Higher realisation driven by a sharp increase in steel prices helped domestic steel majors — Tata Steel, JSW Steel, Jindal Steel and Power (JSPL) and Steel Authority of India (SAIL) — to post better-than-expected earnings for the three months of April-June 2018. Operating profits surged during the period for companies, on the back of prices holding strong — hot rolled coil (HRC) prices were up 14% on a year-on-year basis.

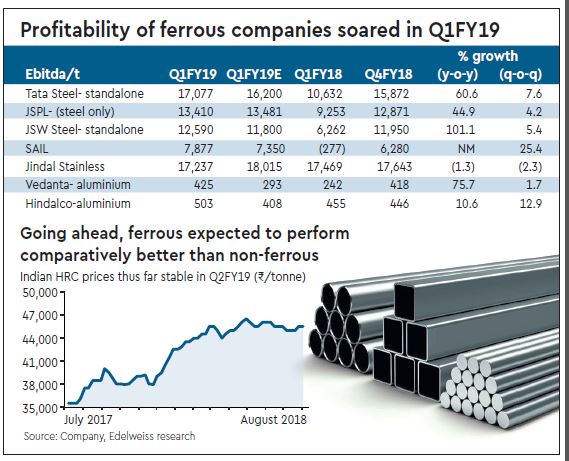

Tata Steel, on a standalone basis, for instance, reported an ebitda per tonne of over Rs 17,000, which was about 61% higher on a y-o-y basis, and about 8% up compared to the March quarter’s Rs 15,872 per tonne. The increase for JSW Steel was even more prominent, as the ebitda per tonne doubled on a y-o-y basis to nearly Rs 12,600 and came in about 5.5% higher sequentially. The company has been ramping up its value-added segment capacity and stable HRC prices are expected to augur well for the company in the coming quarters as well.

Other companies like JSPL reported a sharp 45% y-o-y surge in steel ebitda/tonne to Rs 13,410, while SAIL in a complete turnaround reported Rs 7,877 of Ebitda/tonne versus a negative Rs 277 per tonne a year ago.

Meanwhile, demand boosted by automobile, construction and infrastructure is also driving steel offtake. To be sure, the automobile sector reported an over 14% growth in FY18 compared to a year ago. The commercial vehicle segment, which constitutes a significant portion in the automotive steel demand grew nearly 20% in FY18 versus a year ago, and according to SIAM (Society of Indian Automobile Manufacturers ), the segment is expected to register a strong double-digit growth in the current financial year too. Automobile industry makes up for nearly 15% of the steel demand in India.

Even construction, which is the largest consumer of steel at around 60%, is also picking up with the government’s continuous push to infrastructure and housing. In fact, though demand for long products remained subdued in the first quarter, it is expected to go up in the coming months. Jayant Acharya, director (commercial and marketing), JSW Steel said that given the way infrastructure spends are panning out, from October onward TMT demand will pick up and the possibility of recovery of some of the prices is good.

Traditionally, during the monsoon period as construction slows down the demand and prices for TMT are under pressure.

However, Acharya said given the various projects like the metro, Bharatmala, Zuari bridge, Navi Mumbai airport, coastal road or even mega-stores like IKEA which are coming up, give confidence that the demand is strong for long products.

“There are 25 stores which are likely to come up, and each store consumes let’s say 12,000 to 15,000 tonnes per store. So you will automatically generate 200-250 tonnes of demand, just from the IKEA mega stores,” he told analysts over a conference call.

In fact, companies are finding domestic markets more lucrative to sell in the current price environment, as TV Narendran, managing director, Tata Steel, said the company actually reduced exports because the domestic markets were strong.

“Typically, the prices in the domestic markets are about Rs 2,000 to Rs 3,000 higher than the export markets. So, we can sell more in the domestic. We would prefer to sell more in the domestic,” he told analysts recently.

Narendran also said recently that the company is seeing a pull in demand in India from the automotive sector, which in some sense is a bellwether indicator for the economic activity, particularly the commercial vehicles segment.

According to analysts, Q1FY19 was a breakaway from the past, with the ferrous companies outperforming non-ferrous segment, and reported profit at net level. The ferrous clutch reported Ebitda/tonne in excess of 45%, while Ebitda growth of non-ferrous companies was relatively subdued at 15-30% y-o-y, analysts at Edelweiss Securities wrote in a recent research report.

Going ahead, too, ferrous companies are expected to continue the relative out performance driven by stable prices — average HRC price has declined a mere Rs 700-1,000 per tonne and operating leverage benefits are expected to sustain for companies like Jindal Steel and Power and Steel Authority of India.