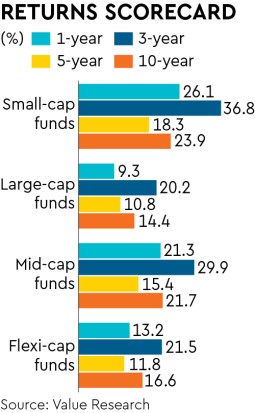

Retail investors are betting big on small-cap funds as the category constitutes more than 50% of net inflows of actively managed equity fund categories. They should now preferably deploy money in these funds in a staggered manner through systematic investment plans (SIPs) or systematic transfer plans (STPs) and avoid lumpsum investments as valuations are turning expensive and the Nifty Smallcap 250 Index is at its all-time high.

As the Nifty Smallcap 250 Index has given returns over 30% returns since April this year, there has been a surge in small-cap fund inflows as a result of this strong performance. While small-cap funds can work better for investors with a long-term perspective, they must be watchful of the volatility. Moreover, investors must not go overboard on small-cap funds as these can have an impact on the overall portfolio and a blended approach will work well for all times.

Arun Kumar, VP and head, Research, FundsIndia, says despite the recent run-up, investors can continue their SIPs provided they have at least a seven-year time frame. “However, if you are planning to deploy large sums of money as lumpsum, the valuations are on the higher side and you might want to stagger the same via a 6-12 month weekly STP,” he says.

Nirav Karkera, head, Research, Fisdom, says amid a run-up in small-cap indices certain pockets might be expensive. However, there are still enough opportunities in the underinvested and under-researched segments. “While the recent run-up in stocks has been notable, investors should deploy money in small-cap funds in a staggered manner. STPs and SIPs are the preferred ways to invest in them,” he says.

Highly volatile

Small-cap segment tends to have higher volatility. For example, during the 2008 global financial crises, the Nifty Smallcap 250 index fell up to 76% and reached its previous peaks only after six years in September 2014. Similarly, post the 2018 sell-off, the Nifty Smallcap 250 index took three years to reach its previous peaks.

Investors need to have a high-risk appetite and a seven-year plus time horizon to invest in small-cap funds. Karkera says small-cap stocks are not suitable for risk averse investors seeking linearity in performance. “Investors should pick funds with a strong track record and an experienced fund manager,” he says.

Tread with caution

Investors must note that revenues and profits of small-cap companies fluctuate more than large-cap companies because of lower ability to withstand market downturns. Investors must identify funds that have drawdown protection and see if the fund manager has many funds to manage which could lead to liquidity being shared across funds. It will be prudent to go with a small-cap fund where the fund manager has had a long tenure managing the fund. Investors with a low to moderate risk appetite should limit their allocation to small-caps at around 5% and those with a longer horizon and higher risk appetite can go for a higher allocation.

Abhishek Banerjee, founder & CEO, Lotusdew Wealth and Investment Advisors, says investors should look at the quality and consistency of returns to ensure that outperformance is due to the stock selection and not so much due to cash calls or off-benchmark bets. “An easy way to do this is to run a regression analysis on the returns against different market indices to see which indices most explain their return pattern,” he says.

Small-caps target companies ranked from 251st company and below. A fund manager has to invest at least 65% of money in these companies to qualify for a small-cap fund. Akhil Bhardwaj, senior partner, Alpha Capital, a registered investment advisor, says when the swings are higher, the risk-bearing capacity of investors should be high. “To mitigate that risk, investors might have to stick with a small-cap strategy for a longer term as compared to other equity categories. There is still enough steam left in small-caps to deliver excess return but still cautious play is advisable by investing in the staggered manner,” he advises.