")

India’s need for cold storage is rising fast. People are buying more fresh and frozen food. E-grocery and quick commerce want tighter delivery windows. Pharma, vaccines, seafood, dairy and meat also need temperature control from factory to customer. When the chain breaks, quality drops. So does the price farmers and suppliers get.

The Indian cold chain market, valued at Rs 2.28 trillion in 2024, is projected to expand at a double-digit CAGR through 2028. This growth is being supercharged by the $5 billion quick-commerce sector, where sub-15 minute delivery requirements are forcing a structural shift from massive rural warehouses to urban micro-fulfilment centers.

The Urban Shift: From Rural Warehouses to Micro-Fulfilment

The infrastructure is improving, but the gap is still visible. India has thousands of cold storages spread across states, but capacity is uneven and still not enough for rising demand. Many facilities are concentrated near production hubs, while consumption centres and smaller towns remain under-served.

A large part of existing storage is also used mainly for single commodities, such as potatoes, limiting flexibility. Government data and industry studies show that current facilities fall short of what the food and pharma supply chain requires, especially for multi-temperature and modern integrated cold-chain networks.

The Multi-Temperature Gap: Why Integrated Networks are Winning

That is why this is an opportunistic time to track cold-chain plays. Policy support is active. The government’s Cold Chain scheme under PMKSY focuses on building end-to-end infrastructure. It covers packhouses, pre-cooling, reefer transport and storage. National logistics programmes such as PM GatiShakti are also improving connectivity and reducing delays across supply chains.

In this backdrop, the stocks chosen in this article are picked for clear exposure to the theme. They are not random logistics names. They sit closest to cold storage, temperature-controlled warehousing, and refrigerated movement. They also have operating scale and client linkages that can benefit as capacity expands and utilisation improves. The aim is simple. Stay aligned to cold storage and refrigerated logistics, not the entire transport universe.

#1 Snowman Logistics: Analyzing the Rs 150 Crore Annual CapEx Strategy

Incorporated in 1993, Snowman Logistics is an integrated temperature-controlled logistics service catering to the logistical requirements of its clients.

Analyzing Snowman Logistics’ ₹150 Crore Expansion

Snowman Logistics is moving ahead with a gradual expansion plan, focused mainly on building its own cold storage capacity. The management said the company intends to spend about ₹100–150 crore every year, largely on setting up two to three new warehouses on owned land. Some facilities will also be developed under build-to-suit arrangements, while limited spending will continue on transport and alternative fuel vehicles.

The company is balancing ownership and leasing based on location and cash flow. In large and stable markets, it prefers to own land and develop warehouses. In other cities, it continues to operate from fully leased facilities. New centres are being planned in line with local demand and market maturity. The company is yet to declare its Q3 results.

On the transportation side, Snowman is working on improving efficiency. Trucks and vehicles that were running at a loss are being removed. The remaining ones are being fixed up or changed so that they run better and cost less to maintain. Leasing is being used more actively to improve asset use and reduce downtime.

Management said recent capacity additions had affected utilisation and margins. These are expected to improve as volumes pick up. With disciplined capital spending and operational tightening, Snowman is aiming for steady, long-term growth in the cold-chain logistics space.

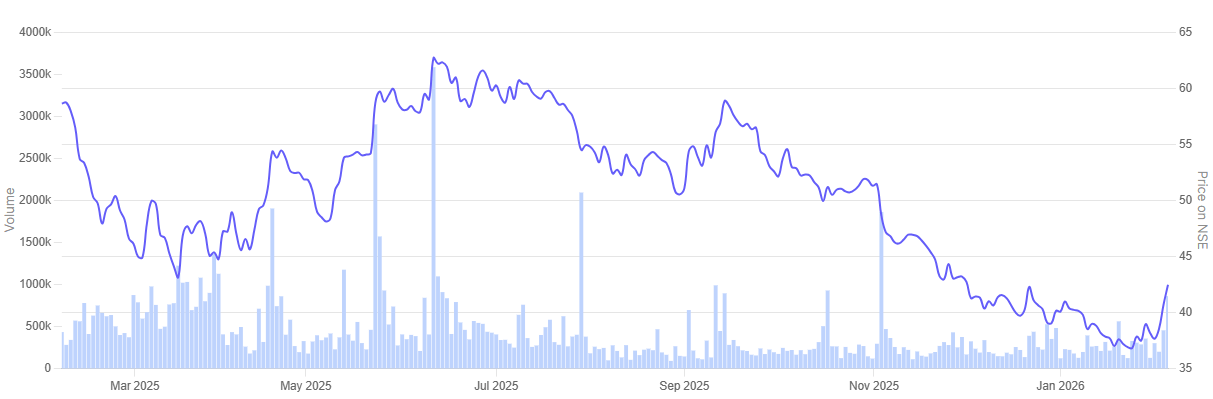

In the past year, Snowman Logistics share price has tumbled 27.7%.

Snowman Logistics 1-Year Share Price Chart

#2 Mahindra Logistics: The Pivot from ‘White Space’ to Profitability

Mahindra Logistics is an integrated logistics & mobility solutions provider. The company offers supply chain expertise to diverse industry verticals such as automotive, engineering, consumer goods, pharmaceuticals, telecommunications, commodities, and e-commerce.

Mahindra Logistics is focusing on operational consolidation after a long turnaround phase.

During Q3 the company returned to profitability after eleven consecutive loss-making quarters, following tighter execution and sharper cost controls. Revenue rose 19% year-on-year (YoY) to Rs 1,898 crore. Express volumes grew by 19%, and gross margins improved from 0.2% to 2.4%. The emphasis has now shifted to improving asset utilisation and customer quality rather than rapid expansion.

A key priority is reducing under-utilised capacity, or “white space”. The Mahindra group company has set a target to cut this by about 95% cent by September 2026.Visible benefits are expected over the next three quarters. This is expected to lift productivity across warehouses and transport networks. Fleet additions are being made selectively on high-demand routes, with capital spending linked closely to utilisation and return thresholds.

The business remains closely linked to the auto sector, which contributes sixty-two per cent of revenue. The Mahindra Group accounts for 58% of total top line revenue, underlining concentration risks. Management is working to increase exposure to e-commerce, manufacturing, and consumer goods.

Internationally, the joint venture with Japan’s Seino is being scaled gradually. Revenues are still limited, as Japanese clients follow long approval cycles.

With stable leadership, improving utilisation, and cautious capital deployment, Mahindra Logistics is aiming for steady and sustainable growth in a competitive logistics market.

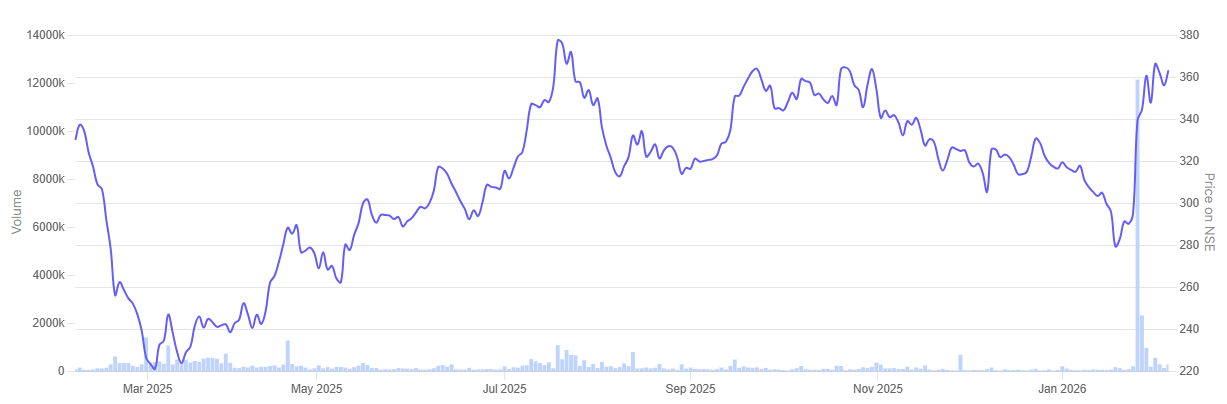

In the past year, Mahindra Logistics share price was up 9.5%.

Mahindra Logistics 1-Year Share Price Chart

Valuation Check: Is the Infrastructure Premium Justified?

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| 2 | Mahindra Logistics | 11.3 | 18.7 | 5.6% |

| Industry Median | 11.5 | – | 14.3% |

Snowman Logistics is trading at an EV/EBITDA multiple of 10.9, compared with its five-year average of 12.2. The stock is trading at a lower valuation than it did in the past. But returns are still weak. ROCE is only 4.2%. This shows the company is yet to get strong results from the capital it has put in.

Mahindra Logistics is valued at an EV/EBITDA multiple of 11.3, below its five-year average of 18.7. This reflects the tough period it has seen in recent years and the cautious mood among investors. Its ROCE of 5.6% is a little better, but still not very strong for a company of this size.

Overall, current valuations appear more reasonable than in the past. Still, investors need to assess whether ongoing improvements in utilisation, margins, and cash generation can be sustained. Only consistent performance will justify higher valuations over time.

Conclusion

Overall, the cold-chain and logistics sector is settling into a more normal growth phase. Capacity is expanding. Networks are improving. Companies are now focusing more on efficiency, costs, and returns than just scale. The easy gains seen after the pandemic are largely over.

From here, results will depend on day-to-day execution. On how fast new warehouses reach healthy utilisation. On how well fleets are managed. On how effectively pricing is protected. Chasing volumes without margins is unlikely to create long-term value.

Stock valuations have come down and look more balanced today. But they are not cheap. Much of the near-term recovery is already reflected in prices. Further upside will need consistent improvement in profitability and cash generation.

For investors, the key is to track strength of the balance sheets, utilisation levels, and management discipline. In this business, steady performers usually win over time. Not the fastest expanders.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.