")

As volatility returns to the lower rungs of the market, many retail investors are fleeing at the first sign of a decline in smaller stocks. But the Warren Buffetts of India are a different breed. One of them, Ashish Kacholia, or as he is called, the “Big Whale” of the Indian markets, remains remarkably calm and still.

While the average investor panics over quarterly fluctuations, Kacholia stands by his decision and is refusing to sell two existing holdings in his portfolio that have recorded a big correction from their all-time high prices and are trading near their 52-week lows.

Both these companies have logged double digit compound growth in profit in the last 5 years but have faced a brutal correction of over 40% from their peaks. While for many investors momentum is often the only metric that matters, such corrections usually trigger a mass exodus.

What is it that Kacholia sees in these stocks that he has held them all this while? Let us dig in to find out.

Agarwal Industrial: Impressive Long-Term Growth vs. Quarterly Hiccups

Incorporated in 1995, Agarwal Industrial Corporation Ltd is primarily engaged in the business activities of manufacturing and trading of Petrochemicals (Bitumen and Bituminous Products), logistics of bitumen and liquefied Petroleum Gas and energy generation through Windmills.

With a market cap of Rs 841 cr currently, the company is a pioneer of logistics in Bitumen, which is predominantly used in road construction business. The bulk bitumen is transported via specially designed tankers, and its tankers are under contract with major oil companies in India like HPCL, BPCL and IOCL. It is amongst the leading transporters of LPG in India.

Ashish Kacholia bought a 2.6% stake in the company per the filings for the quarter ending September 2022, which grew to 4% at the end of March 2025. For the quarter ending December 2025, the holding jumped to 4.33%, amidst the falling price.

So, this could be a case of Kacholia doubling down on the opportunity to add more of what he possibly sees as a turnaround bet. But do the financials of the company hold that promise? Let us try and find out.

The sales have seen a compounded growth of 25% from Rs 787 cr in FY20 to Rs 2,399 cr in FY25. For the 3 quarters of FY26 ending in December 2025, sales of Rs 1,246 cr were recorded.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) which was Rs 46 cr in FY20 climbed to Rs 202 cr in FY25, which is a compound growth of 35%. And for the 3 quarters ending December 2025, the EBITDA logged was Rs 85 cr.

The net profits of the company grew at a compounded rate of 35% from Rs 26 cr in FY20 to Rs 116 cr in FY25. And for the 3 quarters ending in December 2025, the profits logged were Rs 28 cr.

However, while the long-term financials look to be impressive, the quarter-on-quarter figures have seen big drop. Profits dropped from Rs 85 cr figure of Q1-Q3 of FY25 to the figure of Rs 28 cr for the same quarters in FY26.

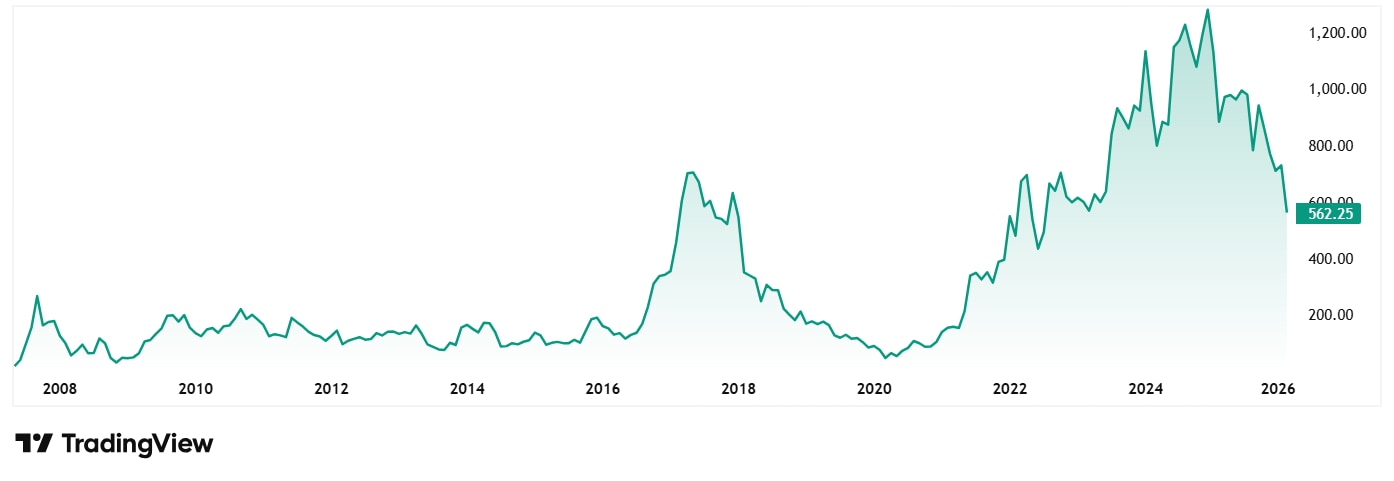

The share price of Agarwal Industrial Corporation Ltd was around Rs 155 in February 2021 and as on 26th February 2026 it was Rs 562 (a 263% jump). However, the stock has corrected by over 47% in the last 1 year and is now trading closer to its 52-week low of Rs 550.

At the current price of Rs 562, the stock is trading at a discount of 60% from its all-time high price of Rs 1,383 and 50% from its 52-week high of Rs 1,114.

As for valuations, the company’s share is trading at a current PE of around 14x, which is same as the current industry median.

The Operating Profit Margin (OPM) hit 5% at the end of December 2025, which is a drop of over 50% when compared to the previous quarter’s 11.5%. Also, screener.com highlights that the company has had declining cash flow from operations for the last 2 years, which is often a precursor to a stock price crash as growth becomes reliant on debt.

Infinium Pharmachem: High ROCE Shadows Margin Erosion

Incorporated in 2003, Infinium Pharmachem Ltd manufactures and sells Iodine based Pharmaceutical Intermediates.

With a market cap of Rs 335 cr the company is a GMP compliant, FDA Approved and ISO 9001-2015 certified company which does development, manufacture, and export of Iodine Derivatives & API, with 250+ intermediates and 15+ APIs.

Ashish Kacholia holds a 4.6% stake in the company as per the exchange filings for the quarter ending September 2025. The company files half yearly figures, as it is listed on the SME exchange.

SME Investing: Rewards vs. Risks

Before we dive into the stock further, please note that the stock is listed EMERGE – NSE’s SME Exchange. And as always, SME stocks come with a warning: buyer beware. The requirement to trade in fixed lots creates a liquidity bottleneck, often leaving investors stranded when prices crash.

Additionally, the tiny equity base of these companies invites manipulation, fuelling ‘pump and dump’ schemes designed to trap retail capital. And lenient reporting standards frequently mask poor financial health, which the investors only come to know about when it’s too late.

The company has a 5-year average ROCE (Return on Capital Employed) of 30%, while the industry median for the same period is 17%. To add to this, the company is currently debt free and hence free from hefty interest payments that eat into profits.

Let us look at the financials to see what apart from this solid capital efficiency is keeping Kacholia interested.

The sales of the company jumped from Rs 39 cr in FY20 to Rs 156 cr in FY25, recording a compound growth of 32%. For H1FY26, the sales recorded by the company were Rs 84 cr.

The EBITDA jumped from Rs 2 cr in FY20 to Rs 19 cr in FY25, which is a compound growth of 57%. And for H1FY26, the EBITDA logged is Rs 10 cr.

The net profits are where the company saw a rough road in the recent years.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Profits/Rs Cr | 1 | 3 | 7 | 10 | 12 | 8 |

Now this fall in profits could be a driver of the correction the share prices. However, for H1FY26, the company has logged profits of Rs 7 cr already, hinting at a much stronger finish for FY26.

The share price of Infinium Pharmachem Ltd was around Rs 90 when it was listed in April 2023 and as on 26th February 2026 it was Rs 215, which is a about 140% jump. However, in less than the last 12 months, the stock has corrected by almost 35%.

At the current price of Rs 215, the stock is trading at a discount of 45% from its all-time high of Rs 392.

The company’s stock is trading at a PE of 36x, and the current industry median is 28x.

Operating Profit Margins for Infinium have eroded significantly, falling from 14-15% in previous years to roughly 10–11% in FY25. As a manufacturer of iodine derivatives, the company is highly vulnerable to raw material price spikes that it has failed to pass on to customers.

One of the biggest red flags is the big drop in the promoter holding from 73% in September 2023 to 60% in September 2025. Many SME promoters treat the IPO as a destination rather than a beginning. If they start offloading stakes shortly after the mandatory lock-in period (usually 1 year for non-promoter and tiered for promoters), it suggests they are cashing out while the valuation is high, rather than staying to build the business. In the case of Infinium Pharmachem, the 13% drop in 2 years is hence a case to worry about.

The Big Whale’s Gambit: Conviction or Catch-22?

Kacholia’s refusal to exit Agarwal Industrial and Infinium Pharmachem suggests a strong conviction he has in these companies. He is probably betting on long-term industrial cycles and recovery arcs, without being bothered by the big price correction.

The numbers of both the companies tell a different story. Infinium has seen shrinking promoter stakes and thin liquidity which are not mere volatility but structural risks that come with SMEs, that can swallow capital whole. In case of Agarwal Industrial’s margin contraction and declining cash flows suggest that the “turnaround” may require more than just patience.

How these two bets of the big whale will perform and will they stage a turnaround will be a fascinating ride to watch. For now, may be add these stocks to a watchlist and keep an eye on them.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.