protect profitability and grow earnings steadily over time.

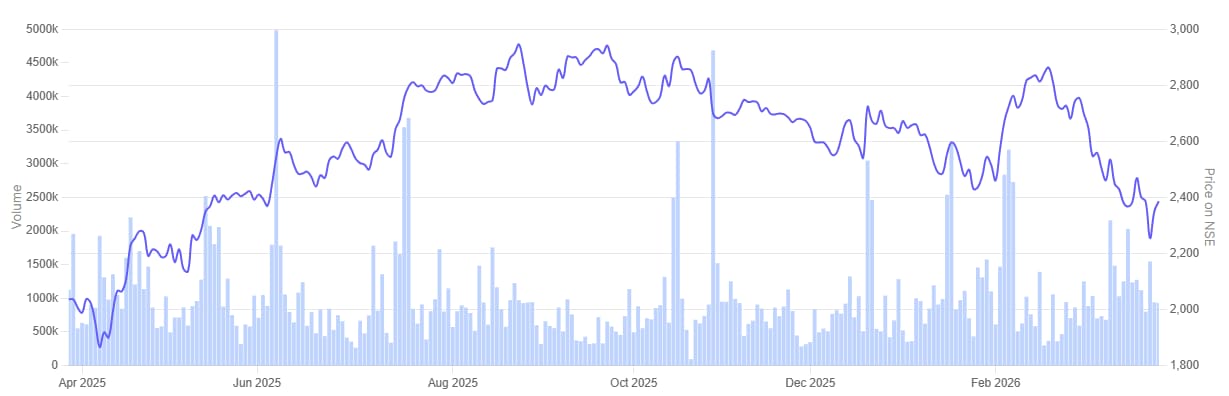

In the past one year, share price of HDFC Asset Management Company is up 17.4%.

HDFC Asset Management Company 1 Year Share Price

#2 SBI Life Insurance Company: Dominating the Bancassurance and Annuity Landscape

SBI Life Insurance Company is engaged in the business of life insurance and annuity. It was started as a joint-venture between State Bank of India and BNP Paribas Cardif S.A.

SBI Life Insurance reported steady growth in Q3 FY26, supported by strong demand across segments and improving industry momentum. Gross written premium for the quarter stood at Rs 73,350 crore, up 20% YoY. Profit after tax came in at Rs 1,670 crore, reflecting a modest 4% YoY growth, impacted by GST and regulatory changes during the period.

The company continued to gain market share, driven by higher individual policy sales and better traction across distribution channels. New business premium grew 19% to Rs 31,330 crore. Individual rated premium rose 15% YoY. Renewal premium also remained strong, growing 21%, indicating steady persistency and a stable customer base. Assets under management crossed Rs 5.1 trillion, reinforcing the long-term nature of the business.

The Protection Pivot: Shifting the Product Mix for Higher Value

Product mix remained a key driver. Unit linked insurance plan continue to dominate, though the share has moderated slightly. Protection business showed strong traction, with annual premium equivalent (APE) growth of 24%. The company has been focusing on expanding its protection portfolio and improving product mix. At the same time, non-par and participating products have seen traction, supported by new launches during the year.

Importantly, the retirement segment continues to scale up. The company reported annuity and pension new business of Rs 6,410 crore. Management highlighted that these plans help customers build a retirement corpus and generate income in later years. This aligns with rising awareness around financial security and ageing demographics in India.

Distribution remains a key strength. The bancassurance channel, led by SBI and partner banks, continues to contribute the majority of business. The company has also expanded its agency network and added new branches during the year. Digital channels are gaining traction, with online sales growing and a higher share of policies being processed digitally.

Looking ahead, the company expects growth to remain steady, supported by improving product mix and distribution reach. Margins are likely to stay within the guided range, even as regulatory changes continue to have some impact. The focus remains on balanced growth across protection, savings, and retirement products, with an emphasis on long-term value creation.

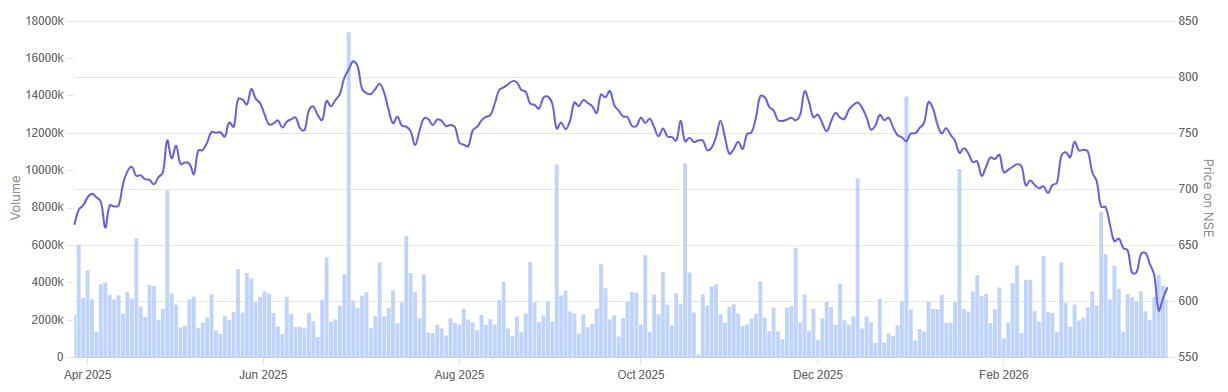

In the past one year, share price of SBI Life Insurance Company is up 19.8%.

SBI Life Insurance Company 1 Year Share Price

#3 ICICI Prudential Life Insurance Company: Mastering Product Diversification and Protection-Led Growth

ICICI Prudential Life Insurance Company carries on business of providing life insurance, pensions and health insurance products to individuals and groups. The business is conducted in participating, non-participating and unit linked lines of business.

ICICI Prudential Life Insurance reported a stable performance in Q3 FY26, supported by steady demand and product diversification. Profit after tax for the quarter stood at Rs 390 crore, up 19.6% year-on-year, driven largely by higher investment income. Value of new business (VNB) for the quarter came in at Rs 615 crore, with margins holding at 24.4%, indicating stable profitability despite regulatory changes.

Growth remained moderate. Retail APE grew 9.9% YoY in Q3, while overall APE growth was 3.6%. The company highlighted that growth was impacted by a high base in the previous year. However, policy volumes remained strong, with retail policies rising 11.7% YoY. This indicates continued demand across customer segments.

A Two-Pronged Strategy: Protection Growth and Guaranteed Returns

Product mix continues to evolve. Protection business saw strong traction, with 40.8% YoY growth in Q3. This was supported by GST-related changes and improving awareness. Non-linked savings products also performed well, growing 15.2% YoY, as customers locked in guaranteed returns. ULIP business remained steady, supported by improving market conditions and customer confidence.

The retirement segment saw some moderation during the quarter. Annuity business declined 16.4% YoY on a high base, though single premium annuity products continued to see traction. Management indicated that this segment remains important and is expected to normalise over the coming quarters. The company continues to focus on long-term savings products that help customers build a retirement corpus over time.

The company is also expanding its product suite. New launches include long-term savings and wealth creation plans such as Wealth Forever, SmartKid 360, and Wealth Elite Pro. These products are designed to cater to different life stages and financial goals. The strategy is to offer a wide range of products across protection, savings and retirement needs.

Distribution remains well diversified. The company has added over 46,000 agents and expanded partnerships across banks and non-bank channels. No single channel dominates the business, which helps manage risk across cycles. The focus remains on aligning product offerings with customer demand rather than pushing specific categories.

Going ahead, the company expects growth to stabilise after the high base impact. Product diversification, cost discipline and distribution expansion are expected to support performance. While some pressure may remain from regulatory changes, the company remains focused on growing absolute VNB and maintaining profitability over the long term.

In the past one year, share price of ICICI Prudential Life Insurance Company is down 8.3%.

ICICI Prudential Life Insurance Company 1 Year Share Price

#4 HDFC Life Insurance Company: Scaling the Retail Protection Moat through Digital Innovation

HDFC Life Insurance Company is engaged in carrying on the business of life insurance. The company offers a range of individual and group insurance solutions. The portfolio comprises of various insurance and investment products such as protection, pension, savings etc.

HDFC Life Insurance reported steady growth in Q3 FY26, supported by strong demand across protection and savings products. Profit after tax stood at Rs 1,414 crore, up 7% YoY. Excluding the one-time impact of new labor code changes, underlying profit growth was closer to 15%. Margins remained stable, with VNB margin at 24.4%, reflecting resilience despite regulatory changes.

Growth was largely volume-led. Individual APE rose 11% YoY. Policy volumes saw strong traction, with a large share coming from first-time buyers. Market share also improved during the period, indicating steady competitive positioning across segments.

The ‘Project Inspire’ Effect: Enhancing Operational Efficiency through Digital Transformation

Product mix continued to shift towards protection. Retail protection grew 70% YoY in Q3, significantly ahead of overall growth. This was supported by GST-related affordability and higher demand from underpenetrated segments. ULIPs remained a key contributor, while non-par savings saw gradual recovery as customers looked for guaranteed returns.

The retirement segment remains a smaller part of the mix but continues to be relevant. Annuity products contributed around 4% of the portfolio. The company is also preparing to launch new offerings such as variable annuity products in the coming months. These products are expected to cater to customers seeking post-retirement income with some level of market linkage.

On distribution, the company continued to expand its reach. The agency network saw strong additions, with over 80,000 agents onboarded during the period. The branch network has crossed 700 locations, completing a multi-year expansion phase. Bancassurance growth was relatively softer in the quarter due to competitive intensity, though management expects this to normalise over time.

Operational initiatives are also underway. The company is investing in digital and process improvements under Project Inspire, aimed at improving efficiency and turnaround times. Early benefits are visible in group business, while retail rollout is expected over the next few quarters.

Going ahead, growth is expected to remain steady. Protection demand is likely to stay strong, while savings and retirement products should benefit from improving financial awareness. Regulatory changes may continue to impact margins in the near term, but the company expects to normalise these effects over the coming quarters.

In the past one year, share price of HDFC Life Insurance Company is down 8.3%.

HDFC Life Insurance Company 1 Year Share Price

Valuation Check: Is the ‘Silver Economy’ Growth Already Priced In?

Let’s now turn to the valuations of the companies in focus.

HDFC Asset Management Company is usually looked at on a price-to-earnings basis. The stock is trading at 26.2x. This is a bit lower than its 5-year average of 29.0x. It is also close to the industry median of 25.6x. Valuations have eased slightly. At the same time, the business continues to see steady flows.

For life insurers, price-to-book is more relevant. Return ratios and valuation levels help in understanding the difference between companies.

Valuation of Insurance Companies in Focus

| Sr No | Company | P/BV Ratio | 5-Year Average EV/EBITDA | ROCE | ROE |

| 1 | SBI Life Insurance Company | 9.7 | 10.3 | 16.90% | 15.10% |

| 2 | ICICI Prudential Life Insurance Company | 5.7 | 7.8 | 11.90% | 10.40% |

| 3 | HDFC Life Insurance Company | 7.4 | 9.8 | 6.60% | 10.80% |

SBI Life is relatively better on return ratios. Return on Capital Employed (ROCE) is at 16.9% and Return on Equity (ROE) at 15.1%. The stock is trading near its historical level at 9.7x versus 10.3x. ICICI Prudential Life is at 5.7x. This is lower than its 5-year average of 7.8x. Return ratios are also lower at 11.9% ROCE and 10.4% ROE. HDFC Life is at 7.4x compared to 9.8x earlier. Return ratios remain lower with ROCE at 6.6% and ROE at 10.8%.

The shift is visible. People are slowly planning for retirement. Savings are moving into financial products. SIPs are steady. Pension and annuity products are also seeing interest.

These companies are part of that journey. One focuses on building the savings over time. The others come in later with protection and income. The numbers show where each one stands today. From here, it will depend on how they grow and manage margins.

The Long Game: Why Execution Will Separate the Winners in India’s Ageing Shift

This is not a quick story. It will take time. But the change is already visible. People are slowly becoming more aware of retirement planning. Savings are getting more structured. The shift towards financial products is also picking up.

There is still a lot of room to grow. Many people are not fully prepared for retirement yet. Insurance reach is still low. That means both asset managers and insurers have space to expand. One side helps build savings over time. The other helps convert it into income later.

Right now, the numbers show a gap. Some companies are stronger on returns. Some are trading at higher valuations. From here, it will depend on how they grow and manage their business. Product mix and margins will matter. This space will grow, but not everyone will grow at the same speed.

You can track how these companies are progressing by adding these stocks to your watchlist.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.