")

India’s electronic manufacturing services (EMS) story remains structurally intact. The long-term tailwinds, including import substitution, China+1 diversification, and rising domestic electronics demand, have not weakened. What has changed is the pace. After several years of near-linear growth, the sector is now seeing a phase of moderation.

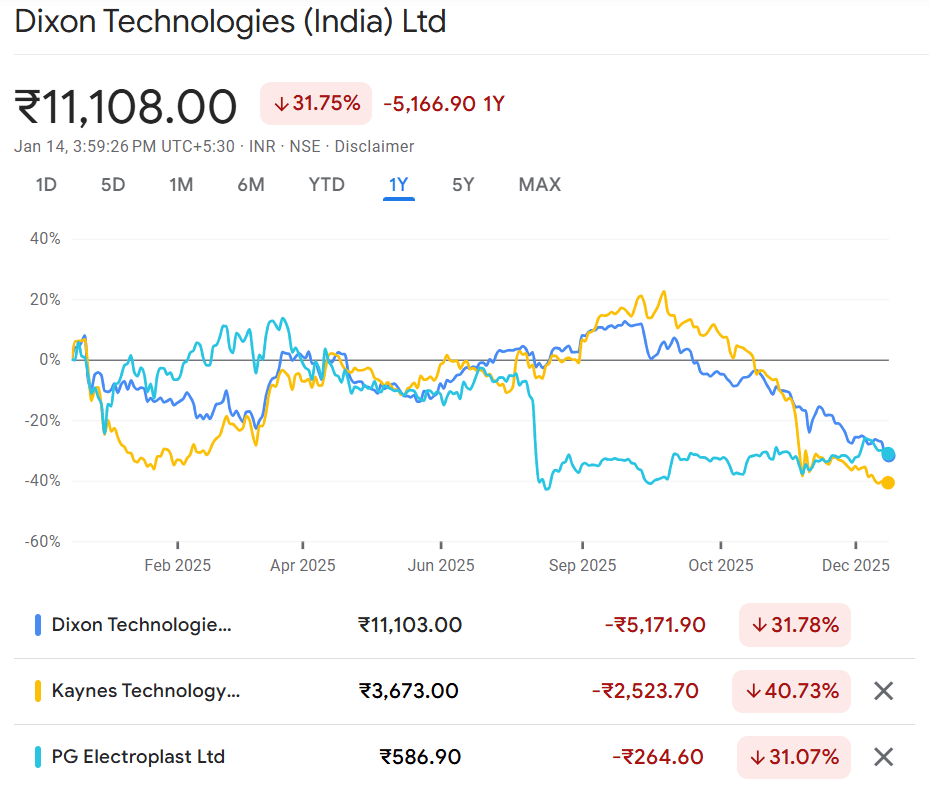

High base effects, temporary demand softness in select categories, working capital pressures, and valuation fatigue are beginning to be reflected in stock prices. The share prices of three leading EMS companies have fallen by more than 30% from their highs. But what now? Are they worth looking at the current valuation?

Share Price Movement

Let’s take a look.

#1 Dixon Technologies:

Dixon Technologies is a leading Indian electronic manufacturing services company. The company operates across multiple segments in mobile phones, consumer electronics, home appliances, lighting, and telecom equipment. Dixon has seen considerable growth, but a slowdown in that growth, along with a high valuation, has pushed the stock lower.

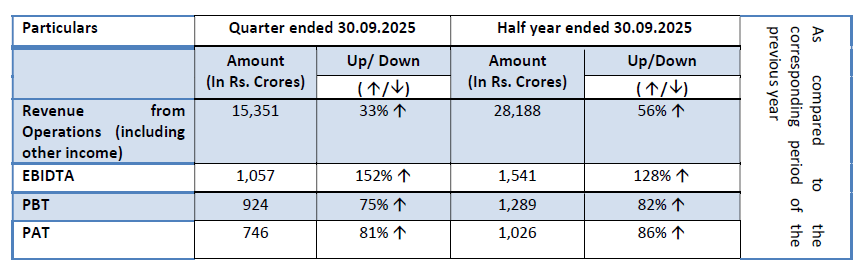

Dixon reported strong financial results for the half-year of FY26. Revenue grew by 56% year-on-year to ₹28,188 crore, driven by volume growth. EBITDA (Earnings before Interest, Tax, Depreciation, and Amortization) surged by 128% to ₹1,541 crore, with margins at 5.5%.

Net profit also jumped by 86% to ₹1,026 crore. However, high memory prices, delays in joint venture approvals, and concerns over the expiry of mobile production-linked incentives have impacted the company’s short-term performance. HSBC said Dixon could report a subdued third quarter, which led to a sharp fall in Dixon’s share price.

A slowdown in particular business segments impacted its performance in Q2. The Consumer Electronics segment (LED TVs and Refrigerators) saw a 32% year-on-year revenue decline in Q2, falling to ₹956 crores from ₹1,413 crores in the previous year. The washing machine business also declined by 3% during the quarter.

Dixon Financials

Beyond the GST impact, other specific issues contributed to the slowdown in particular business lines. The refrigerator segment experienced additional “subdued growth” due to the introduction of new, more stringent energy-efficiency norms in India. The AC market also remained weak, which affected the major sector.

The Pivot to High-Margin Component Manufacturing

The company’s joint venture, Rexxam Dixon Electronics, reported a relatively weak quarter. Management attributed this specifically to subdued demand in the air conditioning (AC) market. Mobile and EMS revenue grew 41% in Q2, acting as a buffer against the slowdown in appliances and TVs. The consolidated net profit still grew 81% year-on-year to ₹746 crore.

This impacted its Q2 performance, with revenue growing “only” 33% to ₹15,351 crore compared with 100% in Q1FY26. Also, the revenue base has grown, so it’s no longer possible to maintain triple-digit growth rates. However, they emphasized that growth remains “aggressive” and that demand could pick up.

The Smartphone Engine

Management remains optimistic, targeting an aspirational revenue goal of ₹1 lakh crore within the next three to four years, suggesting they view the Q2 slowdown as a temporary hurdle. The mobile segment is expected to remain the primary engine of growth. Dixon aims to deliver 55-65 million units in FY27, from 40-42 million in FY26.

A 51:49 Joint Venture (JV) with Vivo is progressing toward approval, which is expected to provide a major push to future numbers. Additionally, a 74:26 JV with Longcheer is expected to be operational by April 2026, targeting 8 to 10 million units in its first year.

Manufacturing for a new large global smartphone ODM is slated to begin in Q4 of FY 25-26 or Q1 of the next fiscal, with expected monthly volumes of approximately 0.5 million units. A new 1 million-square-foot mobile manufacturing campus in Noida is on track to be completed by March 2026 to support anchor customers.

Vertical Integration: Deepening the Moat via Components

A core component of Dixon’s outlook is the “deepening of the moat” through component manufacturing. It plans to invest about ₹3,000 crore over the next three years towards this. Through its JV with HKC, Dixon is creating capacity for 24 million smartphone display modules in the first phase, eventually expanding to 60 million units to cover 80% of captive consumption.

This segment is expected to deliver high double-digit margins. Through the acquisition of a 51% stake in Kunshan Q Tech Microelectronics, Dixon plans to scale smartphone camera module annual production capacity from 40 million units to 190–200 million units within two to three years, targeting revenues of ₹6,000 to ₹7,000 crores.

#2 Kaynes Technologies

Kaynes Technologies is another leading EMS player. It provides design, process, engineering, and life-cycle support to original equipment manufacturers. The company caters to multiple industry verticals, including automotive, aerospace, defence, and railways. It is transforming from a pure EMS provider to an integrated ESDM company. Towards this end, it has several ongoing projects.

The Trust Deficit

Kaynes’s stock has fallen from recent highs amid shaken investor confidence over financial reporting and transparency. A critical report from a major brokerage raised questions about related-party disclosures, working capital trends, and cash flow.

Kaynes Financials

Transparency Concerns and Working Capital Stress

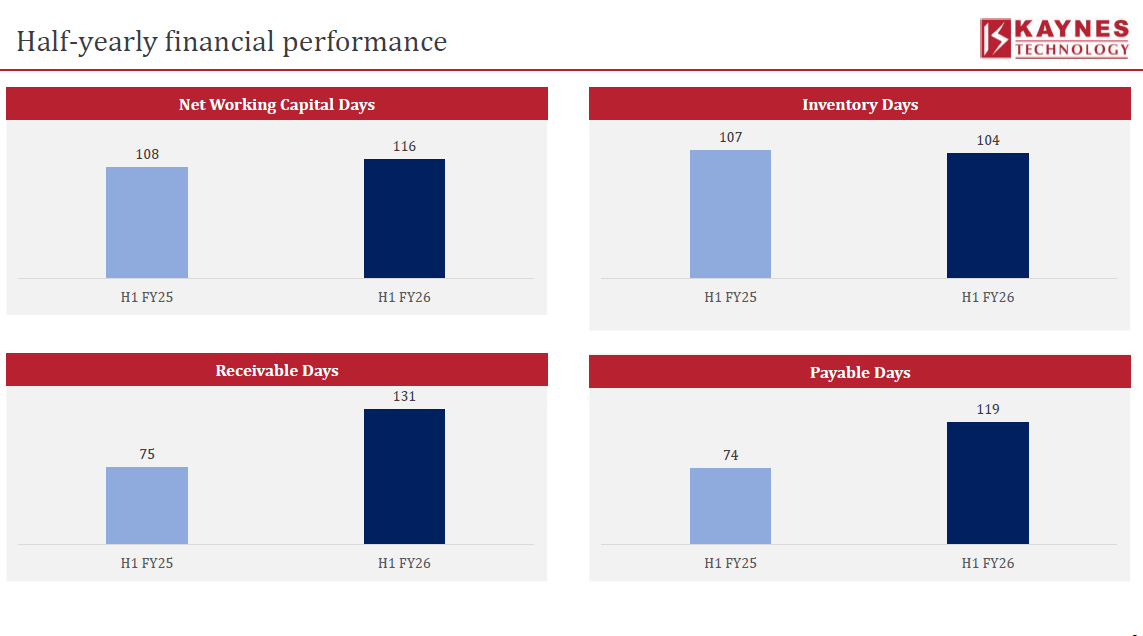

While growth was good, management noted specific operational challenges during this period. Net working capital days increased to 116 days from 108 days last year. Management attributed this increase to higher inventory levels (131 days). The company also noted a billing skew toward the end of quarters, resulting in higher receivables.

Management is implementing strategies. It has outlined measures to address the inventory crisis, including the 2026 Recovery Roadmaps, such as invoice discounting and vendor-managed inventory, to reduce these numbers by the end of the year. It also reported a negative cash flow of ₹180 crore. Management expects this to improve with volume growth in H2.

The company’s H1FY26 performance demonstrated strong growth. Total revenue increased 47% year-over-year to ₹1,580 crore. Operational EBITDA increased 75% to ₹261 crore, while margin expanded 270 bps to 16.5%. Net profit also increased 77% to ₹196 crore.

In terms of revenue mix, industrial (including electric vehicles) accounted for 59%, followed by automotive (24%), railways (7%), and other verticals. Performance was good, but the report cited a lack of related-party disclosures and cash flow issues, which led to a decline in its share price. Its order book stood at ₹8,099.4 crore, providing revenue visibility of over 3 years.

Scaling the Sanand OSAT and PCB Facilities

Kaynes has transitioned from an EMS player to a fully integrated Electronic System Design and Manufacturing (ESDM) company. The Sanand OSAT facility is currently operational and ramping up for nationwide mass production by January 2026.

It has also received government approval for advanced printed circuit board projects, including an upcoming multilayer HDI PCB facility in Chennai. This facility will help Kaynes gain a share of the domestic PCB manufacturing market, which is growing at a compound rate of 20%.

The ₹18,000 crore Revenue Target

Kaynes maintains an aggressive growth outlook, specifically targeting revenues of USD $1 billion (₹9,000 crore) by FY28 and USD $2 billion (₹18,000 crore) by FY30. This target is based on clear visibility to FY28, supported by strong momentum and robust order inflows.

Beyond semiconductor and PCB manufacturing, the aerospace and defence segment is expected to see strong growth in FY27 following final approval from a major U.S. customer later this year. It expects high-performance computing servers for the export market and high-end consumer work to drive a significant portion of its business growth.

#3 PG Electroplast:

PG Electroplast manufactures PCBs and plastic components, including various types of plastic molding. The company’s products are used across industries, including consumer electronics (coolers, air conditioners), automotive, and home appliances.

It is a major manufacturer of air conditioners. PG is the first beneficiary of the PLI scheme designed for AC components, which helped it expand rapidly. Its clientele includes leading OEMs, such as LG Electronics, Jaguar, Kohler, Whirlpool, Godrej, AO Smith, Acer, Voltas, Orient Electric, Blue Star, and Crompton, among others.

The AC Crisis

The company experienced a slowdown in the second quarter and the first half of FY26. The early arrival of monsoons in the first half significantly impacted the air conditioner business. The GST reduction announced on 15 August 2025 further impacted this, leading customers to postpone purchases in anticipation of lower prices.

This led to elevated inventory levels in the sales channels, estimated at 1.5 to 2 million units as of 1 November 2025. Management noted that primary sales in the industry had fallen by 20-25%, while secondary sales had declined even further. Due to the order stock being stuck, there has been a delay or slowdown in brands filling the channels with new inventory.

The Inventory Crisis and the 2026 Recovery Roadmap

Management expects FY26 to be a measured year focused on consolidation and operational discipline, with recovery expected in the second half of FY26. It expects GST rationalization to boost growth in the medium term through penetration. This, along with inventory normalization and the introduction of new energy rating norms, could help drive growth again.

As a result, the AC business contributed ₹131 crores in Q2, representing a decline of nearly 45% compared to the same quarter the previous year. The drop in net profit during the quarter was largely attributed to lower operating leverage resulting from the reduced sales volume in the AC segment. Additionally, operating margins were softened by higher supply costs.

Revenue for the quarter declined 2.4% year-on-year to ₹655.4 crore. EBITDA declined 26.2% to ₹44.7 crore, while margins narrowed to 6.8% from 9% in Q2FY25. The company’s net profit fell severely by 85.7% to ₹2.8 crore. Operating and free cash flow turned negative in H1 2026 due to elevated inventory levels.

Revenue Diversification

Beyond AC, the washing machine business performed well, growing 55% in Q2 and contributing ₹188 crore to sales. To diversify its revenue, management is entering new categories such as refrigerators, which are expected to start contributing by Q2FY27.

PGEL has entered into an agreement with PAX Global for point-of-sale machines, with pilot production scheduled to start in Q3FY26. Management aims for the washing machine business to contribute about 15% of total revenue in the medium term, up from the current 11–12%.

The company has signed memorandums of understanding for a long-term investment of ₹1,000 crore in Maharashtra and Andhra Pradesh. This investment will be made over the next 4-5 years to support future growth. While long-term growth could rebound, short-term pressure persists.

Guidance Reset

The company has lowered its FY26 guidance. It expects consolidated revenue to be approximately ₹6,550-6,650 crore. Net profit is projected to increase by just 3% to 7% to approximately ₹300 crore.

Comparative Analysis: Valuation vs. Return Ratios

Valuations have cooled significantly across the board after the sharp correction, but they are still not cheap, prima facie. Dixon, which has the best return on capital employed (RoCE) and return on equity (RoE) in the industry, is trading below its historical median valuation but above the industry median.

| Peer Comparison (X) | |||||

| Company | P/E | 3Y Median P/E | Industry Median | RoCE (%) | RoE(%) |

| Dixon | 53.0 | 117.9 | 26.1 | 40.0 | 32.9 |

| Kaynes | 65.5 | 119.9 | 32.0 | 14.3 | 10.7 |

| PG | 65.8 | 56.7 | 26.1 | 19.4 | 14.9 |

| Source: screener.in | |||||

Kayne’s valuation has also fallen below its historical median, but still trades at twice the industry median. PG Electroplast, despite falling 50% from its peak, is still trading at a premium to both its historical and industry media, leaving a very low margin of safety.

The recent correction across EMS stocks is more about a reset in growth and valuation assumptions. Execution risks, short-term demand hiccups, and balance sheet stress points have come into sharper focus, even as order books, capacity expansion, and localisation efforts remain strong.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was not available have we used an alternate but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.