Finance minister P Chidambaram on Wednesday held out an olive branch to the Opposition on key reform Bills listed for passage in the current session of Parliament, discussing the issue with two senior BJP leaders, Sushma Swaraj and Arun Jaitley. Chidambaram later claimed to have reached an understanding with the two leaders on the ?urgent need? to get these Bills approved by the House and indicated a consensus was in sight on the banking regulation Bill.

With only six days left to go in the winter session, Chidambaram’s initiative is seen as a last-ditch effort to push through financial sector Bills, particularly those relating to the banking, insurance and pension sectors. Swaraj and Jaitley are the leaders of the opposition in the Lok Sabha and Rajya Sabha, respectively.

With only six days left to go in the winter session, Chidambaram’s initiative is seen as a last-ditch effort to push through financial sector Bills, particularly those relating to the banking, insurance and pension sectors. Swaraj and Jaitley are the leaders of the opposition in the Lok Sabha and Rajya Sabha, respectively.

?I have discussed all five economic reforms Bills with two leaders of opposition (Swaraj and Jaitley). They understand the urgency,? Chidambaram said, adding: ?I told them (the Opposition), let me pass the banking Bill and I will come back to you over the weekend and discuss the insurance Bill.?

Chidambaram’s move comes close on the heels of rating agency Standard and Poor’s saying on Tuesday that India’s large fiscal deficit and the heavy debt burden were the ?most significant rating constraints?. Both S&P and Moody’s accord ratings just above junk status to India right now and a rating downgrade is seen to be imminent if budget deficits are not tamed.

Despite the limited time left in the current session, Chidambaram expressed the hope that all the five financial sector Bills ? on banking, insurance, pension, debt recovery and anti-money laundering ? would be passed in the session. He, however, reiterated that the banking Bill would not need to be referred to the standing committee on finance again as demanded by the Opposition. The contentious proposal to allow banks to trade in commodity futures was inserted by another House panel ? that on food and consumer affairs, he noted.

The minister promised to discuss the insurance Bill with the Opposition again on Saturday to iron out differences. The Bill seeks to raise the foreign investment cap from 26% to 49%. FE had earlier reported that a consensus formula being worked out in this regard could be to retain the foreign direct investment limit at 26% and allow foreign institutional investors to take up 23% on top of it.

The Banking Laws (Amendment) Bill among other things seeks to give the Reserve Bank of India the power to supersede bank boards, a precondition set by the central bank for issuing new bank licences. The passing of the Bill would also encourage domestic and foreign private investors because the voting rights of shareholders of private banks is proposed to be hiked to 26% from 10% and that in the case of nationalised banks from 1% to 10%. The proposed larger say in management is expected to spur private investment ? domestic and foreign ? in the Indian banking industry.

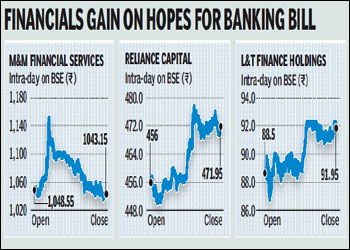

Renewed hopes that the banking Bill could be passed in the current session saw a surge in the stocks of non-banking financial companies that are tipped to be among the new bank licensees ? L&T Finance Holdings, Mahindra & Mahindra Financial Services and Reliance Capital ? on Wednesday.

Amid the gloom, the industrial production data for October denoting an 8.2% annual growth, contrasting with negative growth reported in five out of the first seven months of the fiscal ? brought some cheer. While Chidambaram said the data indicated ?green shoots in the economy?, many analysts saw it as a sign that the economy has finally turned the corner. The surge in the index of industrial production (IIP) was, however, enabled by the Diwali spending spree and a low base ? the index had contracted by 5% in October 2011 and, hence, many discounted it as an ?optical illusion? and drew attention to the high volatility of the IIP data.

The finance minister also said the growth in direct tax receipts in April-November was satisfactory. While the gross direct tax collection grew a modest 7.14% during the period to Rs 3,25,696 crore, net receipts showed a 15.04% jump to Rs.2,70,731 crore, suggesting lesser refunds during the period from a year ago.