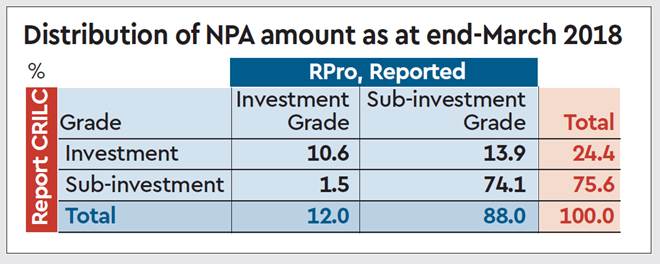

Around 24% of the sampled bad loan exposure from the credit monitoring repository had an investment grade rating just a quarter before they turned non-performing assets, data from the Reserve Bank of India (RBI) showed. The study raises questions about the quality of banks’ reporting to the RBI-constituted Central Repository of Information on Large Credits (CRILC).

In the report, titled ‘Efficacy of Credit Ratings in Assessing Asset Quality: An Analysis of Large Borrowers’, the central bank said there was a divergence between the ratings of credit rating agencies (CRAs) as reported in Prowess and those reported by banks in CRILC. One of the possible reasons for the divergence, as per the report, could be that banks reported the ratings corresponding to only those facilities of a borrower to which they were exposed. However, most of the exposures showing divergence had reached the C or D rating categories as per Prowess, which is an alternative external source of data on corporate credit ratings.

The trend could suggest either delayed action by CRAs or delayed reporting on the part of the lenders, the RBI said. “As the share was derived from CRILC alone, it can be argued that the deficiencies could be due to either the ways in which ratings are assigned by CRAs or the ways in which ratings are reported by banks or both,” the RBI report said, adding, “By mapping CRILC with Prowess, it was observed that about 14% of the sampled NPA exposure showed a sub-investment grade in Prowess, but carried an investment grade in CRILC, indicating concerns about delayed/lagged reporting of ratings by banks in CRILC.”

The central bank also believes that since ratings given by the same CRA for different facilities of a borrower are generally expected to move in tandem, as they are essentially based on the borrower’s repayment capacity, the divergence in ratings could be on account of reporting issues on the part of banks. Another possibility explaining the divergence could be delayed reporting to CRILC by banks. An analysis of the data from both sources showed that ratings reported by banks did not adequately reflect recent rating changes.