")

In today’s time, when growing interest rates have squeezed corporate margins, the Indian markets are witnessing a flight to quality. While retail momentum often chases price action, super investors Radhakishan Damani and Ashish Kacholia are doing something different.

Two stocks, each owned by one of them in their portfolio, have caught the attention of investors, thanks to their portfolios achieving a rare financial trifecta. These Growth Kings are operating with zero debt, delivering an impressive ROCE above 20%, and maintaining consistent quarter-on-quarter profit expansion.

These stocks have built what we can call the fortress balance sheet and hence thrive while competitors struggle with debt servicing. Let us take a look at these stocks to find out if they have it in them to break big in FY27.

VST Industries Ltd: The 4.5% Yield Giant in Damani’s Portfolio

Established originally as Vazir Sultan Tobacco Company, VST Industries Ltd was incorporated in 1930. It is an associate of British American Tobacco Plc., a global leader in the cigarette industry which is into the manufacturing and trading of Cigarettes, Tobacco and Tobacco products.

With a market cap of Rs 3,767 cr, VST is the 3rd largest player in the domestic cigarette market, and an 8% market share based on volume. Its cigarette brand Total is among the top 10 brands in the industry.

Damani has held a stake in VST since March 2016 at least, which means it is now a decade long holding. He could have bought it earlier, but that’s the oldest data available on Trendlyne. He currently holds 29% stake overall worth Rs 1,079 cr.

VST Industries has a current ROCE of an impressive 21%, which is the same as the industry median.

The company has a current dividend yield of 4.5% which is much higher than the current industry median of 0.8%. Which means for every Rs 100 invested, the company is paying Rs 4.5 annually to the investor as dividends, while industry peers are not able to average even 1.

Also, the company is debt free, and hence free from any high interest payments.

If we look at last 4 quarters, the company has logged a steady growth.

| Quarter | Mar’25 | Jun’25 | Sep’25 | Dec’25 |

| Net Profits/Rs Cr | 53 | 56 | 59 | 60 |

But let us also look at the long-term financials to see if the company has what it would take to sustain these numbers.

The company’s sales jumped from Rs 1,239 cr in FY20 to Rs 1,398 cr in FY25 which is a compound jump of a small 2%. And between April and December 2025, the company has logged sales of Rs 1,007 cr.

EBITDA (Earnings before Interest, Taxes, Depreciation, and Amortization,) saw a downward slide in the same 5-year period.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| EBITDA/Cr | 415 | 411 | 412 | 383 | 353 | 279 |

For the three quarters of FY26 ending December 2025, the company has recorded EBITDA of Rs 242 cr.

Regarding the net profits, VST has seen almost a flat or linear performance in the last 5 years.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Net Profits/Cr | 304 | 311 | 320 | 327 | 302 | 290 |

And for the 3 quarters of FY26 ending December 2025, the company has logged net profits of Rs 175 cr.

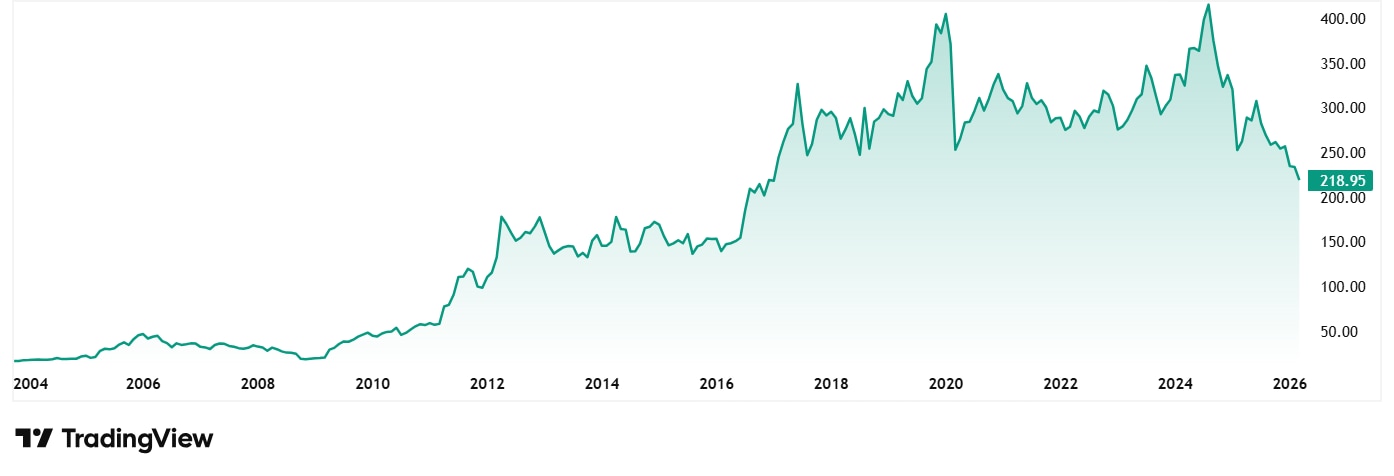

The share price of VST Industries Ltd was around Rs 302 (adjusted for bonus issues) in March 2021 and as of closing on 19th March 2026 it was Rs 222.

The stock is trading closer to its 52-week low price of Rs 213 and at a discount of 56% from its all-time high price of Rs 487.

As for valuations, the stock is trading at a PE of 17x, while the industry median is 21x. The 10-year median PE of VST is 20x and the industry median for the same period is 22x.

VST Industries is a high-yield, zero-debt bet that rewards patience over quick gains. Radhakishan Damani has held this stock for atleast over a decade, likely for its steady cash flow rather than rapid growth. While margins have faced pressure since 2020, the recent quarterly profit climb suggests a quiet comeback.

For most investors, the appeal lies in the 4.5% yield and a valuation that remains cheaper than the industry average. It is a defensive fortress play for a volatile market, backed by one of India’s most disciplined investors.

Fineotex Chemical Ltd: Kacholia’s Debt Free Profit Champ

Incorporated in 1979, Fineotex Chemicals Ltd is engaged in the business of manufacturing auxiliaries and specialty chemicals for textiles, construction, water treatment, fertilizer, leather, and paint industries.

With a market cap of Rs 2,537 cr, the company is one of the leading manufacturers of chemicals for the textiles, construction, water treatment, fertilizer, leather, and paint industries. It provides an entire range of products for the pretreatment, dyeing, printing, and finishing of textile processing to customers across the globe.

Kacholia has held a stake in the company held a stake in the company since the filings for the quarter ending March 2022 as per Trendlyne. He currently holds 2.6% stake in the company worth Rs 65 cr.

Just like VST above, Fineotex has also logged a steady growth in the last few quarters in terms of profits.

| Quarter | Mar’25 | Jun’25 | Sep’25 | Dec’25 |

| Net Profits/Rs Cr | 20 | 25 | 26 | 30 |

If we look at the long-term financials, the company’s sales have recorded a compound growth of 22% from Rs 196 cr in FY20 to Rs 533 cr in FY25. And for the 3 quarters of FY26 ending in December 2025, the sales logged were Rs 459 cr.

EBITDA jumped from Rs 35 cr in FY20 to Rs 127 cr in FY25, which is a compound jump of 29%. And for the first 3 quarters of FY26, EBITDA of Rs 91 cr has been logged.

The net profits grew from Rs 14 cr in FY20 to Rs 109 cr in FY25, recording a compound growth of 40%. And for the 3 quarters of Fy26 ending in December 2025, profits of Rs 81 cr have been logged by the company.

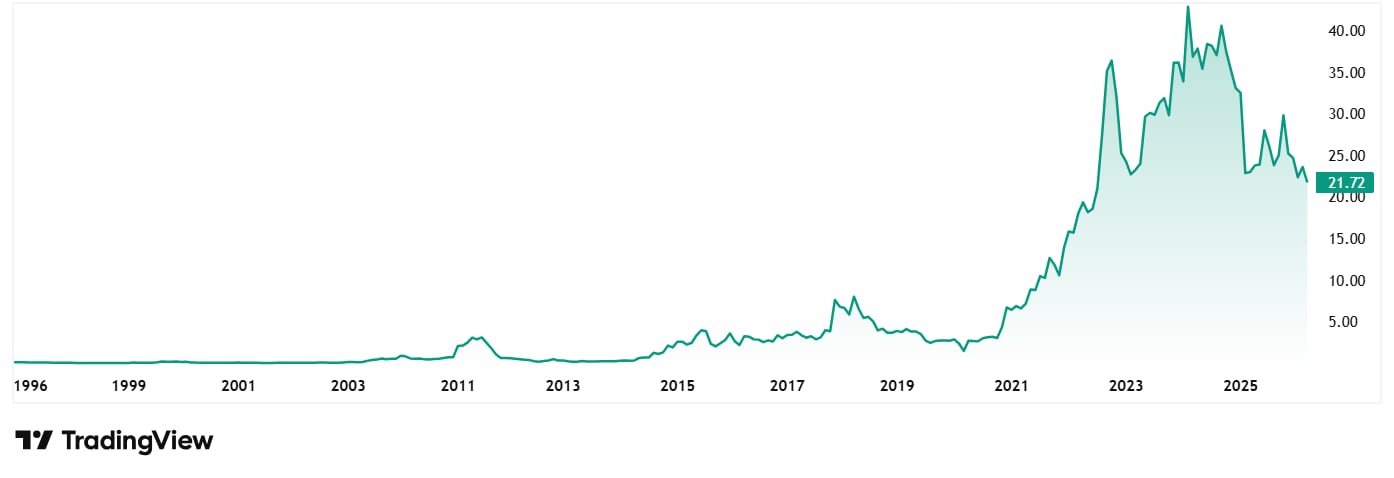

The share price of Fineotex Chemical Ltd was around Rs 6 in March 2021 and as of closing on 19th March 2026 it was Rs 22, which is a jump of over 240% in 5 years.

At the current price, the stock is trading near its 52-week low of Rs 19 and at a discount of 59% from its all-time high of Rs 46.

The company’s share is trading at a current PE of 26x, which is closer to the current industry median of 25x. The 10-Year median PE for the company is 24x while the industry median for the same period is 29x.

As per the February 2026 investor presentation, Fineotex acquired a controlling stake in CrudeChem Technologies Group on 9 Dec 2025 (US-based), which is a specialty chemical manufacturer of advanced chemical fluid additives and comprehensive oilfield chemical solutions.

Fineotex shows the high-velocity side of Ashish Kacholia’s portfolio. While many specialty chemical firms have struggled with volatile raw material costs, Fineotex has maintained a debt-free balance sheet and a consistent quarterly profit climb. Its recent acquisition of CrudeChem Technologies signals a strategic shift toward the high-margin US oilfield market, evolving beyond its textile roots.

So, the stock offers a rare blend of massive historical growth and a current valuation discount, making it a standout Growth King that aligns with Kacholia’s penchant for scalable, capital-efficient businesses.

Patience, Profits, and the Power of a Clean Slate

The contrast between Radhakishan Damani’s VST Industries and Ashish Kacholia’s Fineotex Chemical is ultimately a matter of speed. One offers the slow, rhythmic yield of a defensive stronghold. While the other provides the high-velocity expansion of a global challenger. Yet, they are tethered by the same iron logic: in a world of rising interest rates and thinning margins, a debt-free balance sheet is the ultimate luxury.

While retail momentum often chases the noise of the day, these super investors have anchored their portfolios in companies that own their own future. VST provides a 4.5% yield for the patient, while Fineotex uses its capital efficiency to pivot toward high-margin American oilfields. Both firms have built financial fortresses that thrive precisely because they are free from any interest payments.

As we look toward FY27, the primary question for investors is if the broader market will catch up to the value of boring excellence or will these be the dead horses in the portfolios? For now, adding these stocks to a watchlist and keeping an eye on them seems like a good plan.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.