")

Promoters have been heavy sellers in the Indian market in recent years. According to a media report, promoter selling crossed a record Rs 1.5 lakh crore in 2025, compared with the previous peak of Rs 1.43 lakh crore in 2024. The selling was led by block, bulk and OFS deals. Private promoter shareholding also fell to an eight-year low of 40.58% as of June 2025.

This does not always mean promoters are losing faith in their companies. They may sell shares to repay debt, meet public shareholding norms, fund new ventures, manage succession, or monetise wealth. Still, large promoter selling often worries investors because promoters usually understand their businesses better than outside shareholders.

But the latest shareholding data shows a shift in some companies. Promoters have increased their stake through direct market purchases. This is different from technical increases caused by mergers, warrant conversions, preferential allotments, or reclassification. A direct purchase shows that the promoter is willing to invest more money at the current market price.

For this article, we looked at companies where promoter holding rose materially. We filtered out corporate actions and special situations. The final list includes only three companies where the increase appears to be backed by direct promoter or promoter-group purchases. We also kept the market-cap threshold above Rs 2,000 crore to avoid very small and illiquid names.

#1 Godrej Properties : Scaling Operations Amid Share Consolidation

Godrej Properties (GPL) is the real estate development arm of the Godrej Group, which was started in 1897 and is today one of India’s most successful conglomerates.

Godrej Properties’ promoter buying has come at a time when the company is reporting stronger operating and financial numbers. The promoter group increased their stake by 5% in FY26. A large chunk o the purchase was made in the March quarter. Management linked this to its broader confidence in the company’s long-term value.

Promoter Holding in Godrej Properties in the Past Eight Quarters

| Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| 58.47% | 58.47% | 46.50% | 46.67% | 46.70% | 47.05% | 47.17% | 51.66% |

The purchase was backed by a year of record performance. Godrej Properties said FY26 was its best year for business development, bookings, collections, operating cash flow and earnings. In Q4 FY26, total income rose 47% year-on-year (YoY) to Rs 3,895 crore. Net profit rose 70% YoY to Rs 650 crore. For the full year, total income increased 22% to Rs 8,374 crore, while net profit grew 32% to Rs 1,850 crore.

Execution and FY27 Booking Targets

The company’s sales momentum remained strong across markets. Q4 bookings stood at Rs 10,163 crore, up 21% quarter-on-quarter. For FY26, booking value rose 16% YoY to Rs 34,171 crore, which was 105% of its guidance. The company sold 17,513 units during the year, covering 27 million sq ft.

Business development was another key driver. Godrej Properties added projects with future sales potential of Rs 42,100 crore in FY26. This was more than 200% of its guidance and 59% higher YoY. The company closed 18 deals with an aggregate area of about 33 million sq ft. In Q4 alone, it added six projects with expected booking value of nearly Rs 17,500 crore.

The company has also laid out a busy launch calendar for FY27. In NCR, it expects launches in Gurgaon and is hopeful of launching the long-delayed Ashok Vihar project in Delhi. Management also expects launches or phase activations in Greater Noida, Mumbai, Bandra, Worli, Vikhroli, Thane, Hyderabad, Bengaluru, Pune, Kolkata, Raipur and Ahmedabad. However, it cautioned that some launches can slip because of approvals and project-level timelines.

The FY27 guidance reflects this pipeline. The company expects residential bookings to cross Rs 39,000 crore, about 20% higher than its FY26 guidance. It also expects collections to grow to more than Rs 24,000 crore. Management said its available inventory for sale is 35% higher year-on-year.

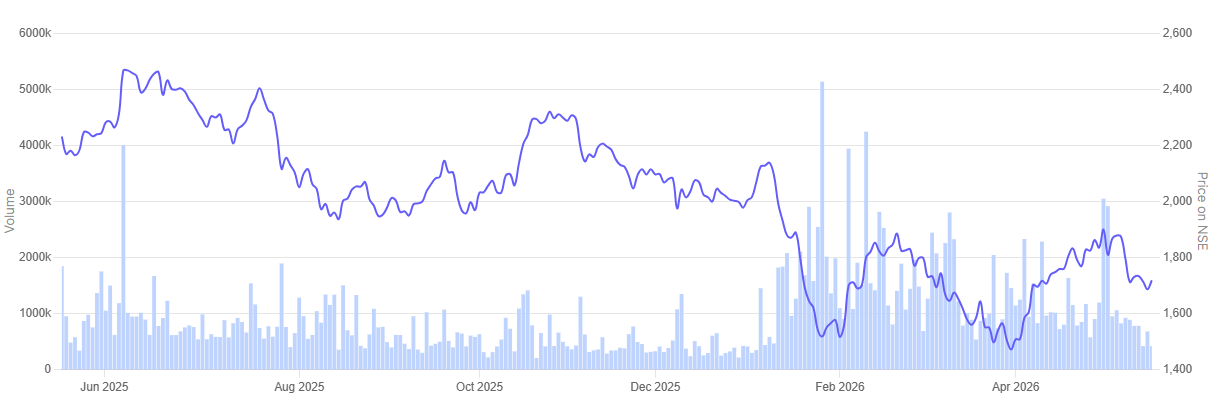

In the past year, the share price of Godrej Properties has tumbled 23.2%.

Godrej Properties 1 Year Share Price Chart

#2 Adani Energy Solutions : Executing an Infrastructure Capitalization Super-Cycle

Adani Energy Solutions, part of the Adani group, is a multidimensional organization with presence in various facets of the energy domain, namely power transmission, distribution, smart metering, and cooling solutions. It is India’s largest private transmission company.

Adani Energy Solutions’ recent promoter buying comes against a year of higher capex, project commissioning and stronger earnings. The company reported a major step-up in its energy infrastructure pipeline in FY26. Management said the business is scaling across transmission, distribution, smart meters and commercial and industrial supply. During Q4 FY2026 promoters holding increased 1.53%; over the ywar, the increase was just under 3%

Promoter Holding in Adani Energy Solutions in the Past Eight Quarters

| Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| 74.95% | 69.94% | 69.94% | 69.94% | 71.19% | 71.19% | 71.19% | 72.72% |

Operational Execution and Capex Targets

The company’s financial performance also improved during the year. In FY26, Adani Energy Solutions reported consolidated sales of Rs 27,588 crore up 16.1% YoY. Its net profit at the end of the year stood at Rs 2,393 crore up 159.5% YoY. Adani Energy’s profit jumped significantly because more of its large projects came out of the commissioning phase have started contributing to the business. The company is now beginning to earn from the heavy investments it made earlier.

A key milestone in the March quarter was the commissioning of the Mumbai HVDC project. The project was fully commissioned on March 15, 2026. Management said the project cost was around Rs 7,000 crore and the full-year tariff from the project is expected to be around Rs 1,300 crore from FY27. The project is also important for Mumbai’s transmission capacity and renewable power integration.

Transmission remains the company’s main growth engine. Adani Energy said its market share in transmission bidding improved to nearly 29-30%. It also said projects worth about Rs 1.5 lakh crore have already been identified for bidding. Of this, about Rs 80,000 crore to Rs 1 lakh crore may be finalised over the next 12 months.

The capex plan is also large. For FY27, the company expects capex of about Rs 21,000-22,000 crore. This includes nearly Rs 15,500 crore in transmission, Rs 2,350 crore in distribution and Rs 3,900 crore in smart metering. FY28 capex is expected to remain in the Rs 22,000-25,000 crore range.

Smart metering was another major area of execution. The company installed 82.29 lakh smart meters in FY26, against an earlier target of around 70 lakh meters. Management said aggregate smart meter deployment had crossed 1 crore meters. For FY27, it expects to install at least another 1 crore meters.

The distribution business remained steady. In Mumbai distribution losses have reduced from 8.5% at the time of takeover to 4.2%. Management said it continues to add Rs 1,500-2,000 crore of capex every year in the distribution business. The focus is on improving service quality while keeping tariffs broadly stable.

On funding, management said the company has improved its credit profile even while raising capex. It also completed refinancing of a $500 million bond through Apollo, a US insurance investor. The company said it will continue to maintain net leverage in the range of 4.5x to 4.7x.

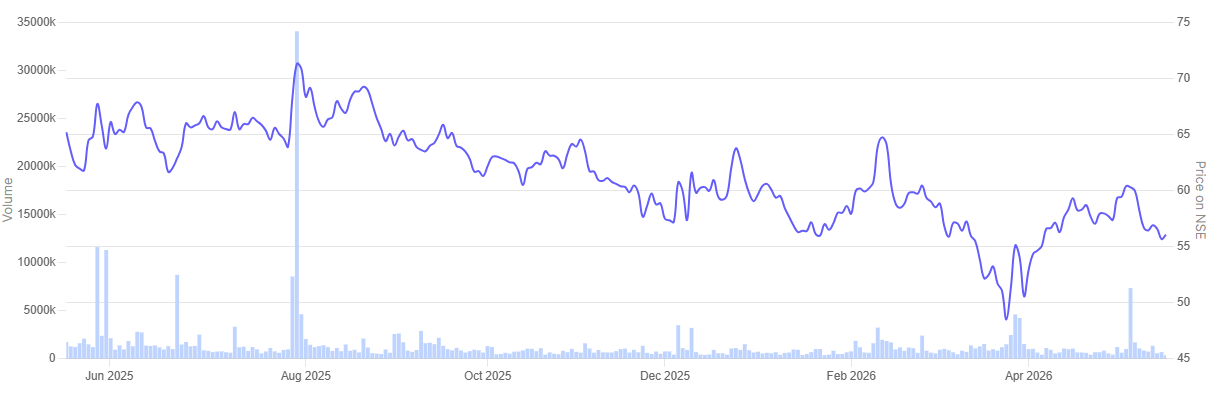

In the past year, the share price of Adani Energy Solutions has rallied 49.1%.

Adani Energy Solutions 1 Year Share Price Chart

#3 Gateway Distriparks: Counter-Cyclical Accumulation in Logistics

Gateway Distriparks is an integrated inter-modal logistics service provider. The company offers general & bonded warehousing, rail & road transportation, container handling services and other value added services.

Gateway Distriparks’ promoter buying came during a soft patch for the logistics sector. Perfect Communications, a promoter-group entity, bought shares through open-market purchases in March 2026. The move came even as the company faced weak EXIM volumes and West Asia-linked disruptions. During March 2026 increased 0.9% holding in the company.

Promoter Holding in Gateaway Distriparks in the Past Eight Quarters

| Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| 32.32% | 32.32% | 32.32% | 32.32% | 32.32% | 32.32% | 33.03% | 33.93% |

Balance Sheet De-leveraging and Volume Outlook

The company’s Q4 FY26 performance was steady, but pressure was visible. Gateway Distriparks reported consolidated total income of Rs 538.71 crore, EBITDA of Rs 122.8 crore and PAT of Rs 63.7 crore for the quarter. Throughput stood at 1,88,179 TEUs.

The operating environment remained weak in the March quarter. Management said volumes were subdued and the trend continued into April. Cargo from the US, Europe and the Middle East was impacted on the import side. On the export side, food and beverage, rice and frozen foods were affected.

Despite the near-term pressure, the company is continuing with expansion. The Indore ICD is progressing and is expected to start operations by 2028. The Jaipur ICD remains under litigation, with the next hearing listed in July for final arguments. Management said it is hopeful of a positive order either in that hearing or shortly after.

Gateway is also working on its Ankleshwar multimodal logistics park. Domestic volumes have started there and are being added month-on-month. The company has won a tender from ArcelorMittal for steel coil rake handling. The ICD portion is under construction and may take three to six months, depending on permissions.

The company is also preparing for the Dedicated Freight Corridor opportunity. Management said the last stretch to JNPT was still not complete and may take another month. Double-stacking stood at 40% for FY26 and 42% in Q4, which is important for rail cost efficiency.

Capex will remain active. Gateway plans to spend on Indore, Jaipur, three new trains, electric reach stackers, electric vehicles, solar infrastructure and warehouses at existing ICDs. The company said it has enough land bank at existing locations to handle up to four times its current volume.

The rail business remains central to the growth plan. Management said it would target about 15% growth in rail over the medium term, helped by new terminals, domestic volumes and expansion at Ankleshwar, Indore and Jaipur. CFS growth is expected to be more modest, at around 5%.

Debt is also coming down. Management said Gateway’s standalone gross debt has reduced from about Rs 550 crore earlier to around Rs 170 crore. Even so, cash flows will be used for trains, EVs, equipment, warehouses, solar infrastructure and future ICD capex.

In the past year, the share price of Gateaway Distriparks is down 13.9%.

Gateaway Distriparks 1 Year Share Price Chart

Conclusion

Promoter buying is a good signal, but it is not a guarantee. Investors should not buy a stock only because promoters have bought shares. It only means the stock is worth a closer look.

These three companies are also very different. One is a real estate company. One is a power infrastructure company. One is a logistics company. So, their numbers and valuations cannot be compared directly.

The better way is to track what happens next. If promoter buying is followed by better execution, stronger cash flows and steady profit growth, the signal becomes more meaningful. Until then, these stocks can be kept on the watch list.

You can track how these are progressing by adding stocks to your watchlist.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.