The Finance Minister’s has made no structural changes in the interim budget in line with the parliamentary practice. Here are some crucial aspects:

No Changes in Personal Tax Rates

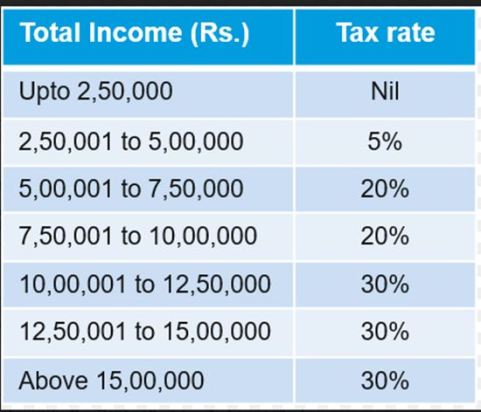

In line with the past parliamentary practice, the interim budget does not propose any major structural change in the tax rates and continues the same as per last year. Under the new regime, a person having gross income up to Rs 7 lakh shall have NIL tax liability.

Old Tax Regime

New Tax Regime

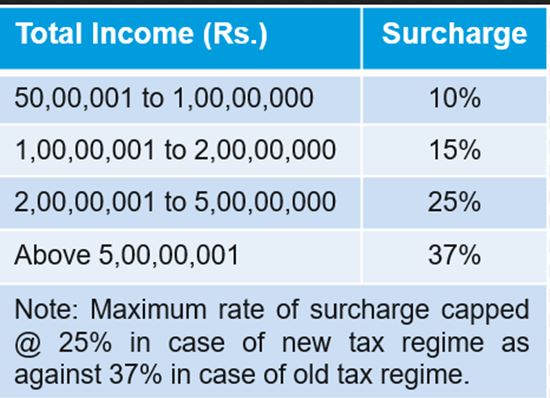

Surcharge Rate

* Health & education cess @ 4% is levied on aggregate of tax amount and surcharge amount.

* Rebate of Rs. 12,500 available in case of old tax regime for total income up to Rs. 5,00,000 and of Rs. 25,000 in case of new tax regime up to total income of Rs. 7,00,000. Marginal tax relief available in case of new tax regime for income exceeding Rs. 7,00,000.

* Surcharge on Capital Gains and dividend taxation unchanged at 15%.

Also Read: Budget 2024: No change in personal taxation disappoints taxpayers, salaried class

Waiver of the old Trivial Tax Demands

In the Interim Budget 2024, the Proposal of waiver of old unreconciled trivial tax outstanding is in line with the Government’s vision to improve ease of living and ease of doing business. There are a large number of petty, non-verified, non-reconciled or disputed direct tax demands, many of them dating as far back as the year 1962, which continue to remain on the books, causing undue hardship, administrative difficulties and hindering refunds of subsequent years.

The proposal is to withdraw such outstanding direct tax demands up to Rs. 25,000 pertaining to the period up to financial year 2009-10 and up to Rs. 10,000 for financial years 2010-11 to 2014-15. No specific mention has been made about whether this tax proposal would be applicable for individual or corporate taxpayers. it is expected to overall benefit about 1 crore taxpayers and is extremely welcome. There are no specific proposals in the Finance Bill 2024 in this respect and it is likely that a separate circular will be issued by the CBDT to provide the aforesaid relief.

No changes in Basic Exemption Limit

As per the current tax laws, the Basic Exemption Limit (‘BEL’) under old tax regime is Rs 2,50,000 which has remained the same since its last revision in Budget 2014. Even under the new tax regime, the basic exemption limit is Rs 3,00,000. Considering that the cost of living has increased multi-fold times in the past decade, it was expected that the said basic exemption limit be increased to Rs 3,50,000 under both the regimes. Enhancing the said basic exemption limit may benefit a large number of taxpayers and tax filers out of the approximately 7 crore taxpayers.

Extension in the due date for filing Belated tax return to the end of the assessment year

The existing due date for filing a belated return is 31st December of the relevant assessment year. For instance, the belated return for Financial Year 2023-24 can be filed by 31st December 2023. Such filing of a belated return would attract late fees of Rs. 5,000 (restricted to Rs. 1,000 wherein the total income of the taxpayer does not exceed Rs 5 lakh). There are a large number of tax filers who miss the deadline of the belated return due to personal exigencies, delay in getting or collating data. It was expected that belated returns should be permitted up to 31 March but can require a higher fee of Rs 10,000. This would have ensured that the while the tax filer is penalized, he does not become a delinquent tax filer.

We can still hope that the increase in basic exemption limit and the belated return related relaxations will be introduced in the Final Budget.

(By Dr Suresh Surana, Founder, RSM India. Views are personal)