")

Recently, we wrote to you about The 3 ‘quiet’ winners of India’s data centre rush. Today, we take this conversation forward by discussing the unexpected winners.

Let’s first rewind a bit and understand the opportunity and its scope. We covered that Colliers India reported that India’s data centre capacity had grown to 1.26 gigawatts (GW) in April 2025, up from 0.3 GW in 2018. This is a 30-fold increase in data traffic since 2017.

Rising penetration of smartphones, over-the-top (OTT) platforms, digital payments, and e-commerce has driven this growth. But this is just scratching the surface. Jefferies estimates that the capacity will quintuple to 8 GW over the next five years, driven by rising internet traffic.

This expansion is estimated to require an investment of $30 billion (about ₹2.6 trillion). This will open up a range of downstream opportunities for Real estate ($6 billion), Electrical and power systems ($10 billion), Racks ($7 billion), cooling systems ($4 billion), and Network Infrastructure ($1 billion).

In our earlier piece, we covered three hidden stocks that could benefit: Kirloskar Oil Engines, which supplies generators and firefighting pumps to data centres, Bazel Projects, which provides substation and transmission line systems, and KRN Heat Exchange, which provides data centre cooling products. Each of these plays a key role in the data centre ecosystem.

The relevance becomes even sharper when you look at what’s unfolding in the tech world.

Data centres are the places where servers store and process the information that keeps our digital lives running. The growth of cloud computing, the rapid rise of artificial intelligence (AI), and the vast amount of data created by businesses and consumers every day are all driving this demand.

Orient Technologies Annual Report states that the data centre industry in India is expected to grow to ₹240-280 billion by FY27, from ₹84.5 billion in FY23. As a result, India has emerged as the second-fastest-growing data centre market in Asia-Pacific.

Several factors, including regulatory mandates and data localisation, digital consumption, cloud adoption, government policies such as the Data Centre Incentive Scheme and the proposed Data Centre Economic Zones, will drive this expansion. Next, apart from this little-known realty stock that is secretly building a ₹100 billion data centre empire, these three stocks could be among the gainers. Let’s take a look…

#1 Orient Technology: Building the backbone of the data-driven economy

Orient Technology began as an Information Technology transformation partner in 1997, evolving from a seller of computer and telefax machines to a digital provider and transformation partner focused on IT asset lifecycle management. The company provides reliable IT infrastructure, managed services, and digital innovation.

Expanding Presence in Data Centre and Cloud Technologies

Within the data centre, it offers a full suite of hardware and software components and related services. This includes servers and storage systems, networking components, and collaboration solutions, including CCTV surveillance systems and video conferencing platforms.

High-scale or hyper-scale data centres are identified as their customers. A significant operational milestone during the quarter relates directly to data centres. A leading insurance company, New India Assurance, placed a multi-year order worth ₹308.1 million with Orient Technologies for network, backup, and storage solutions across New India Assurance’s data centres.

Orient is also present in future-ready technologies such as hyperconverged infrastructure, virtualisation, software-defined technologies, cloud and network solutions, virtual desktop infrastructure, and managed services. The company provides the complete IT Infrastructure for the data centres.

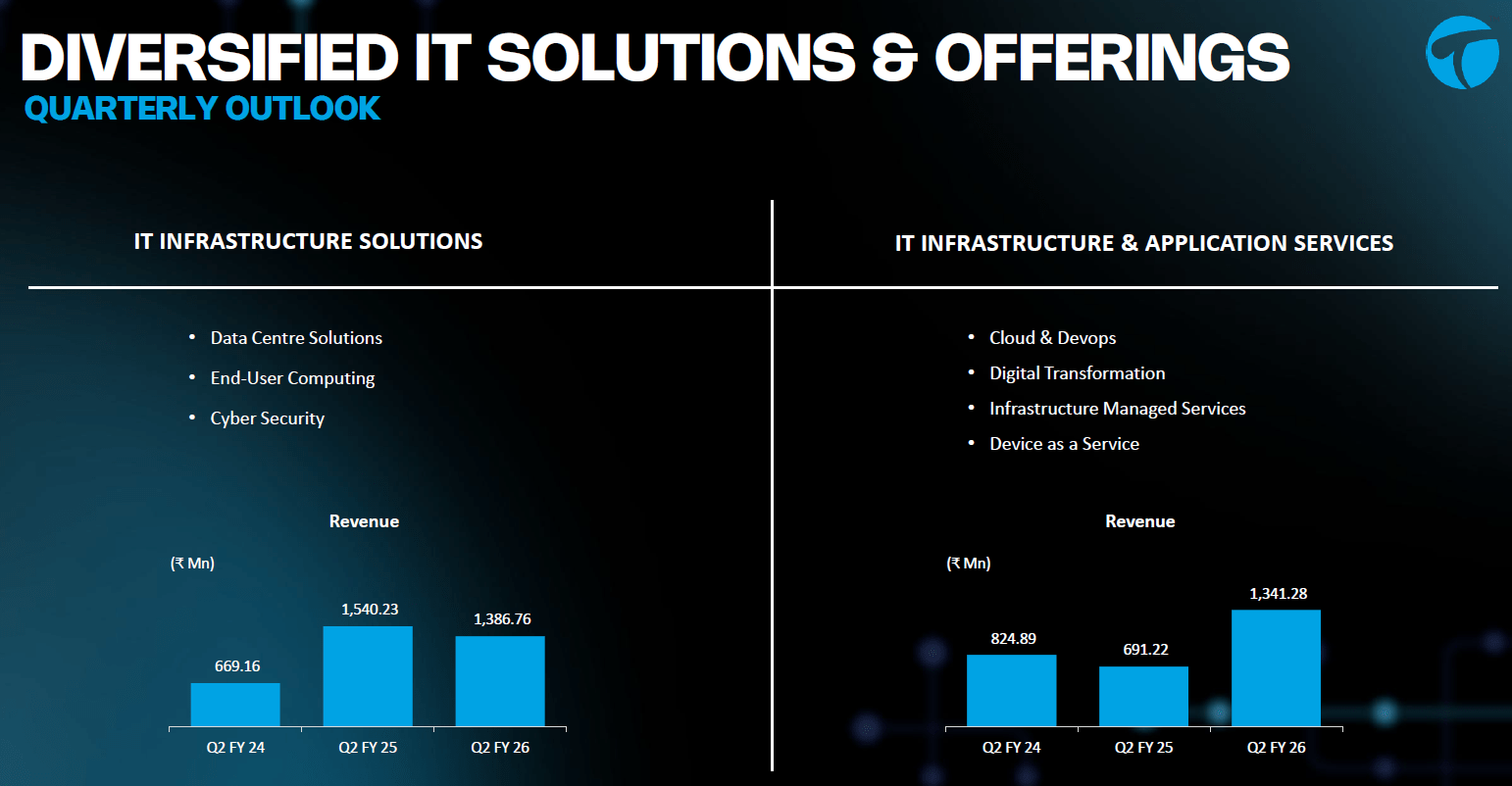

Orient has reorganised its business into two core business lines from FY26, aiming to balance its contributions. IT infrastructure solutions (which include data centres and cybersecurity) and applications and IT infrastructure services both contribute about 50% (each) to revenue.

Orient Segment Performance

The company is steadily increasing its revenue share from cloud and data management services, rising from 16.0% in FY21 to 24.1% in FY25. Most of its business operations are based in India. The company aims to expand its footprint and serve a larger customer base worldwide.

Steady Growth Momentum in Q2 FY26

In Q2FY26, the company’s revenue rose 22.3% year-on-year to ₹2.7 billion. At the same time, EBITDA (earnings before interest, tax, depreciation, and amortisation) surged 6.0% to ₹219.6 million, with a lower margin of 8.0%. Margins were impacted by set-up costs related to strategic investments and the Security Operating Centre (SOC).

As a result, profit after tax (PAT) fell 6.7% to ₹141.7 million. But management expects margins to improve starting Q4 FY26 as set-up costs taper and services-led revenues scale up. Orient reported a strong order book of ₹4.1 billion for the remainder of FY26, with billings of ₹1.8 billion in Q2FY26.

Strategic Shift Towards a Service-Led Growth Model

Looking ahead, the company is strategically moving towards a service-led business model, from single-product sales to bundled offerings that integrate value-added services. This approach aims to enhance customer value, improve margins, and ensure long-term revenue sustainability through an annual recurring revenue model.

To this end, Cloud and Digital Transformation remain key drivers of growth. The company provides solutions such as SecOps (security in the cloud) and SynOps (cloud financial management) to help customers optimise their increasingly expensive cloud billing. It is fully on track to begin commercialising the SOC and generating revenue from the latter half of Q3 or early Q4.

The SOC investment is expected to strengthen the cybersecurity portfolio and increase recurring service revenue. Another centre in Turbhe, Navi Mumbai, is ready for operational purposes. The company expects to begin generating revenue from this centre by the end of Q3 or early Q4.

Over the longer term, the company aims to become one of the top five System Integrator partners in India within three years. The company is confident that FY26 will close with solid double-digit revenue growth due to strong demand across digital, cloud, and managed services.

While operations are currently concentrated in India, generating the predominant share of revenue. Orient also aims to expand its geographic footprint and cater to a broader global customer base, targeting Asia Pacific countries or the Middle East within three years.

#2 Blackbox: Where Global Scale Meets Next-Gen Data-Centre Execution

Black Box operates as a global digital infrastructure integrator, offering broader technology solutions and services to global markets and across various sectors. It serves mainly through the Global Solutions Integration segment, which provides connectivity infrastructure, cybersecurity, and data centre services.

A Glocal Operating Model Redefining Black Box’s Global Ambition

The company operates on a “glocal” model (think global, act local) to serve its more than 1,000 global clients. It has a presence in 35 countries across six regions, including North America, Latin America, Europe, Asia-Pacific, the Middle East and Africa, and India. North America is currently the largest growing market.

Data Centre Mega-Deals Emerging as the New Growth Catalyst

Blackbox provides hyperscale and enterprise data centre solutions across various countries and continents. This includes building dense infrastructure, providing specialised capabilities such as high-speed networking and modular deployment models, implementing retrofits, and developing energy-efficient, AI-ready infrastructure.

The company aims to evolve from a transactional provider to a strategic partner for its data centre customers. To this end, the data centre vertical is one of five high-growth areas of BlackBox’s market entry strategy. Blackbox currently executes large-scale mandates for three of the top five hyperscalers worldwide. Hyperscaler means a large cloud service provider.

The company engages directly with major hyperscalers (such as Meta) for contracts at certain sites and geographies (e.g., Europe & the US). In addition, it also works with their large master contractors in other areas. To capitalise on the opportunity, the company is scaling strategically to capture data centre opportunities.

A Swelling Backlog Setting Up the March Toward the $2 Billion Vision

Black Box is currently building a specialised data centre AI services team in the U.S. that will focus on higher-value multi-hyperscaler engagements. A focused data centre team has been established in the last six months. Management is confident of securing $50 million to $100 million in orders within the data centre sector over the next five months of FY26.

BlackBox estimates that its data centre orders should represent around 20%-25% of its total order book. This means that, based on the company’s target of achieving a $1 billion order book in FY26, data Centre orders are expected to exceed $200 million.

In Q1 FY26, BlackBox secured two significant data centre orders in the US. Of this, one order was from a global hyperscaler and the other from a top-10 global core location provider. The company is also leveraging its global experience with hyperscaler clients to establish leadership in the Indian digital infrastructure ecosystem.

In addition, the recent strategic partnership with Wind River, a leader in intelligent edge software, is expected to accelerate edge and cloud innovation globally. This collaboration is highly strategic, as it fills a missing link (platforms) in Black Box’s portfolio and is crucial as more and more EDGE data centres, computing, and AI come into play.

This partnership is expected to generate about ₹13.5 billion in revenue over the next five years (about $30 million annually). Margins from this business are expected to be robust, with support and services margins projected at 25%-30%.

Its current order pipeline exceeds $2 billion, and it aims to achieve a total revenue of $2 billion by FY29. The company plans to achieve this through both organic and inorganic routes. Black Box plans to grow at about 15% annually, with an expected revenue target of around $1.2 billion. The rest will come from acquisitions in the $50–200 million range.

Robust Order Book Sets Stage for Stronger H2

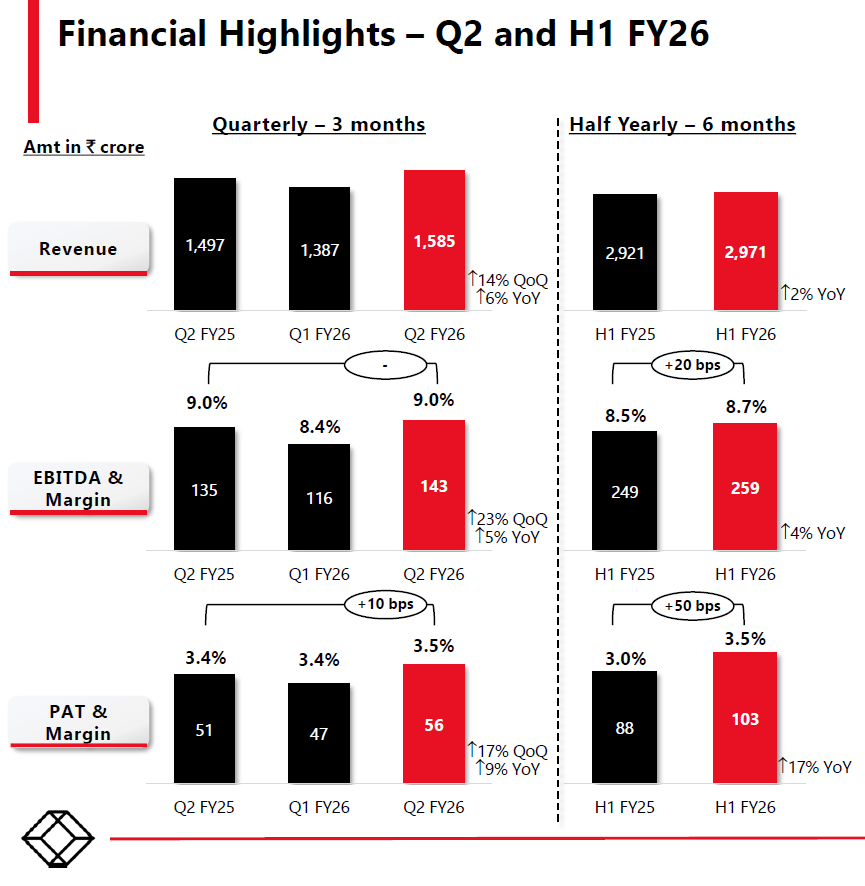

From a financial perspective, revenue from operations rose 6% year-on-year to ₹15.9 billion. Growth was impacted by clients’ delays in purchasing equipment due to the current tariff situation. EBITDA increased by just 6% to ₹1.4 billion, while margin stayed flat at 9%.

Black Box Financial Performance

PAT, however, rose 9% to ₹560 million. The total order backlog remained strong at $555 million in Q2 FY26 and is estimated to reach over $1 billion by the end of FY26. Blackbox continues to focus on attracting large-sized contracts and high-value customers. Management expects H2 of FY26 to be better than H1, supported by growing order books and strong execution momentum across geographies.

#3 E2E Networks: Turning Its Data Centre Network into a National AI Power Grid

E2E Networks is primarily an AI-focused hyperscale cloud platform. The company operates its cloud infrastructure through data Centres, providing services such as accelerated Cloud GPUs and managed hosting solutions. Within data Centres, E2E includes cloud computing services to Indian data Centres in Noida, Chennai, and Mumbai.

Scaling Up the Data Centre Footprint to Support AI Demand

Historically, E2E operations have been concentrated around Delhi-NCR. In 2019, the company established a new data Centre in Delhi-NCR and expanded GPU deployment. It maintains a total of 10 MW of data Centre IT power capacity and 3,900 GPUs. Recently, it added GPU capacity in Noida, which is operational and available for proof-of-concept and revenue generation.

Additionally, it has expanded into Chennai to strengthen its infrastructure presence across India and enhance regional latency for enterprise and AI workloads. E2E has deployed GPU clusters at Larsen & Toubro’s state-of-the-art data Centre in Chennai, with a capacity of 1,024 single large GPU clusters. This capacity comprises 20,000 GPUs, enabling future expansion as needed.

E2E views the Generative AI sector as a high-value niche that could grow into a $1.3 trillion market by 2032, positioning E2E as the backbone cloud platform for enterprises. E2E also intends to invest in NVIDIA Blackwell GPUs (such as B200 or B300/GB300 series) with capacity expansion potentially occurring in Q4FY26.

To this end, the company is in advanced stages of placing orders for nearly 2,048 Blackwell GPUs (mainly B200). Depending on demand, orders could double to 4,096 GPUs before March.

E2E’s Capacity Build-Out Pushes the Company Into Losses

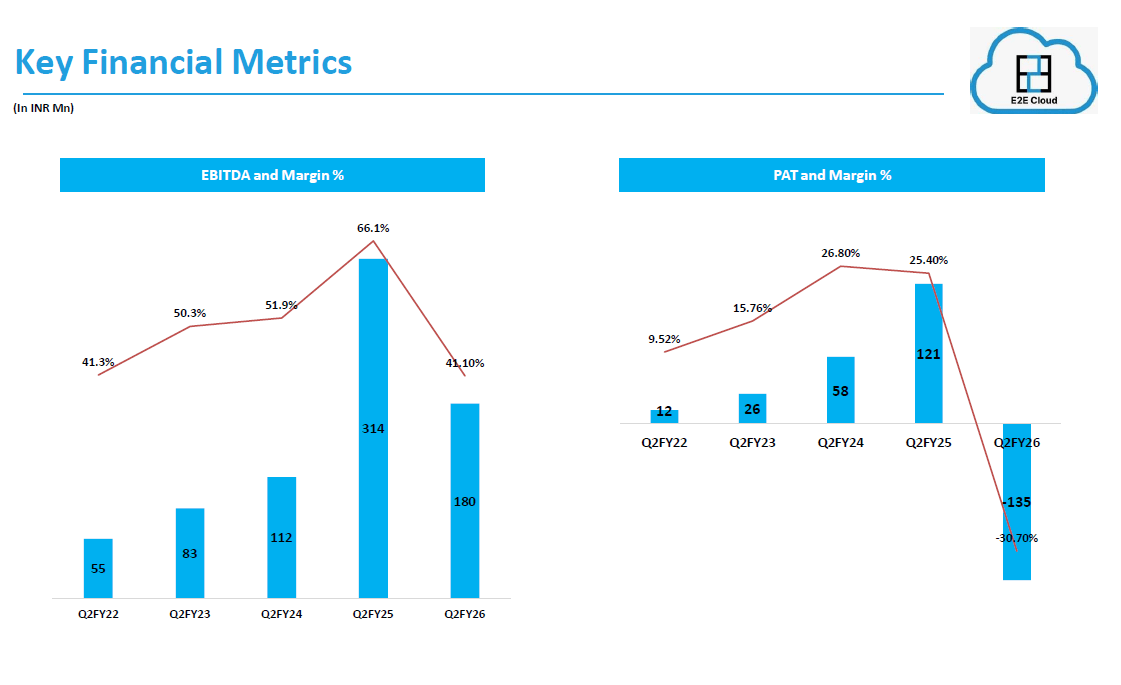

From a financial perspective, revenue declined 7.9% to ₹438 million in the first quarter of FY26. However, EBITDA decreased 42.7% to ₹180 million, while margins fell 25 percentage points to 41.1%. As a result, E2E swung from a profit of ₹121 million to a net loss of ₹130 million, mainly due to higher depreciation costs related to new facilities.

E2E Slips from Profit to Loss

Despite this, E2E reiterated its guidance for a monthly run rate (MRR) of ₹350-400 million by March FY26, primarily driven by two large orders (totalling ₹2.6 billion) from the IndiaAI mission. Long-term EBITDA guidance is set at around 70%, driven by operating leverage along with volume growth.

The exit MRR for the quarter ended September 2025 was ₹160 million, up from ₹145 million in the previous June quarter. After the IndiaAI mission orders, the company is targeting to increase the utilisation of existing infrastructure to 80%-90% by March, up from 35-40% in the previous quarter.

Valuations Telling Mixed Story

The growth story is undoubtedly strong, which is already factored into valuations.

E2E is currently trading at an inflated price-to-earnings (P/E) multiple of 512x, a figure that has shot up largely because the company recently slipped into losses (trailing twelve months is still profitable though). In contrast, the Blackbox valuation at 33x sits comfortably in line with both its historical median and the broader industry range.

Orient, at 29.6x, is also positioned close to the sector average. A historical comparison for Orient isn’t meaningful yet, given its short trading record.

Valuation- Comparison (X)

| Company | P/E | 5-Year Median |

| Orient | 29.6 | NA |

| Blackbox | 34.0 | 34.2 |

| E2E | 512 | 74.2 |

| Industry | 34.9 | |

While valuations appear in line, stakes are high. Any delay in execution or slower-than-expected demand could bring a knee-jerk reaction. This is pretty evident as all these first surged meaningfully recently, but have been on a downward trajectory since then.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.