By Mitali Salian & Vinayak Aggarwal

Stung by the collapse of IL&FS and Jet Airways, a clutch of state-owned banks has put aside a staggering Rs 50,000 crore in the March quarter for existing and potential loan losses. How much of this would be written off and how much can be put to use again is hard to say. But the sheer size of the provisions suggests the NPA (non-performing assets) cycle hasn’t quite turned.

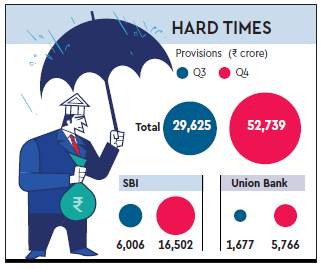

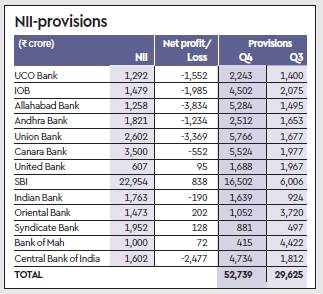

Loan loss provisions across 13 public-sector banks stood at Rs 52,739.39 crore for Q4FY19, sharply higher than the `29,625.25 crore in Q3FY19. Most of these lenders reported losses for the March quarter with total losses of eight banks at `15,192 crore.

At the post-earnings press conference last week, State Bank of India chairman Rajnish Kumar clarified the bank has classified `1,125 crore of the total IL&FS exposure of `3,487 crore, as an npa. “Now whatever happens, the remaining legacy credit cost will be done by March 2020. From 1 April, 2020, there will be no legacy cost as far as corporate book is concerned,” Kumar said.

The bank also classified a `1,200-crore exposure to Jet Airways as an NPA, against which “more than required provisions” have been made. SBI’s loan loss provisions for Q4FY19 stood at `16,501.89 crore, a four-fold jump over the `6,006.22 in Q3FY19.

In the case of eight of 13 PSBs, loan loss provisions far exceeded the net interest income (NII) in the March quarter. Analysts suggest these lenders could take at least two more quarters and additional provisioning before their books are clean.

The cumulative net income interest for the 13 lenders stood at `43,304.13 crore against the `52,739.39-crore loan loss provisions.

In a post-earnings press release, Indian Overseas Bank attributed its loss in the quarter to increased provisions on non-performing assets and fraud accounts “especially due to back dating of NPAs and one big account declared as fraud”.

The bank further said the impact of these two events on provisions was around `2,150 crore. Analysts say the net NPA ratio at 10.8% of total assets will require approximately `6,000 crore in provisions to help bring the ratio to below 6% and to help it emerge from the Prompt Corrective Action framework.

The additional provisioning, they pointed out, is around 1.2 times the lender’s operating profit for FY19. “We believe the bank would be making provisions aggressively in the next few quarters. This would result in negative earnings for at least the next couple of quarters,” analysts at Anand Rathi said.

Analysts at Axis Capital noted that Canara Bank, which posted a loss of `551.53 crore in Q4FY19, too, was hit by higher provisions. They expect these will remain elevated on high SMA II and power sector exposure.

In the case of Union Bank of India, the Q4FY19 loss of `3,369 crore came on the back of `5,766-crore provision burden. The bank said it needed to make additional ageing provisions of over `3,000 crore for some NPAs where the Reserve Bank of India had identified divergences in asset classification.

Analysts at Emkay noted Indian Bank’s higher loan loss provisions were the result of the ageing effect. Also, residual provision divergence for FY18 led to a large loss of `1,900 crore in Q4FY19.