For about half a century, if you walked into a workshop in Detroit or Stuttgart and picked up a heavy-duty crankshaft, chances are it was made by Bharat Forge. This Pune-based giant with a leadership position in the metal-bashers space, saw its fortunes rise and fall with the cyclical demand for American Class-8 trucks.

With a market cap of Rs 70,315 cr, Bharat Forge (part of the US$ 3 bn Kalyani Group) is engaged in the manufacturing and selling of forged and machined components for auto and industrial sectors.

But on December 31, 2025, something big happened and one of Bharat Forge’s long-held dreams came true.

With the announcement of a massive Rs 1,662 cr contract from the Ministry of Defence (MoD), Bharat Forge has signalled the completion of a decade-long metamorphosis. It is no longer just an auto-ancillary stock. It is a full-fledged defence prime.

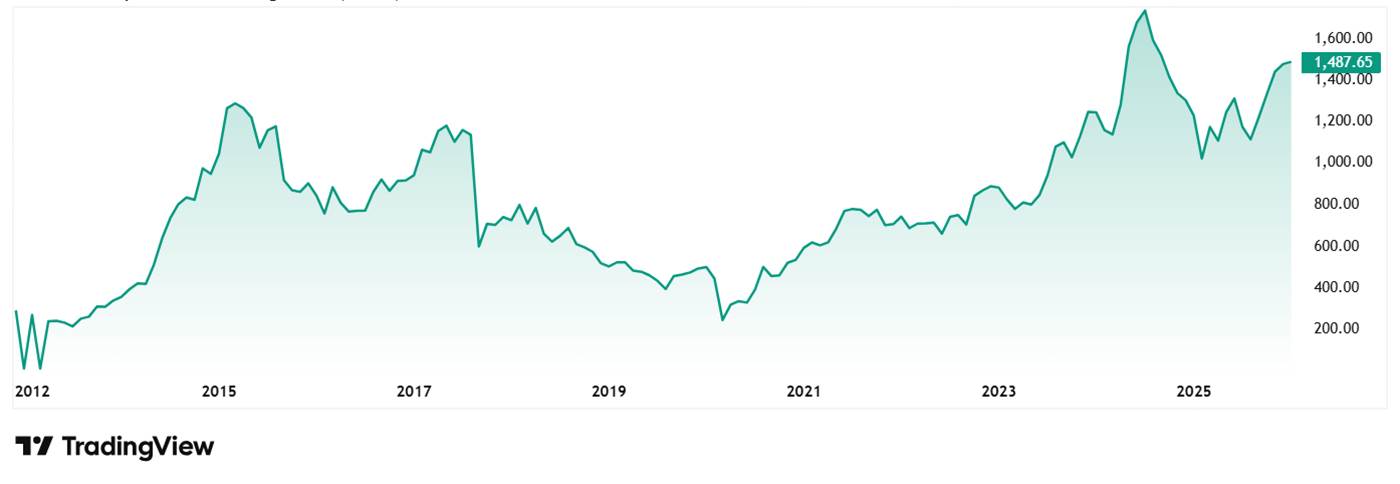

For investors watching the stock priced at Rs 1,471 (as on 6th January 2026) inch closer to its all-time high of Rs 1,826, the question is no longer “Is it cheap?” but “How big can this get?”

Bharat Forge Stock Price Chart

The “small arms” jackpot: Why this deal matters

To understand why this order has caused ripples, you have to look past the rupee figure. Rs 1,662 cr is big, but for a company with over Rs 15,000 cr in revenue, it is not a significant outlier.

The real story is not the number, but the nature of the order.

You see, for decades, the Indian Army’s small arms like rifles, carbines, light machine guns, were the exclusive domain of state-run ordnance factories or foreign vendors like Sig Sauer. So, quality was hit-or-miss; timelines were theoretical.

By awarding this contract to Bharat Forge, the Ministry of Defence has effectively handed the keys of infantry modernization to the private sector.

The economics of mass production: 2.5 Lakh Units

The deal, signed on the last day of 2025 involves the supply of 255,128 Close Quarter Battle (CQB) Carbines to the Indian Army.

Over2.55 Lakh units. This is not a boutique order for a few hundred sniper rifles. This is mass production on a scale that rivals automotive assembly lines.

What makes it even more interesting is the timelines. The order has to be executed in the next 5 Years. This gives a verified revenue visibility through 2030.

It creates a base load for their defence factories that artillery guns (which are lumpy, one-off orders) cannot provide.

And like we said, this isn’t just a usual order. The order is for Indigenously Designed, Developed and Manufactured (IDDM) weapons.

Bharat Forge didn’t just buy the blueprints; they co-developed the tech with DRDO. That means the Intellectual Property (IP) stays in Pune. There are no royalty cheques being mailed to a foreign partner, which means the margins stick to the bottom line.

Kalyani strategic systems: The growth engine

Investors often look at Bharat Forge’s standalone numbers and wonder, “Why is the revenue growth flat?”.

The reason is that the magic is happening in the subsidiary – Kalyani Strategic Systems Ltd (KSSL). KSSL is the entity housing the defence ambitions.

In just three years, this subsidiary has evolved from a prototype shop to an export powerhouse.

In November 2022, KSSL bagged a $155 Mn export order for 155mm artillery guns. The order is currently active and deliveries are taking place

And now with this new Carbine win, the executable defence order book has jumped from roughly Rs 9,400 cr in September 2025 to over Rs 11,000 cr today (per a quote by Amit Kalyani (MD) to NDTV Profit).

To put that in context: The defence order book is now nearly 70% of Bharat Forge’s entire FY25 standalone revenue. The long-held dream is fast becoming the main event.

Valuation forensics: The ‘auto-drag’ vs. The ‘defense-lift’

Let us dive a bit deeper to understand what is in store here.

If one buys into Bharat Forge today at its current price of Rs 1,471, they are essentially buying two different companies wrapped in one ticker symbol.

1. The “Auto” Anchor (The Drag) The traditional business, making parts for US and European trucks, is currently in a brutal winter. Q2 FY26 numbers showed a 7.5% revenue decline in this segment. The management explicitly cited “destocking” in North America. If Bharat Forge were solely an auto parts maker, the stock price could have been a different ball game in today’s market.

2. The “Defence” Engine (The Lift) The market is willing to look past the US truck recession because the defence vertical is growing at triple digits.

- FY23 Defence Revenue: Rs 410 cr

- FY25 Defence Revenue: Rs 1,772 cr

- FY26 Est. Defence Revenue: Expected to cross Rs 2,500 Cr

3. The Valuation Premium The stock trades at a consolidated P/E of roughly 65x. This is expensive, no questions asked. For comparison, the current industry median is 30x.

The market is possibly in the phase of re-rating the company from a low PE Auto Ancillary to a high PE Defence Capital Goods company.

If the defence contribution to profit crosses 25-30%, this premium is justified. If execution falters, the valuation could contract painfully.

The turnaround possibility

Bharat Forge has spent the last five years pouring concrete. They built massive new facilities for defence and aerospace in Khed and Baramati. These factories are currently “Works in Progress” or running at low utilization. They are eating capital but not yet spitting out profits.

In accounting terms, the “Capital Employed” has bloated, but the “Return” hasn’t kicked in yet.

So, as the Rs 11,000 cr order book gets executed, these factories will ramp up. Operating leverage will in all possibility kick in. If everything plays out to perfection, a big “if”, then perhaps there’s something worth tracking closely here.

The bear case: Execution risks and raw materials

While everything looks very bright and colourful up until now, an investor must never lose objectivity. Remember, trees don’t grow in air. Here are the risks/red flags that one must know about.

- Execution Risk: Manufacturing 2.5 lakh guns is a logistical nightmare. Any quality control issue (a jammed rifle in a field test) can lead to contract pauses. The Indian Ministry of Defence is the strictest customer you could ever find.

- Global Recession: While defence is insulated, 60% of revenue still comes from Auto/Industrial sectors. If the US hard landing happens in 2026, the core business could bleed enough to offset the defence gains.

- Raw Material Volatility: Steel prices are inching up. As a forging company, Bharat Forge passes these costs on, but usually with a lag, which can hit margins in the short term.

The Verdict: A structural pivot

In simpler words, Bharat Forge is currently a tale of two cities. One city (Auto) is struggling with a cyclic winter. The other city (Defence) is booming. The company’s transformation from a chassis-maker to a gun-maker is a rare value migration story in the Indian market.

The Rs 1,662 cr order is the bridge that carries the company safely across the auto sector chaos. It provides verified, government-backed cash flow for the next 5 years.

The stock is not cheap. But most category leaders undergoing a structural pivot rarely are. It is highly recommended that the stock be added to a watchlist and the quarterly execution numbers are looked at closely.

If the company delivers the first batch of carbines on time, it will be a fascinating ride to watch from there on.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.