")

You open your phone to check one message. A few minutes later, you have watched five reels, two food vlogs, one finance podcast clip, and a stranger explaining how to make money using stock charts.

You earned nothing from this. Someone else did.

Every scroll, pause, and accidental replay feeds a system that quietly turns attention into money. What feels like timepass has today become serious business.

India’s creator economy is growing fast.

According to report by the Boston Consulting Group presented in Waves 2025 Mumbai, there are an estimated 2 to 2.5 million active digital creators in the country today. These creators influence over $350 billion in consumer spending every year.

This impact could rise to more than $1 trillion by 2030, while direct revenues from the ecosystem may reach $100–125 billion by the end of the decade, according to the Press Information Bureau.

This makes it an opportune time to look at the investment angle.

The shift is structural, not temporary. Content is no longer just entertainment. It drives subscriptions, advertising yields, licensing income, and digital engagement-led spending. As monetisation models mature, attention is steadily converting into predictable cash flows.

In selecting stocks for this theme, the focus stays tight. Only companies where content or creators sit at the centre of the revenue model are considered.

Broader digital or marketing-led plays are excluded, where creators are mainly acquisition tools. Very small and illiquid names are also left out.

The final list reflects businesses where content-led monetisation is visible, scalable, and fundamental to long-term growth.

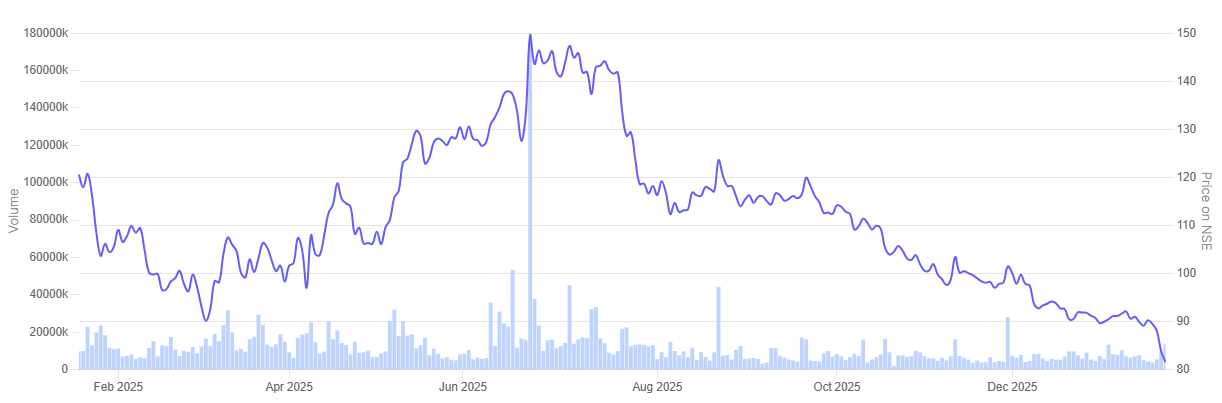

#1 Zee Entertainment Enterprise: The Legacy Pivot

Zee Entertainment Enterprises is mainly in the following businesses: broadcasting of satellite television channels, space selling agent for other satellite television channels, and sale of media content i.e. programs / film rights / feeds /music rights.

The company recorded weak results in Q2 FY26 as it stepped up spending to rebuild viewership and strengthen its digital business.

For Q2 FY26 the company earned revenue of Rs 1,969 crore which is lower than the Rs 2,001 crore reported in the year-ago period.

Profit after tax stood at Rs 76 crore which is significantly lower than Rs 209 crore earned in the year-ago period due to higher content and promotional costs tied to new show launches and the rollout of regional channels.

Advertising revenue remained weak, declining 11% year on year (YoY), though management pointed to a gradual pickup during the festive period, led largely by FMCG advertisers.

Digital continued to provide support.

ZEE5 revenue rose 32% YoY, helped by the introduction of language-based subscription packs and stronger engagement across regional markets. The platform reported quarterly revenue of over Rs 311 crore and cut its earnings before interest, tax, depreciation, and amortisation (EBITDA) loss by more than 80%, moving closer to breakeven.

The company is also expanding into short-form formats and omni-platform content monetisation, with management expecting margins to recover as costs stabilise in the second half of the year.

In the past year, Zee Entertainment Enterprises tumbled 31.5%.

Zee Entertainment Enterprises 1 Year Share Price Chart

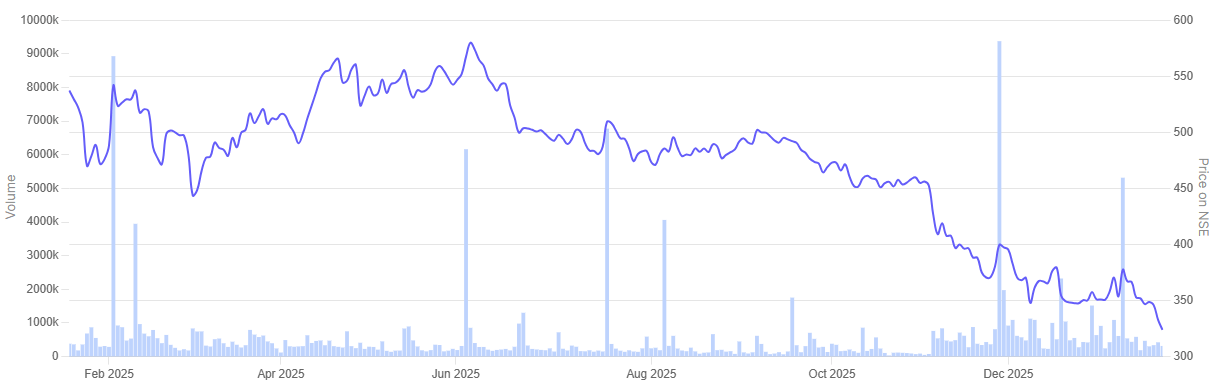

#2 Saregama India: The Content Arbitrage

Saregama India is the oldest music label company from India (established 1902, erstwhile “Gramophone Company of India” & then “HMV”). The company is aiming to be a pure-play content company supported by the global consumption boom.

Since 2017, Saregama has been making headlines again owing to the launch of two unique initiatives, Saregama Carvaan and Yoodlee Films.

The company reported a weak set of numbers in Q2 in FY26. Revenue for the quarter under consideration stood at Rs 230 crore which is lower than Rs 242 crore reported in a year ago period. Net profit for Q2 FY26 stood at Rs 44 crore which is marginally lower from Rs 45 crore reported in Q2 FY25.

Saregama India has changed the way it plans to source film music by investing directly in Bhansali Productions. The company will put in Rs 325 crore as a primary investment.

Its stake is expected to move between 28% and 49.9% by October 2028, depending on how the studio performs. Bhansali Productions reported revenue of Rs 304 crore and a net profit of Rs 45 crore in FY25, placing it among the more profitable film production houses.

The deal gives Saregama exclusive access to all future music from Bhansali Productions. This could account for about 30-40% of its Hindi film music pipeline, without the uncertainty of bidding for each project. At the same time, Saregama plans to slowly step away from its own film production over the next three to five quarters. This is expected to free up Rs 150–175 crore of capital.

Management expects the move to support margins, reduce content risk, and make the investment earnings accretive by FY27, while strengthening its position in the creator-led content space.

In the past year, Saregama India nose-dived 39.3%.

Saregama India 1 Year Share Price Chart

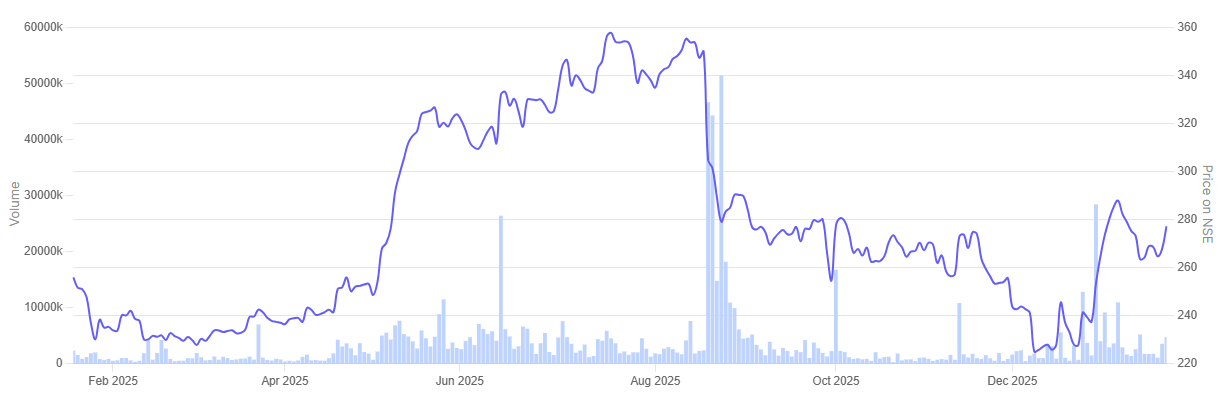

#3 Nazara Technologies: The Global Gaming IP Play

Nazara Technologies is the leading India based diversified gaming and sports media platform with presence in India and across emerging and developed global markets such as Africa and North America. The company’s offerings range from interactive gaming, eSports to gamified early learning ecosystems.

Nazara Technologies posted strong topline growth in Q2 FY26, led by its gaming businesses outside India, even as one-off issues hit the bottom line.

For Q2 FY26 quarterly revenue rose 65% YoY to Rs 526 crore, supported by mobile games, PC and console publishing, and offline gaming formats. Profit after tax, however, slipped into a loss of Rs 33.9 crore for the quarter as compared to profit of Rs 16 crore reported in Q2 FY25 due to impairments linked to its exposure to real-money gaming.

International markets now contribute over 90% of gaming revenue, underlining the company’s shift toward global IP-led growth.

Nazara continues to invest in gaming IPs, esports, and creator-driven content through platforms such as Nodwin Gaming. It is also expanding offline formats like Funky Monkeys and plans to relaunch Smaaash in FY27.

Management said the focus remains on building scalable franchises that can be monetised across platforms, aligning the business closely with the creator-led gaming economy.

In the past year, Nazara Technologies is up 8.9%.

Nazara Technologies 1 Year Share Price Chart

Valuation Audit: Are Content Stocks Undervalued?

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | 3 Year Median EV/EBITDA | ROCE |

| 1 | Zee Entertainment Enterprises | 6.2 | 11.1 | 9.2% |

| 2 | Saregama India | 16.8 | 25.8 | 17.2% |

| 3 | Nazara Technologies | 8.9 | 35.6 | 2.5% |

Zee Entertainment is currently trading at about 6.2 times EV/EBITDA, which is sharply lower when compared to its three-year median of 11.1 times. The discount mirrors the stress in advertising revenues and the slow pace at which the digital transition is translating into returns. At 9.2 percent, return on capital is still low. It tells you efficiency has not really turned the corner yet.

Saregama India is trading at about 16.8 times EV/EBITDA. Its three-year average is much higher, at 25.8 times. This gap exists even though returns are better here, with ROCE at 17.2 percent. The steady cash flow from its music catalogue across streaming and short-video platforms is visible. The market seems cautious on how fast growth will come, not on whether the business works.

Nazara Technologies is priced at roughly 8.9 times EV/EBITDA. That is a sharp fall from its three-year median of 35.6 times, reflecting recent volatility rather than long-term potential. Earnings volatility and regulatory uncertainty have weighed on returns, keeping ROCE low at 2.5%. At the same time, gaming remains a long-cycle business where IP creation takes time.

Overall, valuations look more sober than in the past. The real test now is execution. Investors need to judge whether improving monetisation can lift returns, instead of assuming that old multiples will return on their own.

Conclusion

The creator economy in India is clearly expanding, but the investment landscape around it is still limited. Content consumption is rising every year, yet only a few listed companies have been able to build businesses where attention steadily turns into revenue. In this space, scale and ownership of content matter far more than temporary spikes in engagement.

Recent valuation corrections reflect this reality. Advertising cycles remain uneven. Digital investments take time to pay off. Regulatory and execution risks are still present. As a result, stock prices today are less about optimism and more about delivery.

For investors, the opportunity is not in chasing the idea of creators, but in backing companies that can monetise content repeatedly and across platforms. The real test ahead is not growth in views or users, but whether these businesses can convert that growth into consistent returns over time.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.