Nirmala Sitharaman’s recently presented Budget for 2026 represents a clear shift from populism to duty (Kartavya). One of these duties is to care for the environment. The budget has a plan in place to change Carbon Capture, Utilization, and Storage (CCUS) from a niche technical concept into a central pillar of India’s industrial policy.

By committing a Rs 20,000 cr outlay over the next five years, the government is providing the financial bridge needed to scale this technology across high-emission sectors like steel, cement, and power. This move effectively future-proofs Indian heavy industry against global carbon taxes and aligns domestic growth with strict net-zero targets.

While the big names will continue to grab all the limelight as usual, there are a few underdogs which are positioned to be a very important part of this big change. But before you read about them, you must know what CCUS is.

CCUS: The Vacuum Cleaner of Heavy Industry

In the simplest of words, Carbon Capture, Utilization, and Storage (CCUS) is a suite of technologies designed to act like a giant vacuum for industrial pollution.

It catches carbon emissions directly at the source (like a steel furnace or power plant) before they are let out into the environment. This carbon is then either buried deep underground forever (“Storage”) or recycled into products like building materials, chemicals, or fuels (“Utilization”).

India is the world’s third-largest emitter and many of our critical industries, like steel and cement, rely on coal and have no easy way to go green overnight. The Rs 20,000 cr outlay over five years aims to make this expensive technology commercially viable for five key sectors: Power, Steel, Cement, Refineries, and Chemicals.

Without this technology, our steel and cement could face exorbitantly high carbon taxes when sold to markets like Europe. The CCUS technology will protect the long-term export competitiveness of Indian companies in such a case.

Here are the two contrasting stocks poised to get attention from investors for their expertise in CCUS.

#1 Ducon: The Turnaround Underdog

Incorporated in 2005, Ducon Infratechnologies Ltd is in Engineering, Procurement and Construction business.

With a small market cap of Rs 114 cr as on 3rd February 2026, the company does not see much coverage in mainstream media but is one of the few Indian firms with an active R&D program (launched in September 2025) dedicated specifically to solvent-based carbon capture technology.

This technology is critical because it can be retrofitted onto existing coal and gas power plants. Something which is a major priority in the new budget.

The company is already a leader in Flue Gas Desulphurization (FGD) systems. In industrial engineering, an FGD system is a mandatory technical pre-requisite for carbon capture; adding CCUS to their portfolio allows Ducon to offer a seamless, end-to-end decarbonization package.

Ducon serves massive hard-to-abate industries, including power utilities (up to 1000 MW single boilers), cement, steel, and oil refineries. Their recent launch of an AI-driven optimization platform, IQ Energy AI, further targets these energy-intensive sectors to improve fuel efficiency and reduce emissions.

Let us look at the financials of the company to see how it has been doing in the past few years.

The sales of the company have grown at a compound rate of 7% from Rs 342 cr in FY21 to Rs 451 cr in FY25, and for H1FY26, the sales reached Rs 227 cr.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) was Rs 13 cr in FY21 which grew to Rs 30 cr in FY25, logging a compound growth of 23%. For H1FY26, the EBITDA logged by the company is Rs 15 cr.

The company wasn’t making any profits until FY21, which changed from FY22 and in FY25 the company recorded profits of Rs 14 cr. For H1FY26, the company has logged profits of Rs 7 cr.

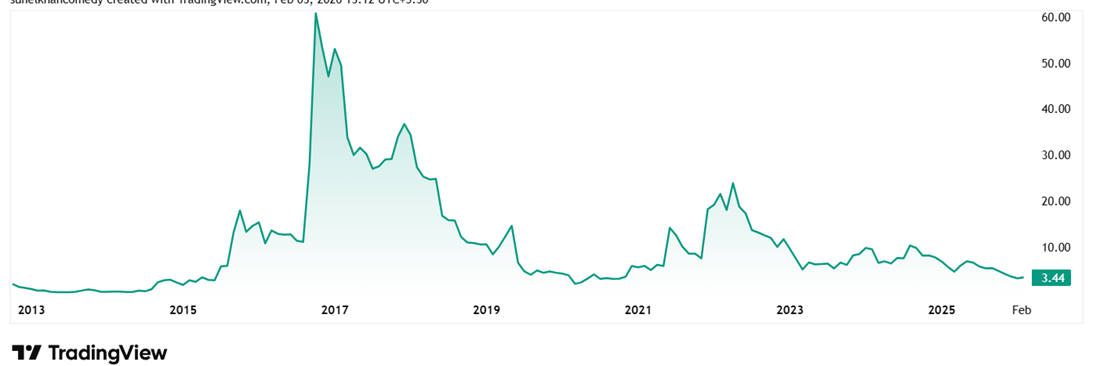

The share price of Ducon Infratechnologies Ltd was around Rs 6 in February 2021 and as on 3rd February 2026 it was Rs 3.5.

This decline was primarily driven by a severe working capital crisis, evidenced by high collection cycle of upto 225 days. This inability to convert accounting profits into actual cash has starved the company of liquidity, forcing it to rely on expensive debt of Rs 101 cr.

At the current price, the stock is trading at a discount of 95% from its all-time high of Rs 77. With the company now poised to be an important cog in the CCUS machinery the government plans too build, could this be a turnaround opportunity?

The stock is trading at a PE of 8x, while the current industry median is 10x. Which could mean the market is discounting the stock because its earnings are “on paper” only, trapped in a long collection cycle rather than being realized as cash. Investors view its low PE not as a bargain, but as a necessary risk premium to compensate for high debt and the potential threat of insolvency.

In the press release on 2nd February, a day after the budget, the company’s CMD Arun Govil said that the Government’s Budget 2026 allocation for CCUS validates Ducon’s early investments in solvent-based carbon capture R&D and signals CCUS will become an integral part of India’s industrial framework.

The press release also quotes, “Early R&D and technology differentiation (proprietary solvents and process know-how), plus engineering/EPC and lifecycle services (O&M, solvent management), should support long-term value creation as CCUS deployment scales. The Budget strengthens conviction in Ducon’s clean-technology roadmap”

#2 Thermax: The Quality Giant

Incorporated in 1966, Thermax Ltd provides integrated solutions in heating, cooling, power generation, water treatment and recycling, air pollution control and chemicals, emphasizing on ensuring clean air, clean energy and clean water.

Just like Ducon, Thermax designs the CO2 capture units for hard-to-abate sectors like refineries. Their partnership with HPCL focuses on identifying high-emission units (furnaces and hydrogen plants) where carbon can be captured and either used or prepared for storage.

With the Tax holiday for Data centres announced in the budget, their numbers are going to only go up. Data centres are energy hungry giants that require massive cooling systems. Thermax is a dominant player in absorption cooling and sophisticated energy management, making it an essential vendor for the multi-billion-dollar data centre boom the government is incentivizing.

Looking at the financials of the company, the sales have grown at a compound rate of 13% from Rs 5,731 cr in FY20 to Rs 10,389 cr in FY25, and for H1FY26, the sales have been about Rs 5,109 cr.

EBITDA grew from Rs 401 cr in FY20 to Rs 910 cr in FY25, logging a compound growth of 18% and for H1FY26, the EBITDA logged by the company is Rs 427 cr.

Net Profits jumped from Rs 212 in FY20 to Rs 627 in FY25, logging a compound growth of 25%. For H1FY26, the profits recorded by the company are Rs 324 cr.

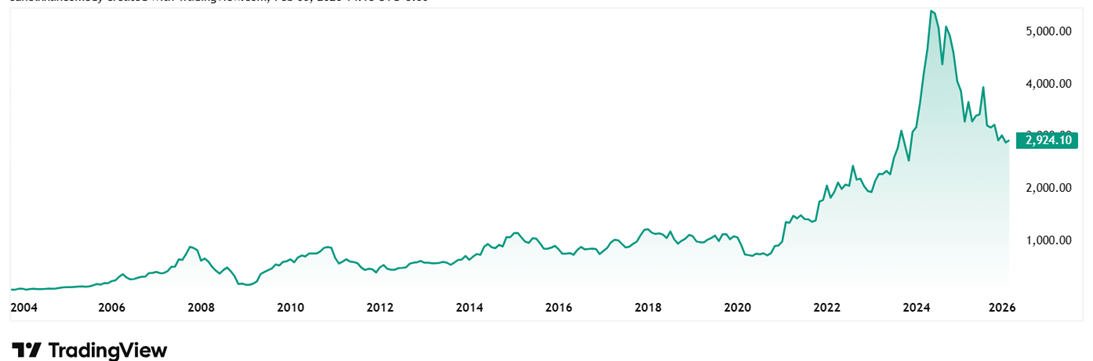

The share price of Thermax Ltd was around Rs 1,180 in February 2021 and as on 3rd February 2026 it was Rs 2,928, which is a 148% jump in 5 years.

The stock saw a considerable decline in the last 6 months possibly due to the YoY decline in profits for the quarter ending September 2025. But post the filing of the December 2025 quarter, the stock seems to be on a rebound with improved numbers.

However, at the current price, the stock is trading at a discount of 50% from its all-time high of Rs 5,840.

Looking at the valuations, the company’s share is trading at a PE of 5x, while the current industry PE is 36x.

The company had its Q3FY26 earning call on the 2nd of February 2026, in which MD and CEO, Ashish Bhandari, said that the budgets Rs 20,000 outlay for CCUS validates their partnership with HPCL and provides a clear commercial pathway for their new energy segment.

The management on the same call also highlighted that the record Rs 12.2 lakh cr infrastructure spend is a huge tailwind for their Industrial Products segment, which saw a 34% surge in orders in Q3FY26.

Investment Verdict: Quality vs. Value in the CCUS Space

The government’s Rs 20,000 cr push for carbon capture changes the game for heavy industry. The policy turns pollution control from a compliance burden into a lucrative business opportunity. Both Ducon and Thermax already have experience in the area. We could say they will both be fighting for a slice of this new pie.

But it all boils down to the level of risk one can take as an investor. While Thermax offers the safety of a clean balance sheet and steady profit growth, Ducon currently looks like a risky bet on a turnaround. These companies are from the opposite ends of the spectrum, a microcap stock and a mammoth, but have the expertise in CCUS as a common factor between them.

You see, history shows that big incentives create winners, but not every runner finishes the race. Will you pay a premium for quality or hunt for value in distress? A good idea would be to add these stocks to a watchlist and keep a watchful eye on them.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.