India’s digital infrastructure has expanded rapidly over the past decade. Internet access has widened across cities and villages. Data has become cheaper and more accessible. Government data highlights a sharp rise in connectivity and broadband reach in recent years. This shows how deeply digital adoption has taken root in the country. (Source: PIB)

This shift is not just about usage. It is about the backbone that supports it. Towers, fibre networks, and telecom equipment are enabling this growth. Every video streamed, payment made, or app used depends on this infrastructure. As data demand rises, these assets become more critical. The real story lies behind the screens, in the networks that carry this traffic.

This also makes it a timely theme for investors. Data consumption continues to grow. 5G rollout is still underway. Rural connectivity is expanding through large government projects. Businesses are moving to cloud and digital platforms. At the same time, India still has room to catch up with global digital capacity. This creates a long runway for growth.

The stock selection reflects this full ecosystem. One part focuses on stable, asset-heavy businesses with predictable income. Another captures companies building the fibre backbone. One adds exposure to telecom technology and future upgrades. The last represents network ownership and monetisation. Together, they avoid overlap and cover the entire chain. This makes the basket balanced rather than repetitive.

#1 Indus Towers: The rental giant of Indian telecom

Indus Towers is engaged in the business of setting up, operating and maintaining wireless communication towers.

Indus Towers reported a steady Q3 FY26 performance. The numbers reflect continued demand for telecom infrastructure. Revenue for the December quarter came in at Rs 8,150 crore. This was up 7.9% year-on-year (YoY). Growth was driven by higher tenancy additions and increased loading on existing towers. Core rental revenue rose 9.5% YoY, showing strong underlying demand.

On the operational side, the company added over 3,500 towers during the quarter. It also added more than 6,000 colocations. This indicates ongoing network expansion by telecom operators. Indus continues to capture a meaningful share of these rollouts. The total tower base now stands at over 2.7 lakh sites. The tenancy ratio remains stable at 1.6, pointing to efficient asset use.

Operational resilience: Expanding the tower footprint and tenancy ratio

The broader industry trend remains supportive. Data usage continues to rise across the country. 5G rollout is still in progress. While new tower additions may slow, network densification is picking up. This means more equipment is being added on existing towers. The company also expanded into remote and strategic areas. This includes deployments in Lakshadweep and defence locations.

Profitability Audit: One-off impacts vs. adjusted core growth

Profitability declined on a reported basis. Net profit stood at Rs 1,780 crore. This was down 55.6% YoY. The drop was due to one-off gains in the previous year. Adjusted profit growth remained positive. This indicates stable core performance. Cost control efforts also continued. Lower diesel usage and higher solar adoption supported margins.

Looking ahead, growth remains tied to telecom capex. The company has a strong order book. Tenancy additions are expected to remain healthy. Tower additions may moderate over time. The company is also exploring global expansion. Africa remains a long-term opportunity. Overall, Indus Towers remains a key enabler of India’s telecom backbone. It plays a central role in supporting rising data demand.

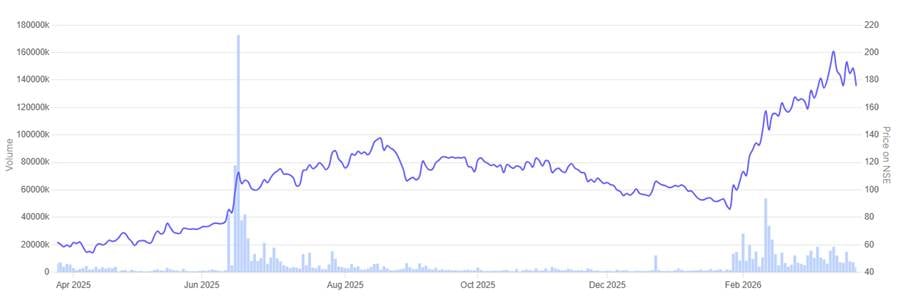

In the past year, share price of Indus Towers rallied 19.4%.

Indus Towers 1 Year Share Price Chart

#2 Sterlite Technologies: Betting on global fiber recovery

Sterlite Technologies (STL) was established in July 2001 after the demerger of the telecom division of Sterlite Industries (SIL). In July 2006, STL acquired the transmission line business of SIL to foray into the power transmission cables business.

STL has grown over the years to become the largest optical fibre and optical fibre cables manufacturer in the country. The company also has sizeable presence in the overseas markets with an established presence in the global optical fibre market.

Sterlite Technologies reported a steady Q3 FY26 performance, reflecting recovery in the optical networking business. Revenue for the quarter stood at Rs 1,257 crore up 26% YoY. This showed continued growth driven by higher volumes and improved product mix.

Net loss stood at Rs 17 crore, which is lower compared to a loss of Rs 24 crore reported in the same period last year. This indicates a turnaround at the profitability level, supported by better execution and operating discipline.

The turnaround story: Revenue growth amidst global expansion

The company’s core optical business saw strong traction during the quarter. Revenues from this segment came in at Rs 1,174 crore, supported by rising demand for fiber and connectivity solutions. Growth was driven by global telecom and data infrastructure investments. The company remains positioned at the center of three key cycles. These include fiber-to-the-home expansion, data center build-outs, and 5G rollout. These trends continue to drive long-term demand for optical networks.

Order inflows remained strong. The company reported order wins of over Rs 4,200 crore during the year so far, up over 40% YoY. This was led by data center connectivity projects and entry into Tier-1 telecom customers in North America. The order book stood above Rs 5,300 crore, providing clear visibility for future execution. A significant portion of this is expected to be executed over the next few quarters and into FY27.

Order book visibility: Capitalising on the Data Center build-out

Global exposure continues to be a key driver. North America now contributes a higher share of revenues. The company is also strengthening its presence in Europe and Southeast Asia. It is investing in local manufacturing and expanding its footprint to serve global clients. At the same time, projects like BharatNet in India are expected to support domestic demand over the medium term.

Margins, however, remain under pressure in the near term. This was impacted by tariff-related costs in the U.S. market. The company has initiated mitigation measures. These include passing on part of the cost to customers and increasing local production in overseas markets.

From a strategic standpoint, the company continues to focus on next-generation technologies. It is investing in high-density fiber, data center solutions, and low-latency networks. These are aligned with rising demand from AI-led infrastructure. New product launches and global trials indicate a shift towards higher-value offerings. This is expected to improve margins over time.

Looking ahead, growth remains linked to global digital infrastructure spending. Demand from data centers and telecom networks is expected to stay strong. At the same time, execution risks such as tariffs and supply chain constraints remain. Overall, Sterlite Technologies continues to play a key role in building the fiber backbone of the telecom ecosystem, making it a critical but less visible enabler of the digital economy.

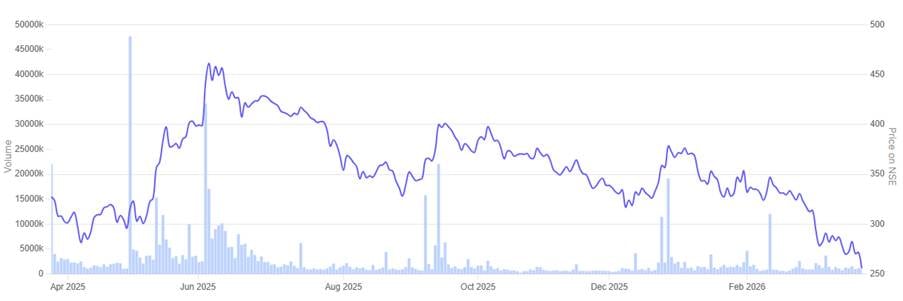

In the past year, share price of Sterlite Technologies surged 197.1%.

Sterlite Technologies 1 Year Share Price Chart

#3 Tejas Networks: The Tata-backed play on India’s 5G backbone

Incorporated in 2000, Tejas Networks (TNL) designs and manufactures wireline and wireless networking products, with a focus on technology, innovation and R&D. TNL carrier-class products are used by telecom service providers, utilities, governments, and defence networks in 75+ countries

Tejas Networks reported a modest improvement in revenue for Q3 FY26, but profitability remained under pressure as the company continues to transition its business model. Revenue for the quarter stood at Rs 307 crore, which is quite lower from Rs 2,642 crore reported a year ago.

However, the company reported a net loss of Rs 197 crore, compared to a profit of Rs 166 crore reported a year ago. This reflects continued stress on earnings amid high costs and delayed project execution.

Navigating the transition: Addressing revenue volatility and working capital

The quarter was largely driven by wireline products, with strong supplies to Indian private telecom operators and select international customers. The company is increasingly positioning itself as a core supplier in telecom backhaul and broadband infrastructure. This places it within the backbone layer of the telecom ecosystem, where optical and routing equipment support data traffic growth across networks.

Order inflows showed some improvement. The order book rose to Rs 1,329 crore, indicating gradual traction. A significant portion continues to come from India, especially government-led and large-scale network projects. The company also secured additional packages under BharatNet Phase 3, where it is supplying routers for backbone connectivity. Execution of these projects is expected to be spread over the next two years.

However, delays in key projects remain a concern. The much-anticipated BSNL 4G expansion order has not yet been received. This has impacted revenue visibility and led to elevated inventory levels. The company had already procured equipment in anticipation of this order. As a result, working capital remains stretched, and execution timelines have shifted to the next financial year.

On the growth front, Tejas is focusing on expanding its wireless portfolio. Multiple 4G and 5G trials are underway in India and overseas markets. Several of these engagements have moved to the commercial negotiation stage and are expected to convert into orders in the coming months. The company is also seeing early traction in private 5G deployments across sectors such as ports and mining.

International business is emerging as a key area of focus. The company is engaging with operators across Europe, Africa, Latin America, and Southeast Asia. Partnerships with global players are helping it enter new markets. It has also secured wins in areas such as optical backbone networks and network transformation projects. These moves are aimed at reducing dependence on domestic government contracts over time.

R&D and Global trials: Reducing dependence on domestic contract

The company is also entering newer segments within telecom infrastructure. It recently secured its first order for networking inside a data center, marking a shift beyond traditional interconnect solutions. This aligns with rising data traffic and increasing investments in AI-driven data infrastructure, where high-capacity networks are critical.

Despite these developments, profitability remains linked to scale. Management indicated that margins in international markets are higher compared to India, where pricing remains competitive. The path to profitability depends on scaling global business and improving product mix. Continued investments in R&D, especially in 5G and future technologies, are expected to keep costs elevated in the near term.

Going ahead, the company’s outlook hinges on timely execution of large domestic projects and conversion of international opportunities. Demand for telecom infrastructure remains strong, supported by data growth and network expansion.

However, delays, high working capital, and ongoing losses continue to weigh on near-term performance. Tejas Networks remains a key but under-the-radar player in the telecom value chain, with its growth tied to the broader expansion of digital connectivity infrastructure.

In the past year, share price of Tejas Networks declined sharply by 50.9%.

Tejas Networks 1 Year Share Price Chart

#4 RailTel Corporation of India: Monetizing the Indian Railways’ fiber goldmine

RailTel Corporation of India was incorporated in 2000, with the objective of creating nationwide broadband and virtual private network (VPN) services, telecom, and multimedia network, to modernise the train control operation and safety system of Indian Railways.

It is a Navratna public sector undertaking (PSU) of the Government of India. At present, RailTel’s network passes through around 6,000 stations across the country, covering all major commercial centers.

RailTel Corporation of India reported steady growth in Q3 FY26, reflecting its role as a key digital infrastructure provider within the telecom ecosystem. The company posted operating revenue of Rs 913 crore for the quarter, marking a YoY growth of about 19%.

Net profit for Q3 FY26 stood at Rs 62 crore which is slightly lower compared to Rs 65 crore profit reported in same quarter last year.

The growth in revenue was driven by both telecom services and project execution. The telecom segment contributed around Rs 349 crore, while the project segment accounted for Rs 564 crore. Despite higher revenues, profitability remained relatively stable, with profit before tax slightly lower year-on-year due to a higher share of low-margin project work during the quarter.

RailTel operates at the backbone level of India’s telecom network. Its core business includes national long-distance fiber, internet services, and enterprise connectivity. Within telecom, the company continues to focus on NLD traffic and capacity expansion. However, pricing pressure in the sector has impacted growth in this segment, with margins remaining under strain.

Scaling the portfolio: From NLD fiber to smart ICT solutions

To offset this, the company is investing in capacity upgrades and network expansion. Capex has been ongoing over the past two years, aimed at strengthening fiber infrastructure and improving network throughput. Management indicated that these investments are expected to support growth in the coming quarters.

RailTel is also expanding into data center and digital infrastructure services. A key data center project is under construction and is expected to be ready by March 2027. In parallel, the company has started smaller edge data center operations across locations such as Gurugram, Mumbai, and Indore. These are expected to gradually contribute to revenues from the next financial year.

On the project side, railway-led initiatives remain a major growth driver. The company is executing orders under the Kavach safety system, including two confirmed orders worth about Rs 468 crore in the East Central Railway. Deployment is underway, including tower installations and network infrastructure rollout. Additional tenders are in progress, which could further expand this pipeline.

The Railway Catalyst: Kavach safety systems and order pipeline

The broader order book remains strong. The company indicated an overall order pipeline of around Rs 8,400 crore, combining telecom and project segments. This provides visibility for future growth, especially as railway signaling, safety systems, and digital connectivity projects scale up.

RailTel is also exploring opportunities beyond its core railway ecosystem. It has ongoing engagements in areas such as smart classrooms, hospital management systems, and enterprise information and communication technologies (ICT) solutions. While margins in these projects remain moderate, they help diversify revenue streams and improve utilisation of network infrastructure.

Looking ahead, management has guided for around 20% growth, supported by project execution and gradual recovery in telecom services. However, margins are expected to remain mixed, with telecom offering higher margins and project business staying relatively lower.

Overall, RailTel continues to position itself as a critical yet less visible layer of India’s telecom and digital infrastructure. Its performance will depend on execution of large government-led projects and its ability to monetise its fiber and data infrastructure.

In the past year, share price of Railtel Corporation of India tumbled 23.1%.

Railtel Corporation of India 1 Year Share Price Chart

Comparative Analysis: Finding the relative value in EV/EBITDA and ROCE

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | 5-Year Average EV/EBITDA | Industry Median | ROCE | ROE |

| 1 | Indus Towers | 7.1 | 6.1 | 21.3 | 29.0% | 32.5% |

| 2 | Sterlite Technologies | 18.3 | 11.4 | 12.0 | 2.9% | -6.3% |

| 3 | Tejas Networks | -27.8 | 30.8 | 12.0 | 15.5% | 12.5% |

| 4 | Railtel Corporation of India | 12.3 | 15.0 | 19.8 | 21.8% | 16.5% |

Indus Towers is the clear outlier when it comes to returns. Return on Capital Employed (ROCE) is 29.0% and Return on Equity (ROE) is 32.5%. That is much higher than the rest. RailTel is also decent with ROCE of 21.8% and ROE of 16.5%. Tejas Networks is lower at 15.5% ROCE and 12.5% ROE. Sterlite Technologies is struggling here. ROCE is only 2.9% and ROE is negative at -6.3%.

Valuations are telling a different story. Indus Towers is at 7.1 times EV/EBITDA. This is close to its 5-year average of 6.1 and far below the industry median of 21.3. RailTel is at 12.3 times, again below its own average of 15.0 and below the industry median of 19.8.

Sterlite Technologies is more expensive at 18.3 times. This is higher than its 5-year average of 11.4 and also above the industry median of 12.0. Tejas Networks is loss-making, so EV/EBITDA is at -27.8, compared to a 5-year average of 30.8.

If you look at the business side, they are not the same. Some are stable, some are still building. Data usage is going up. 5G rollout is still happening. This is pushing demand for towers, fibre and network equipment. These companies sit behind all of this. They don’t sell data. They make sure it flows.

Indus Towers runs a rental model. RailTel mixes fibre network with project work. Sterlite is tied to fibre demand but margins are still weak. Tejas depends on large orders, which don’t come evenly. So performance can swing. Together, they give a good sense of how the telecom backbone story is playing out.

The long-term play: Execution as the final differentiator

In the end, this is a simple story. More data is being used every year. Networks are getting upgraded. That means more towers, more fibre and more equipment on the ground. These companies sit in that layer.

But the numbers will not always look smooth. One quarter can be strong. Another can look weak. A lot depends on when orders come and when they get executed. That is why some companies show steady performance, while others look uneven.

There is also a difference in business models. Companies that own assets like towers or networks usually show more stable earnings. Those who supply equipment or technology depend on orders. So their performance can move up and down.

The opportunity is there for everyone. But outcomes will differ. The ones who manage execution well and keep margins under control are likely to do better over time.

So this is not a short-term theme. It is something to watch over a longer period. These are not front-facing names, but they are part of the backbone that keeps the whole system running.

You can track how these companies progress with the advent of digital infrastructure by adding these stocks to your watchlist.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.