The new pharma playbook for FY27

India, or as many like to call it, the pharmacy of the world, has been at the centre of the world’s attention for some time now. As the world’s biggest provider of generic drugs, known for affordable vaccines and high-quality medicines, the Indian pharmaceutical industry is currently ranked 3rd in terms of pharmaceutical production by volume.

The heavyweights of the Nifty Pharma index grapple with the tightening noose of USFDA scrutiny and eroding margins. The era of “growth at any cost” has ended and is replaced by a ruthless investor preference for capital efficiency and predictable earnings.

At such a time, two outliers have caught the attention of investors thanks to their surgical precision in operations. These are specialized players that have turned Return on Capital Employed (ROCE) into a competitive moat. Plus, they possess a rare commodity to have in today’s markets – Consistency.

While the big companies report inconsistent recovery curves, these two companies have logged uninterrupted profit growth for consecutive quarters. For investors looking toward FY27, these stocks hold merit to find a place in a watchlist.

Ajanta Pharma: The 32% ROCE specialist dominating niche therapies

Incorporated in 1979, Ajanta Pharma is primarily engaged in development, manufacturing and marketing of speciality pharmaceutical quality finished dosages.

With a market cap of Rs 36,855 cr as on 9th March 2026, the company is focused on niche and first-to-market drugs in 4 therapeutic areas – cardiology, ophthalmology, dermatology, pain management.

The company has a current ROCE (Return on Capital Employed) of 32%, which is more than double than the current industry median of 15%. In simple words, Ajanta generates a profit of Rs 32 on every Rs 100 it uses as capital, while its peers average about Rs 15.

The 5-year average ROCE of the company is also an impressive 30%, while the industry median for the same period is 17%, which speaks volumes of how the company has managed to deliver sustained capital efficiency.

It also has a current dividend yield of close to 1% while the industry median is just around 0.1%.

Let us look at the core financials of the company to see if it has what it takes keep up these figures.

The sales of the company grew from Rs 2,588 cr to Rs 4,648 cr between FY20 and FY25, which is a compound growth of 12%. And for the first 3 quarters of FY26 (ending December 2025), the company has logged sales of over Rs 4,000 cr already.

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) went from Rs 683 cr in FY20 to Rs 1,269 cr in FY25, which is a compound growth of 13%. And for the 3 quarters of FY26, the EBITDA logged is Rs 1,061 cr.

Looking at the net profits, the company has logged compound growth of 14% from Rs 468 cr in FY20 to Rs 920 cr in FY25. What has caught the attention of the smart investors, is the quarter-on-quarter growth the company has logged between December 2024 and December 2025.

| Year | Dec 2024 | Mar 2025 | Jun 2025 | Sep 2025 | Dec 2025 |

| Profits/Rs Cr | 233 | 225 | 255 | 260 | 274 |

The generic giant

This impressive profit growth was driven by a double-digit surge in US generics revenue and a significant 260-basis-point expansion in gross margins, which reached 79% through an optimized, high-value product mix. And this momentum was reinforced by strong performance in India’s chronic therapy segments, backed by disciplined operational leverage that successfully absorbed higher R&D and personnel costs.

By focusing on limited competition launches and specialized domestic brands, Ajanta delivered a robust bottom-line despite temporary shipment timing lags in its Asian markets.

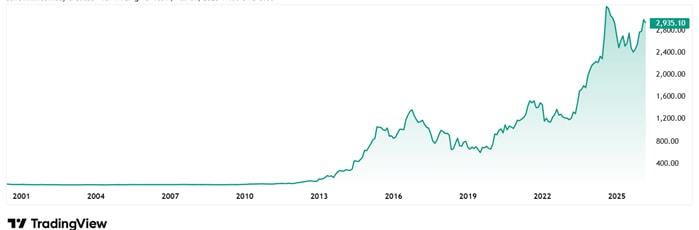

The share price of Ajanta Pharma Ltd was around Rs 1,220 in March 2021 and as on 9th March 2026 it was Rs 2,950, which is over a 140% jump in 5 years.

Regarding the valuation, the stock is trading at a PE of 36x which is more than the current industry median of 28x. Which means that the market is willing to pay a premium to own a piece of Ajanta.

Ajanta Pharma with superior capital efficiency and an almost debt-free balance sheet, probably justifies its valuation premium over the industry median. However, investors should weigh this growth against a steep price-to-book ratio of over 8x, and a high cash conversion cycle driven by elevated inventory levels.

While the core fundamentals are sturdy, recent minor promoter pledging and volatility in Asian shipment timings serve as reminders that even the most efficient performers require a watchful eye on execution risks and valuation comfort.

Torrent Pharmaceuticals: Why markets pay a scarcity premium for chronic revenue

Incorporated in 1972, Torrent Pharmaceuticals Ltd is one of the leading Indian Pharmaceutical companies engaged in research, development, manufacturing and marketing of generic pharmaceutical formulations.

With a market cap of Rs 1,45,181 cr the company is the flagship company of Torrent Group which also has presence in power and city gas distribution businesses.

The company has a current ROCE of 27%, which is higher than the current industry median of 15%. Add to this the company’s low debt status, giving them the freedom to use the profits to grow, without having to worry about hefty interest payments.

Looking at the financials of the company, the sales of the company jumped from Rs 7,939 cr in FY20 to Rs 11,516 cr in FY25, recording a compound growth of 8%. And for the first 3 quarters of FY26, sales of Rs 9,783 cr have been logged.

The EBITDA jumped from Rs 2,170 cr in FY20 to Rs 3,721 cr in FY25, which is a compound growth of around 12%. And between April and December 2025, the EBITDA logged is Rs 3,203 cr.

The net profits grew at a compound rate of 14% from Rs 1,025 cr in FY20 to Rs 1,911 cr in FY25. And just like Ajanta above, Torrent too has logged impressive sustained QoQ profit growth.

| Year | Dec 2024 | Mar 2025 | Jun 2025 | Sep 2025 | Dec 2025 |

| Profits/Rs Cr | 503 | 498 | 548 | 591 | 635 |

The chronic moat: Why sticky patient adherence protects torrent’s margins

The company achieved this by strong operating leverage and a high-margin revenue mix. While consolidated revenue remained largely flat, the bottom line expanded to Rs 635 cr as total operating expenses declined. This margin accretion was supported by sustained outperformance in the domestic chronic segment, plus robust growth in the U.S. and Brazilian branded markets.

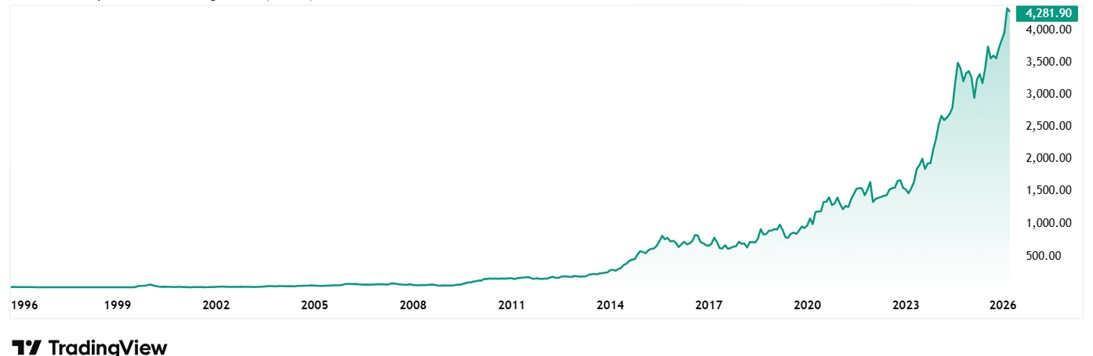

The share price of Torrent Pharmaceuticals Ltd was around Rs 1,230 in March 2021 and as on 9th March 2026 it was Rs 4,290 which is a jump of almost 250%.

The valuation verdict: High stake bets on flawless execution

As for valuations, the company’s stock is trading at a PE of 63x, which is more than double the current industry median of 28x.

This high valuation is anchored by a dominant 76% revenue share from domestic chronic therapies, which offer superior pricing power and sticky patient adherence compared to volatile export markets. Also, the market is pricing in the high-accrual synergies from the JB Chemicals acquisition and a robust pipeline of complex molecules like GLP-1s.

However, with that high valuation, the company offers a thin margin of safety. Also, any friction in integrating JB Chemicals or a regulatory setback in the complex generics pipeline could lead to a sharp valuation derating. Investors are essentially paying a steep scarcity premium for the company’s high margins and chronic-market dominance. At these levels, the stock is less of a value play and more of high stakes bet on flawless execution.

The FY27 Outlook: Pricing flawless execution in a premium market

In an industry often distracted by the sheer scale of global exports, Ajanta and Torrent have proven that the most lucrative path forward lies in surgical precision rather than raw volume. Their ability to maintain sector-beating returns on capital suggests that moats in the modern pharmaceutical landscape are no longer built solely on R&D budgets, but on the ability to extract maximum value from every rupee deployed.

However, for investors eyeing the FY27 horizon, the central question shifts from performance to price. With valuations trading at significant premiums to the industry median, the market has already priced in a future of near-flawless execution.

Whether these outliers can continue to outpace their peers will depend on their ability to navigate thinning margins of safety and the perpetual shadow of regulatory scrutiny. A good idea would be to add these stocks to a watchlist and keep an eye on them.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.