Rural demand in India has strengthened over the past few months. FMCG consumption in villages and small towns has grown faster than in cities.

In the three months ended September, rural volume growth stood at 7.7%, compared with 3.7% in urban markets, according to data from NIQ. This points to a clear shift in demand towards rural areas.

The wider rural economy has also shown improvement.

Consumption, incomes and investment picked up in late 2025 after a key tax reform and easing inflation. As per NABARD’s Rural Economic Conditions and Sentiments Survey November 2025, 79.2% of rural households increased their spending so far in FY26, up from 76.2% in the previous round.

This makes the current phase worth noticing.

Demand recovery is no longer limited to basic needs. Spending is gradually spreading to mobility, housing upgrades and discretionary items. Balance sheets across sectors are cleaner. Credit availability has improved. Together, this creates a more supportive environment for long-term investing.

The stock selection was deliberately limited using measurable operating and financial cut-offs to avoid a broad rural theme. Only companies showing visible rural traction in recent reported numbers were considered.

In addition, each stock had to clear at least one financial quality filter, either through strong balance-sheet protection, such as net-cash positions or capital adequacy buffers around regulatory comfort levels, or through valuation discipline, where current trading multiples were aligned with or below long-term historical averages unless supported by clear operating recovery.

Applying these filters eliminated many rural-facing names that lacked either visible demand traction or financial resilience, resulting in a focused four-stock selection where rural exposure is already reflected in data and downside risks are quantitatively contained.

#1 Hindustan Unilever: Navigating the GST transition

Hindustan Unilever is in the FMCG business comprising primarily home care, beauty & personal care and foods & refreshment segments. The company has manufacturing facilities across the country and sells primarily in India.

Consumer Staples: Navigating policy and tax shifts

Hindustan Unilever posted a soft set of numbers in the September quarter of FY26, with tax changes and temporary demand disruption weighing on volumes.

Sales for the quarter stood at Rs 16,241 crore up only 2% year-on-year (YoY). Sales growth was driven largely by pricing, while volume growth remained muted.

The quarter was impacted by GST rate rationalisation announced in early September. Close to 40% of the company’s portfolio shifted to the 5% tax slab. The benefit was passed on across more than 1,200 products. This led to trade destocking and some postponement of purchases, particularly in personal care and packaged foods.

Margins came under pressure as the company stepped up spending on brands and promotions. Net profit rose 4% in Q2 FY26 to Rs 2,694 crore due to a one-time tax benefit.

Management said demand conditions have begun to stabilise from November and expects a better performance in the second half as the impact of tax changes fades and inflation remains benign.

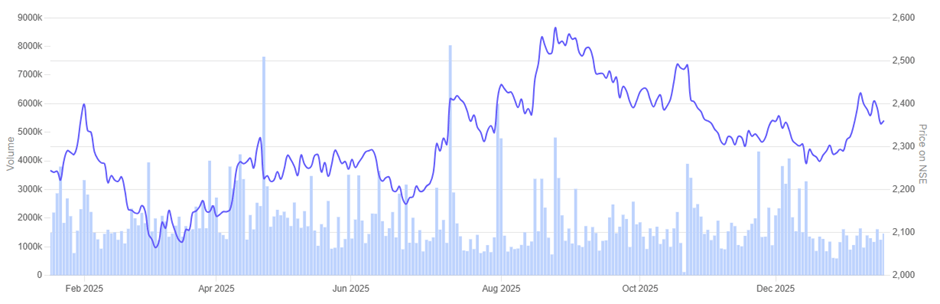

In the past year, Hindustan Unilever share price is up marginally 0.7%

Hindustan Unilever 1 Year Share Price Chart

#2 Mahindra and Mahindra: A rural surge powered by tractors

Mahindra & Mahindra is one of the most diversified automobile companies in India with presence across 2-wheelers, 3-wheelers, PVs, CVs, tractors & earthmovers. Its subsidiaries span other businesses including real estate, technology and financial services.

Industrial Mobility: The tractor-led recovery

Mahindra & Mahindra reported a strong September quarter in FY26, helped by improvement in rural demand. During the quarter, consolidated revenue grew 22% YoY to Rs 46,106 crore. Net profit rose 28% YoY, to Rs 3,964 crore after adjusting for one-offs.

The farm business led the performance. Tractor volumes increased 32% during the quarter compared to the same period in the previous year. Better farm incomes and cash flows supported demand. Profit from the segment rose 54%. Margins stayed above 20%. Revenue from farm machinery was around Rs 330 crore, reflecting higher use of mechanisation.

The auto business also saw growth. Revenue rose 25% YoY. SUV volumes grew 13%. September saw some disruption due to GST changes, but demand held up. Exports increased by nearly 40%. Electric vehicles made up 8.7% of total volumes.

Management said demand trends remain stable and expects the second half to be better, supported by easing inflation and steady rural spending.

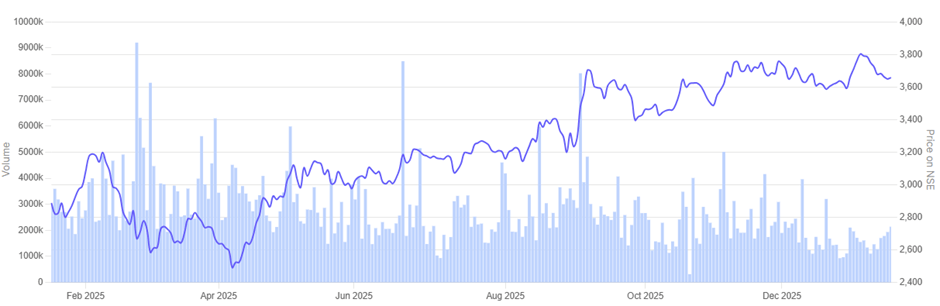

In the past year, Mahindra & Mahindra share price rallied 26.7%

Mahindra & Mahindra 1 Year Share Price Chart

#3 Finolex Industries: Shifting towards Non-Agri stability

Finolex Industries (FIL) is a leading manufacturer of PVC Resin and the largest producer of PVC Pipes & Fittings in India. The company offers the latest range of superior quality and durable PVC-U pipes and fittings used in agriculture, construction and industrial operations. Its product portfolio consists of two major divisions: PVC Resin and PVC Pipes & Fittings

Strategic diversification: Transitioning beyond agriculture

Finolex Industries turned in a mixed performance in the September quarter of FY26. Sales volume declined 6% to 65,336 tonnes. Revenue from operations still rose 4% to Rs 859 crore, supported by better pricing.

Margins improved sharply during the quarter. Higher contribution from non-agri products and improved gross margins helped profitability. Net profit increased to Rs 119 crore, up 133% from a year ago.

The non-agriculture segment remained steady. Volumes in this segment grew 7%, while agri demand stayed weak due to excess rainfall. Non-agri products now form 44% of total volumes. This shift helped offset pressure from lower agri sales. Installed capacity stands at 5.2 lakh tonnes, with utilisation at around 70%.

The company continues to carry a strong balance sheet, with net cash of about Rs 2,360 crore. Management expects demand to improve in the second half as monsoon-related disruption eases and infrastructure activity picks up.

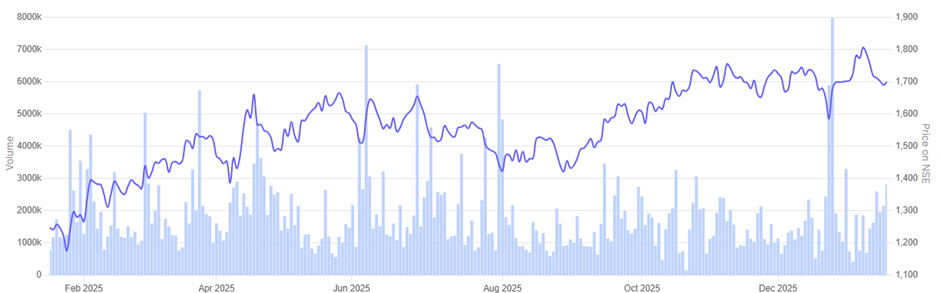

In the past year, Finolex Industries share price tumbled 16%

Finolex Industries 1 Year Share Price Chart

#4 Cholamandalam investment and finance company: Balancing credit growth with asset quality

Cholamandalam Investment & Finance Company is one of the premier diversified non-banking financial services companies in India, engaged in providing vehicle finance, home loans and Loan against property.

The NBFC reported steady growth in the September quarter of FY26. Total income increased to Rs 7,590 crore, up 21% from last year. Net profit rose 20% to Rs 1,155 crore. Assets under management crossed Rs 2.1 lakh crore, reflecting continued loan disbursements during the quarter.

Rural Credit: Lending to the next billion

Most of the growth came from vehicle finance. Sales of used vehicles, tractors and small trucks held up well in villages and smaller towns. MSME and property-backed loans also moved up as the company added more branches. Net interest margin improved to 7.9%, helped by stable borrowing costs.

Asset quality remained under watch. Gross NPA stood at 4.5% at the end of the quarter up 79 basis points from a year ago. Capital adequacy stayed comfortable at around 20%, providing a cushion for growth. Liquidity remained adequate.

Management said growth will remain measured in the coming quarters. The focus will be on credit quality and disciplined underwriting as loan demand normalises.

In the past year, Cholamandalam Investment & Finance Company share price surged 36.2%

Cholamandalam Investment & Finance Company 1 Year Share Price Chart

Valuations

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | 5 Year Median EV/EBITDA | ROCE |

| 1 | Hindustan Unilever | 35.3 | 38.3 | 27.8% |

| 2 | Mahindra and Mahindra | 14.8 | 12.4 | 13.9% |

| 3 | Finolex Industries | 15.2 | 17.4 | 8.8% |

| 4 | Cholamandlam Investment and Finance Company | 15.9 | 16.0 | 10.3% |

HUL continues to trade at a high multiple. Even so, it is below its own five-year media. This reflects strong and consistent returns, though growth has slowed.

Mahindra and Mahindra is trading above its long-term median. This indicates that the recent improvement in volumes and margins is already reflected in the stock price.

Finolex Industries trades below its historical average. Returns are lower and demand moves in cycles. That has kept valuations from moving higher, even though the balance sheet is strong.

Cholamandalam Investment and Finance is trading close to its five-year average, which suggests the market is taking a balanced view on growth and asset quality.

Valuations are not cheap. Investors need to decide whether future growth can support current prices, instead of relying only on recent momentum.

Conclusion

Rural demand in India is clearly picking up. Spending is improving and the recovery is showing up across several sectors. But the benefits are not evenly spread. Some businesses are converting this trend into steady numbers. Others are still struggling with returns or consistency.

That gap is visible in valuations. Companies with stable cash flows and better profitability continue to command higher multiples. Those with weaker or more cyclical performance remain cheaper. The market is already making that distinction.

For investors, this means one simple thing. This is not a story to buy blindly. It is about choosing carefully. The better opportunities lie in businesses where rural exposure is real, balance sheets are strong, and growth has held up across cycles, not just in one good year.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.