The Indian infrastructure sector has been under pressure, with valuations compressing across segments.

This slowdown is mainly driven by subdued awarding of projects, which has impacted companies’ order books.

Thus, road construction is expected to come down to 27 kilometers per day in FY26, down from a high of 37 kilometers per day in FY21.

This slowdown has also impacted the share prices of infrastructure companies.

However, the government’s focus on infrastructure remains strong, with a robust bidding pipeline.

Order awarding is also expected to pick up from the third quarter of this financial year, providing a boost to the sector.

We have identified top 5 infrastructure stocks that are currently trading at a discount.

Let’s take a look…

#1 HG Infra Engineering

First on this list is HG Infra Engineering.

HG Infra operates in the infrastructure construction activities across roads and railways.

The company is gradually diversifying into solar power, battery energy storage systems (BESS), and the transmission & distribution sector.

HG is present across 13 states, including Maharashtra, Jharkhand, Uttar Pradesh, Andhra Pradesh, Gujarat, and Rajasthan.

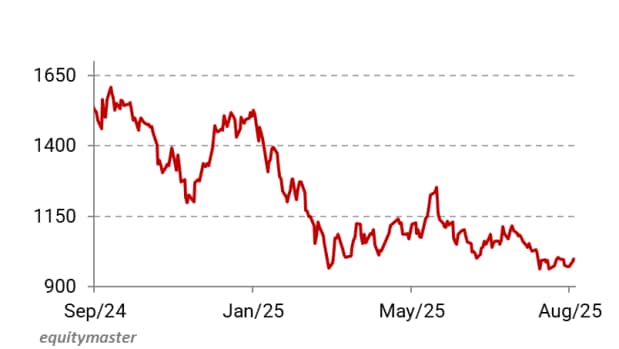

The company’s share price is down 39% from its 52-week high of Rs 1,643.

HG Infra Share Price – 1 Year

Source: Equitymaster

This downtrend is driven by subdued order inflow and financial results.

Revenue and PAT both declined 6% to Rs 50.6 billion (bn) and Rs 5 bn in FY25. The financials were impacted due to the elimination of inter-company transactions in the solar segment.

Furthermore, in Q1 FY26, revenue also fell 3% to Rs 14.8 bn, due to subdued execution. PAT declined 39% to Rs 992.6 million (m) due to lower margins caused by one-time cost effects.

As of 30 June 2025, HG’s order book stood at Rs 146.6 bn. This provides revenue visibility of about 3 years. Road contributes 65.6% to the order book, followed by railways (20%), BESS (11%), and the rest comes from solar.

Looking ahead, the company estimates revenue to grow 17-18% in FY26, in line with its historical growth.

The National Highway Authority of India plans to award 6,376 km of road projects in FY26, worth Rs 3.4 trillion. Accordingly, HG is targeting an order inflow of Rs 110 bn in FY26.

It has already submitted bids for orders worth Rs 160 bn, for which it is awaiting final approval.

HG aims to have 40% of its orders from the non-road sector in the next 2-3 years. Additionally, the company aims to achieve a 5% share of India’s total BESS market.

The company also plans to venture into airports, urban infrastructure, and the water and irrigation sector, to reduce its concentration on the road sector.

#2 KNR Construction

Second on this list is KNR Construction.

KNR is a leading company that provides engineering, procurement, and construction (EPC) services. It has an established presence in roads, irrigation, mining, and urban water infrastructure management.

The company operates across India, with major projects concentrated in the South, including Tamil Nadu, Andhra Pradesh, Telangana, Kerala, and Karnataka.

From a financial perspective, in FY25, revenue rose 7% to Rs 47.5 bn, while PAT surged 33% to Rs 10 bn due to higher other income.

However, sluggish execution due to a low order book is impacting growth. In Q1 FY26, revenue fell 37.7% to Rs 6.1 bn, while PAT declined 26% to Rs 1.2 bn.

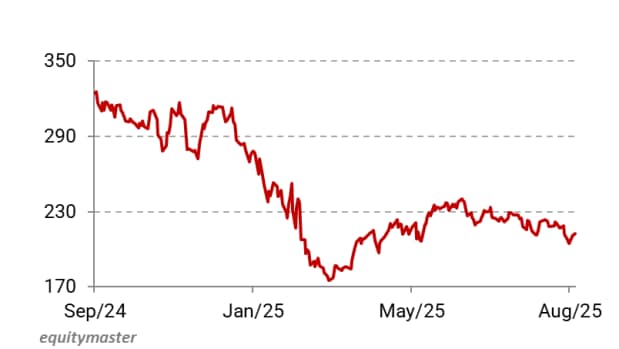

As a result, its share price is down almost 45% from its 52-week high of Rs 360.

KNR Share Price – 1 Year

Source: Equitymaster

This was primarily because most existing projects are nearing completion. The company’s order book stood at Rs 83 bn as of 30 June 2025.

Mining accounts for 43% of the book, followed by roads (27%), irrigation (17%), and pipeline (13%). The order book provides revenue visibility of just about 2 years.

Looking ahead, KNR expects to secure orders worth Rs 130-150 bn in FY26. However, it has guided for a softer FY26 due to delays in order receipts.

The company intends to bid for contracts worth Rs 800-900 bn by the end of March 2026.

KNR is also exploring opportunities with toll developers and expressway projects, while evaluating entry into new segments, including metro, solar, toll, and railways.

#3 KEC International

Third on this list is KEC International.

KEC, a part of the RPG Group, is a major EPC player in infrastructure segments including transmission and distribution (T&D), civil, transportation, oil and gas, renewables, and cables.

The company provides services in diverse sectors, including water, airports, hospitals, data centers, solar energy, and logistics.

On the financial front, revenue grew 9.7% to Rs 218.5 bn in FY25, while PAT grew 64.5% to Rs 5.7 bn. This momentum continued in this financial year as well.

In Q1 FY26, revenue rose 11% to Rs 50.2 bn, driven by robust execution in the T&D business. PAT grew 42% to Rs 1.2 bn, driven by margin expansion.

T&D now contributes 63% to total revenue, compared to 55% in the same quarter last year.

KEC International Share Price – 1 Year

Source: Equitymaster

Looking ahead, KEC’s order book stood at Rs 400 bn, providing revenue visibility of about 2 years. The management estimates revenue growth of about 15% in FY26.

The company holds an L1 position of Rs 60 bn in the T&D business. Moreover, tenders worth Rs 1,800 bn are under evaluation.

The company is also expanding its tower manufacturing capacity to 10,000-12,000 tonnes.

In the cable segment, KEC is doubling the capacity of the aluminum conductor plant, with commercial production expected by the end of FY26.

In the renewable energy, the company continues to bid for select opportunities in solar, wind, and BESS. KEC aims for this business to reach Rs 30-40 bn in the next 2-3 years.

#4 NCC

Fourth on this list is NCC.

NCC is a key player in India’s infrastructure development. The company operates across sectors, including buildings, water pipelines, irrigation, transmission, power generation, and transportation.

Revenue rose 6.6% to Rs 223.5 bn in FY25, while PAT grew 8.4% to Rs 19.2 bn. However, in the first quarter of FY26, revenue has declined 6.3% to Rs 52.1 bn, and PAT rose 3.7% to Rs 1.9 bn.

The reason for the slowdown is the large orders received at the end of March 2025. Revenue from new works is expected to start from September. This will improve growth rates.

NCC Share Price – 1 Year

Source: Equitymaster

Looking ahead, NCC’s order book stood at Rs 700 bn, providing revenue visibility of over three years.

Building construction accounted for 34% of the order book, followed by transport (26%), water and railways (6%), power (22%), mining (7%), and irrigation (5%).

The company has a healthy project pipeline of around Rs 2,500 bn with order inflows of Rs 220-250 bn expected in FY26.

#5 Bondada Engineering

Fifth on this list is Bondada Engineering.

Bondada provides EPC and design services to the telecom, railway, BESS, and renewable energy sectors. In the telecom space, it also provides operations and maintenance services.

It serves a strong clientele, including Airtel, Tata, Ericsson, Reliance Jio, and Coal India.

Revenue almost doubled from last year to Rs 15.7 bn in FY25. In the revenue mix, about 58% came from solar energy, followed by telecom (28%), and products (14%).

PAT increased 150% to Rs 1.1 bn. Bondada reports financial results on a semi-annual basis and has yet to release its FY26 numbers.

Looking ahead, Bondada’s order book stands at Rs 50.4 bn, providing revenue visibility of about 3 years.

Renewable energy accounts for about 72% of the order book, followed by telecom (22%), railways (4%), and others (2%).

Bondada Engineering Share Price – 1 Year

Source: Equitymaster

Bondada has submitted tenders for projects worth Rs 16.7 bn. Tenders worth Rs 46.7 bn have been identified for participation.

The management has set an ambitious target of growing revenue sixfold to Rs 100 bn by FY30, from Rs 15.7 bn in FY25. This growth is expected to be driven by the renewable energy segment.

The company aims to build a portfolio comprising 6 gigawatts (GW) of solar EPC, 2 GW of BESS, and 2 GW of solar independent power producers (IPP) projects.

Conclusion

The infrastructure sector is navigating short-term challenges from weak order inflows and execution delays. Near-term performance will depend on the pace of new project awards.

The stocks mentioned here have decent fundamentals and growth prospects as long as there is a pickup in order inflows.

Instead of relying only on hype, it’s necessary for investors to carefully analyse the company’s fundamentals, including financial performance, corporate governance practices, and growth prospects.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.