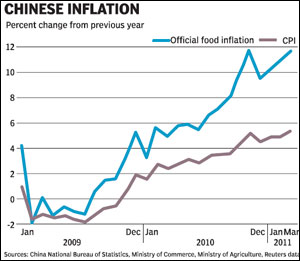

The wholesale price index rose an annual 7.48% in November, in line with analysts? forecast. The figure was lower than the annual rise of 8.58% in October.

All commodities

* WPI annual inflation rate slides in Nov to 7.48% from Oct 8.58%

* WPI inflation rate in Nov nearly flat vs economists? forecast of 7.50%

PRIMARY ARTICLES GROUP

* Primary articles month-on-month inflation rate 0.8% in Nov

* Primary articles annual inflation rate 13% in Nov, down vs 16.7% in Oct

* Food articles inflation rises in Nov 0.1% vs Oct

* Food articles year-on-year inflation 9.41% in Nov vs 14.1% in Oct

* Non-food articles month-on-month inflation rate 3.9% in Nov

* Non-food articles prices in Nov up 23.2% on year vs 22.2% rise in Oct

FUEL, POWER, LIGHT AND LUBRICANTS GROUP

FUEL, POWER, LIGHT AND LUBRICANTS GROUP

* Fuel group month-on-month inflation rate 0.3% in Nov

* Fuel group annual inflation rate 10.32% in Nov vs 11.02% Oct

MANUFACTURED PRODUCTS GROUP

* Manufactured products inflation rate rises 0.3% in Nov from month ago

* Manufactured products prices up 4.56% on yr vs 4.8% Oct

SEPTEMBER FINAL ESTIMATE

* WPI inflation in Sep revised up to 8.93% vs 8.62% provisional

EXPERTSPEAK

BRIAN JACKSON, senior emerging markets strategist, Royal Bankof Canada, Hong Kong

?Inflation is heading in the right direction, and today?s number is probably enough to keep the RBI on hold this week, in line with comments made by Governor Subbarao back in early November. However, Subbarao also noted last week that inflation is still above his ?tolerance level? and recent PMI survey data also suggest that price pressures may remain stubbornly high in the months ahead. This suggest that the RBI?s policy bias remains firmly in favour of more policy tightening, and we continue to expect more rate hikes in the new year.?

JONATHAN CAVENAGH, senior Fx strategist, Institutional Fx sales, Asia at Westpac Institutional Bank, Singapore

?The data came out largely as expected. The RBI will take some comfort from the continued slide in the year-on-year pace of wholesale price changes, although the outright level of close to 7.5% will still be deemed too high for comfort. This is unlikely to prompt any response from the RBI later this week but we do expect higher rates by Q2 of next year.?

MOHAN SHENOI, head of treasury, Kotak Mahindra Bank, Mumbai

?I expect December inflation to fall to 7% and 6.0-6.5% in March. With inflation trending lower, and liquidity tightness persisting, I expect RBI to be on pause mode till January. However, if energy prices rise and food prices remain sticky, inflation may not fall as much as RBI would want by March and therefore RBI may then hike rates in March.?

MANISH WADHAWAN, director and head of rates trading, hsbc India, Mumbai

?It is on expected lines and thus upholds the view that RBI may not hike rates day after tomorrow.It is too early to comment about the future rate hikes at this point but we are already seeing the transmission of policy rates in the form of high lending rates and high deposit rates, so the message is thus getting passed. The way things are, it is already hitting the system, so at this point to say whether RBI will hike rates post Dec. 16, it will depend on the data that is released in the interim.?

ANUBHUTI SAHAY, economist, Standard Chartered Bank, Mumbai

?The headline number is in line with expectation and reaffirms that RBI will adopt a wait and watch stance on Dec 16. It is encouraging to see a downward trend in headline as well inflation at sub indices level. However, upward revisions to past data and upward risk to commodity prices indicates that inflation risks still need to be watched out for. Thus while a status quo on rates is expected, the policy statement most probably will once again echo its vigilance on inflation.?

RUPA REGE NITSURE, chief economist, Bank of Baroda, Mumbai

?Inflation numbers looks comfortable but it is primarily because of the statistical base effect. We have seen over the past few weeks that pressure has been building up again both on the food and non-food inflation front. The current surge in demand will allow the manufacturing industry to pass on the cost increase to consumers thus having a cascading effect. ?Oil prices have been escalating, thus inflation risks continue. People?s expectations of inflation too are on the rise according to the recent survey of households conducted by the central bank.RBI thus needs to act in the interest of inflation management and I expect them to raise rates by 25 basis points each on Dec. 16. They should not get too swayed by the current tight liquidity conditions as it is going to ease in the fourth quarter.?

RVS SRIDHAR, president and head of markets in treasury, Axis Bank, Mumbai

?I don?t expect this number to have any relevance on the policy. Market will continue to expect RBI to remain on a pause mode in this policy. But the fact that the index is rising proves that inflation is high.?

NAMRATA PADHYE, economist, IDBI Gilts, Mumbai

?The reading on inflation should reiterate market expectations for a pause at the upcoming policy review. Tight liquidity is aiding the monetary transmission, as was expected by RBI but liquidity deficit beyond the comfort level is a concern. I expect the liquidity to ease to some extent on RBI measures and bond redemptions by end of January but liquidity would still remain in considerable deficit unless stronger measures are adopted.?

SUJAN HAJRA,chief economist, Anand Rathi Securities

?In the next three month inflation level will further go down as food prices have started softening though not to a great extent. I expect RBI to achieve its inflation target of 6% for this fiscal year ending March. I don?t expect RBI to hike rates on Dec 16 and in its Jan 25 policy. Moreover, if inflation continues to be at lower level and liquidity remains tight there may be no further rate hikes this fiscal year. The gap between CPI and WPI is expected to narrow as food inflation which has higher weightage in CPI has started falling.?

JOYDEEP SEN, vice-president (fixed income), bnp Paribas Wealth Management

?The data has come in line with expectations. It is not a surprise.We do not see RBI hiking rate at its Dec 16 policy but there are expectations of a concrete measure like a cut in cash reserve ratio to ease liquidity tightness. Seeing this number, RBI should more or less be able to meet its 6% target for inflation by end March.?

SHUBHADA RAO, chief economist, Yes bank

?The tight liquidity is serving the purpose and the effect of tightening is already underway. We do not expect the liquidity to ease significantly in January and may be through February. It is also unlikely that the RBI will hike rates in the December and January policy meets. There are upside risks to the 6% trajectory of inflation put forth by RBI. The commodity prices have firmed up and primary articles have not eased as anticipated. So perhaps RBI will revisit the inflation target in the January policy meet. The likely diesel price hike may add another round of pressure on prices. Without a diesel price hike at this point in time we see inflation at 6.2% for 2010-11 (Apr-Mar).?