")

According to the Ministry of New and Renewable Energy, India has reached 100 gigawatts (GW) of total solar photovoltaic (PV) module manufacturing capacity. However, renewable energy sources like solar or wind power generate electricity only when sunlight or wind is available. This creates challenges in maintaining grid stability and meeting power demand around the clock.

This is where the need for Battery Energy Storage Systems (BESS) comes in. BESS stores excess electricity and releases it when needed, making it a critical component. As penetration of green energy increases, the demand for BESS is expected to increase as India aims to reach 500 GW of renewable energy by 2030.

To support this, it aims to achieve 74 GW of BESS capacity by 2031-32, up from the current 205 MW installation. This creates a big market potential for companies in the sector. The government has also recently provided viability gap funding (VGF) of ₹54 billion to build BESS systems with a capacity of 30 GW. This will result in an estimated investment of ₹330 billion.

Three solar companies have already received orders, with more expected.

#1 Tata Power: The Utility King Pivot to Storage

Tata Power, a part of the Tata Group, is India’s largest vertically integrated power company. It operates in the areas of new-age energy solutions, power generation, renewable energy, and transmission and distribution.

Tata Power Leads with India’s First Standalone BESS Agreement

The company has a total generation capacity of 26.3 GW, a transmission capacity of 4,659 circuit kilometres, and an integrated cell and module manufacturing capacity of 4.9 GW. BESS is one of the sectors Tata Power plans to leverage to create the ‘Utility of the Future’. This strategic area also includes Smart Grids, Green H2, robotic panel cleaning, and SMR (Small Modular Reactors).

Tata Power, through its subsidiary Tata Power Renewable Energy, has signed the first agreement in the standalone BESS segment, with NHPC for the Kerala State Electricity Board. The project involves setting up a battery storage system with 120 megawatt-hours (MWh) of capacity and is targeted for completion in 15 months.

This is part of NHPC’s broader initiative to develop 500 MWh of standalone battery storage capacity in Kerala, supported by viability gap funding. This initiative supports the government of India’s goal of achieving 500 GW of non-fossil fuel capacity by 2030. The minimum e-reverse auction tariffs for Storage were ₹3.6/kWh in H1 FY26.

Strengthening Mumbai’s Power Resilience

Apart from this, the company is also looking to aggressively expand its BESS capacity. The company plans to install 100 MW BESS with load centres at 10 locations in Mumbai in the next two years. It will be installed in metros, hospitals, and data centres to ensure an uninterrupted power supply.

Tata Power also plans to develop 2.8 GW of pumped storage capacity, which is expected to be commissioned by August 2028. An additional 1.8 GW of capacity is expected to be commissioned by 2030. It is also upgrading the electronic charging platform, Easy Charge, to support 10-fold growth over the next five years.

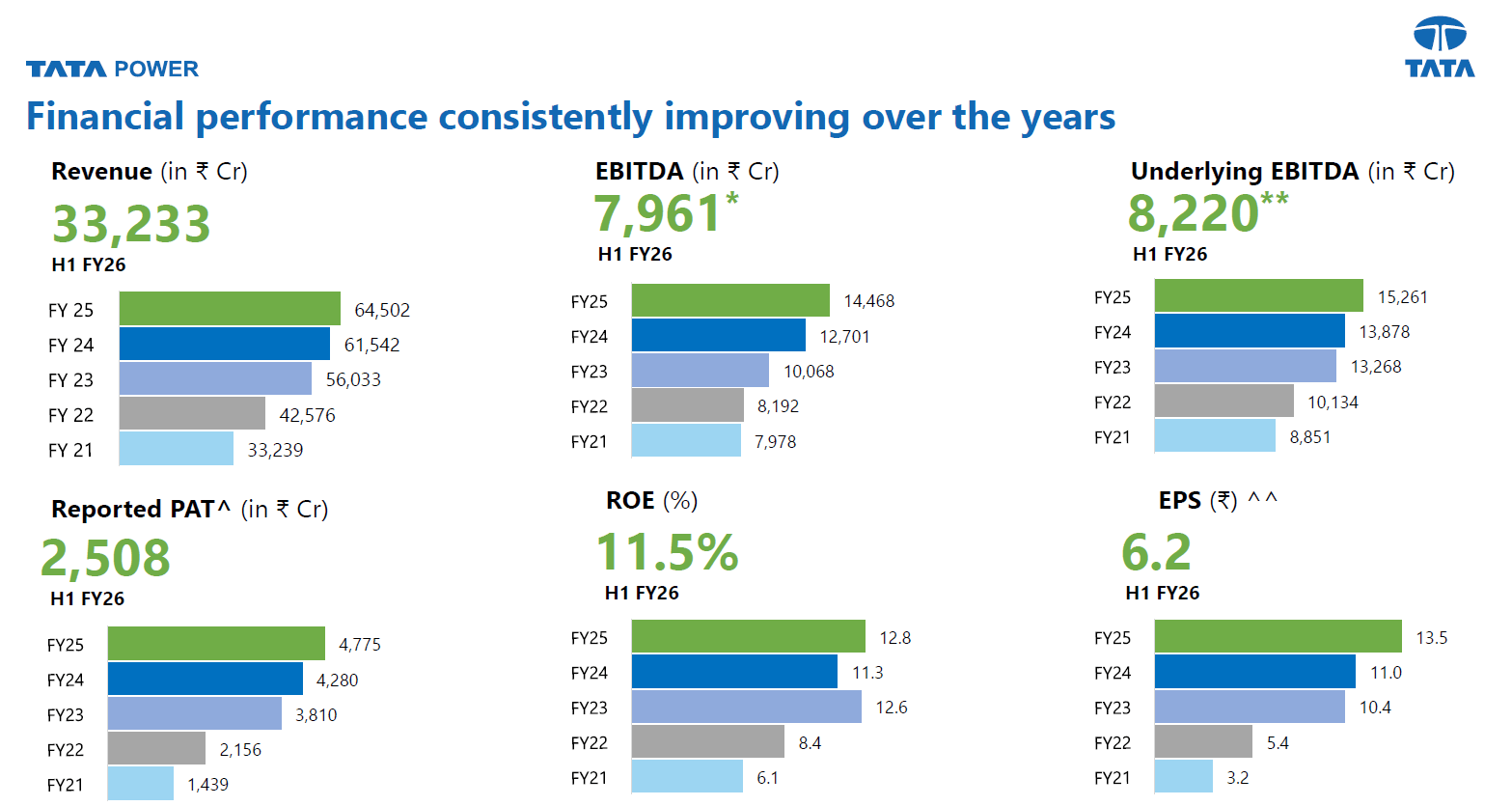

Stable Financial Performance

Now, looking at the performance for the first six months of FY26, revenue grew 3.7% year-over-year to ₹332.3 billion. This growth was driven by improved performance in the distribution, solar manufacturing, and solar rooftop businesses.

Tata Power Financial Performance

Operating performance also remained strong, with EBITDA (earnings before interest, tax, depreciation and amortisation) increasing 11.2% to ₹79.6 billion. Profit after tax (PAT) increased 9.9% to ₹25.1 billion, while margins expanded 40 basis points (bps) to 17.5%.

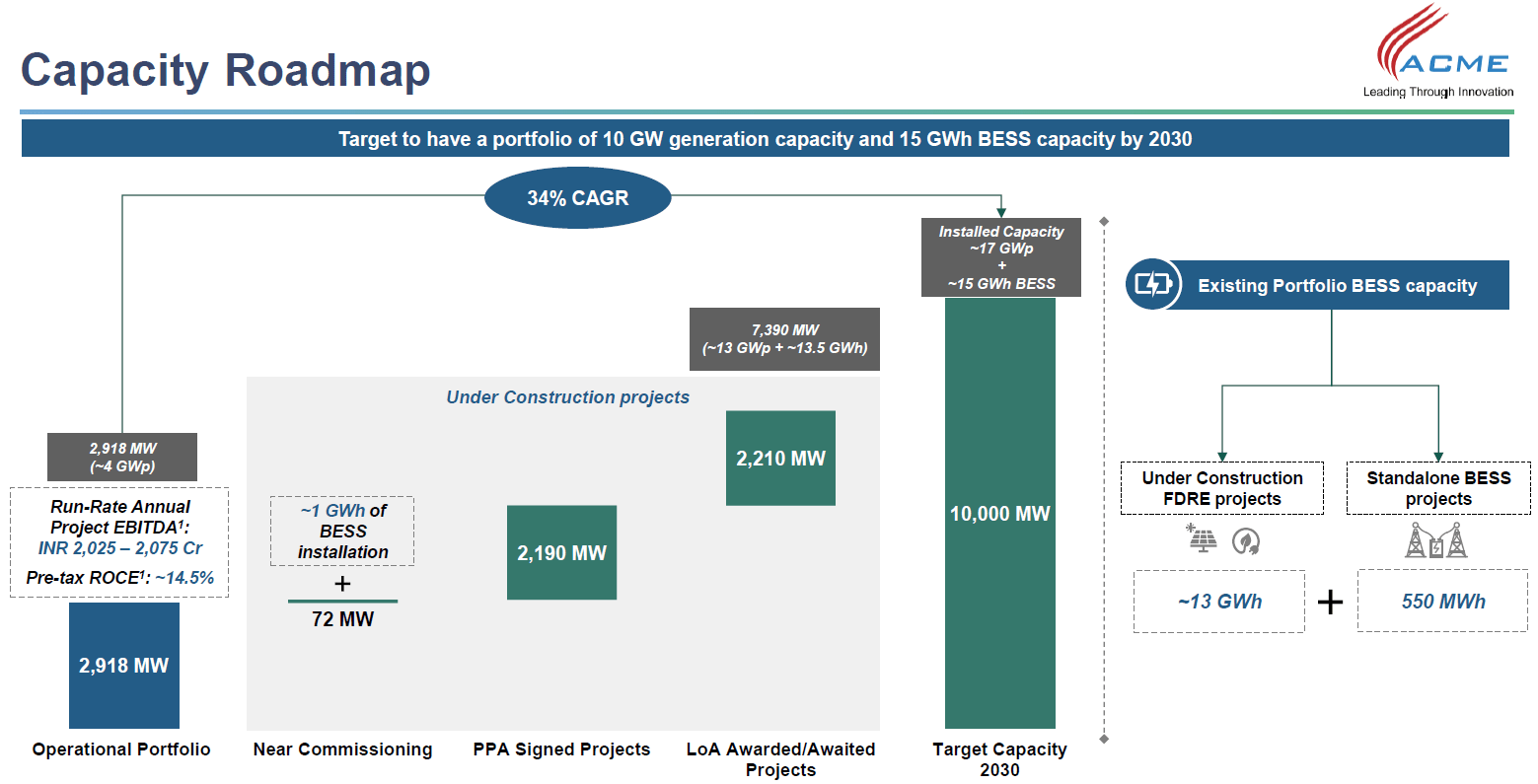

#2 Acme Solar: The Pure-Play BESS Bet with 13.5 GWh Ambitions

Acme Solar is one of the largest independent power producers in renewable energy. It has a portfolio of 7.4 GW spanning solar (43%), wind (2%), storage, hybrid and other projects (55%). In addition, the company also has 550 MWh of standalone BESS capacity.

Acme’s Expanding Renewable Portfolio

Of this, 2.9 gigawatts (GW) is already operational, power purchase agreements (PPAs) have been signed for another 5.2 GW, and letters of award (LOAs) have been issued for an additional 2.2 GW. These contracts provide long-term stable cash flows contracted through a 25-year PPA at fixed tariffs with government-backed entities.

Acme has a diversified portfolio, with over 85% contracted to central offtakers, spanning new-age technologies such as Fully Dispatchable Renewable Energy (FDRE) and hybrid technologies. The majority of Acme’s operating portfolio is located in states with high resource potential.

Building Scale in Battery Storage

The company is building BESS as a core part of its portfolio. ACME Solar’s total capacity stands at 7.4 GW, supported by 13.5 GWh of planned battery storage. Of this, 4.5 MW/13.5 GWh is already under construction, and the roadmap shows an existing storage pipeline of 13 GWh.

To this end, the company has placed big orders for BESS equipment, with installation scheduled to begin soon. ACME Solar placed an additional 2 GWh BESS order from leading global energy system suppliers in Q2 FY26, taking the total BESS ordered capacity to 5.1 GWh as of Q2 FY26.

The first phase of BESS delivery is scheduled to begin in December 2025 onwards. Phased commissioning of this ordered capacity is expected to commence in Q4 FY26. BESS is primarily utilised in Firm and Dispatchable Renewable Energy (FDRE) and standalone configurations, and is also leveraged for merchant operations.

The company plans to operate about 1 GWh of BESS on a merchant basis starting in Q4 FY26. This merchant operation is expected to deliver upside potential of around ₹1.7 billion in annual EBITDA, assuming an ₹5 difference between merchant power sold during peak hours and production costs.

To optimise future large-scale installations, ACME Solar operationalised a pilot BESS project. A 10 MWh BESS pilot project was operationalised in Rajasthan in October 2025, specifically for FDRE/Solar+BESS projects. An Energy Management System was also commissioned to automatically control BESS operations.

Acme Capacity Roadmap

Acme is targeting 10 GW of generation capacity and 15 GWh of BESS capacity by 2030. They will be tied to 15-year service agreements with their BESS vendors. These agreements include an annual maintenance fee and mandate on-ground personnel and reserves to guarantee specified availability and round-trip efficiency.

A Strong First-Half Performance

Acme reported a stellar performance in H1 FY26. Total revenue grew 86.6% year-on-year to ₹11.8 billion, driven by capacity additions and higher capacity utilisation. EBITDA grew 90.7% to ₹10.6 billion due to operating leverage, while margins expanded by 190 bps to 89.8%. As a result, PAT also grew sharply, rising from ₹170 million to ₹2,460 million.

#3 Bondada Engineering: The High-Growth EPC Capture

Bondada undertakes design and Engineering, Procurement, and Construction (EPC) work for the telecom, railways, and renewable energy sectors. It also provides operations and maintenance services to telecom service providers.

Its clients include Vodafone Idea, Airtel, Tata, Ericsson, Reliance Jio, NTPC, and Coal India. The company has also ventured into battery storage divisions under the build-own-operate model.

Bondada Steps Into Large-Scale Battery Storage

The company is positioning itself to be a BESS EPC player for various Public Sector Companies that are undergoing power transition. It is considered part of the larger 21 GW capacity that it aims to execute in the EPC model, distinguishing it from the capital-intensive IPP model.

Bondada partners with technology providers to supply batteries for eco-friendly storage solutions. Current tenders are often for build, operate, and own (BOO) contracts, which typically last 12-14 years. To this end, the company holds a 400 MWh contract structure on a BOO basis for the next 12-14 years. The company also plans to offer BESS O&M services.

A Longer-Term Revenue Model Takes Shape

The current BESS order book is about ₹8.5 billion. BESS is grouped with Solar EPC and IPP under the Renewable Energy segment, which collectively accounts for ₹45.7 billion of the total order book (₹59.9 billion) as of 28 October 2025. The order book provides over 3 years of revenue visibility.

Bondada states that BESS projects typically take 15 to 18 months to set up, including AC and DC design and cell imports. The company’s current contract is running on an 18-month timeline, which could be reduced to 12 to 15 months as the Indian BESS ecosystem improves. Also, it estimates the cost of 1 GWh of BESS at around ₹2.5-3.0 billion.

This creates a revenue potential of approximately ₹25-30 million per megawatt hour (covering both AC and DC sides). On the margin side, the BOO model provides annuity income with a target internal rate of return of 16-17% for the current project, which is expected to stabilise at 13-14% in the future. Meanwhile, EPC project margins are 12-13%.

It plans to further scale its BESS Independent Power Producer capacity, intending to establish 2 GW capacity BESS across India over the next 2-3 years under the BOO model. The company has an ambitious target of achieving revenue of ₹100 billion by FY30. By then, it plans to have a portfolio of solar EPC (6 GW), BESS (2 GW), and solar independent power producers (2 GW). Of this, 2 GW of solar EPC is currently under construction.

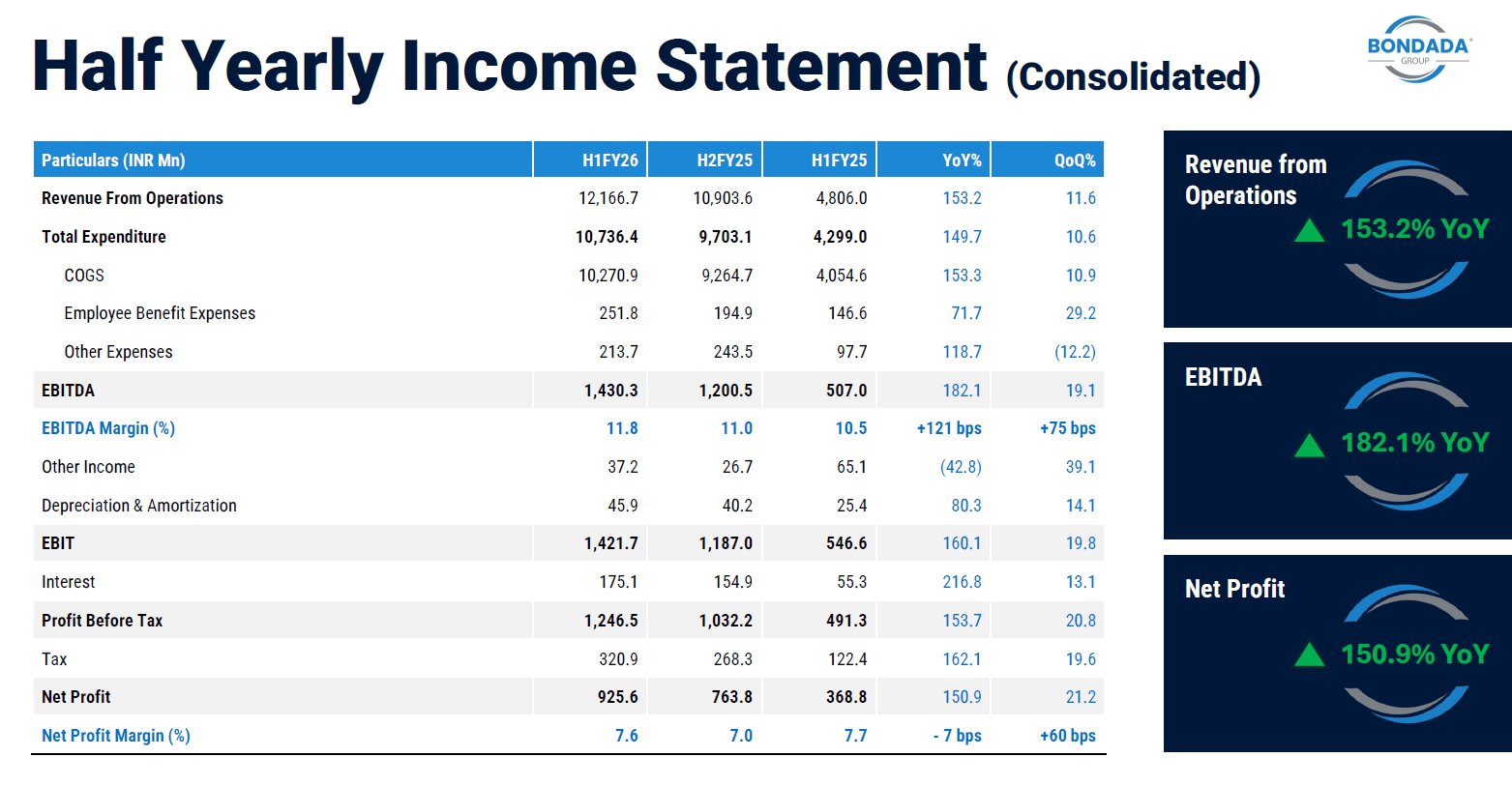

Momentum Builds in First-Half Performance

Now coming to its financial performance, revenue increased by 153% year-on-year to ₹12.2 billion in the first half of FY26. In the revenue mix, about 78% revenue came from renewable energy, followed by telecom (14%), and product manufacturing (8%). EBITDA increased by 182% to ₹1.4 billion, driven by operating leverage, while margin rose 121 bps to 11.8%. PAT, on the other hand, rose by 150.9% to ₹926 million.

Bondada Strong Financial Performance

Bottomline

In terms of valuation, both Acme and Tata Power are trading close to the industry EV/EBITDA, with Tata Power also near its 3-year median valuation. Bondada, on the other hand, trades at a higher valuation than the industry but below its 2-year median valuation. Both Acme and Bondada are new listings, so long-term data is not available.

Valuation Assessment (X)

| Company | EV/EBITDA | 3-Year Median | Industry |

| Tata Power | 11.7 | 11.1 | 12.6 |

| Acme Solar | 12.3 | NA | 10.5 |

| Bondada | 15.8 | 41.4 (2Y) | 9.3 |

That said,with India accelerating its renewable energy transition, battery storage is emerging as a crucial piece of the puzzle. Government support and growing demand have opened up a strong growth runway for players like Tata Power, Acme Solar, and Bondada Engineering.

While Tata Power offers scale and stability, Acme brings innovation in dispatchable energy. As the energy landscape shifts, these companies are well-positioned to benefit from rising adoption of BESS solutions in the years ahead.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.