Hero Motocorp’s (HMCL’s) strong operating performance was driven by lower commodity prices and cost-saving initiatives. BS6 led the volume weakness (op. lev) and rising RM costs should drag margins over the next 2-3 quarters. We marginally upgrade our EPS estimates, but maintain Neutral rating with TP of ~Rs2,690 (~14x Dec’21e EPS+Rs 100/share for Hero FinCorp).

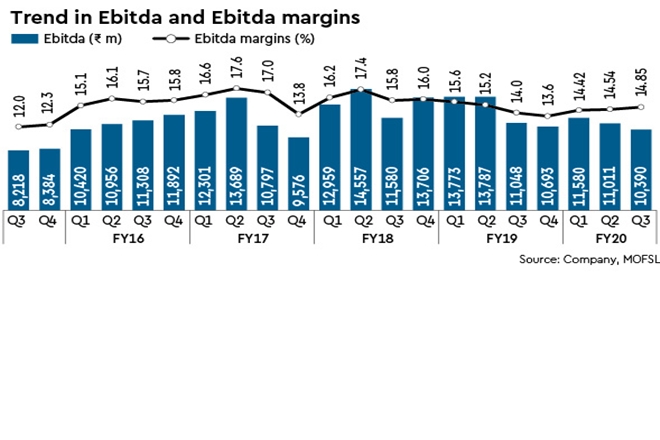

Above estimates; lower RM leads to strong Ebitda margins: Q3FY20 revenues/Ebitda/PAT grew-14%/-6%/ +15% y-o-y and declined 12%/ 15%/8% in 9MFY20. Realisations increased ~4% y-o-y (+1.4% q-o-q) to ~Rs 45.4k (v/s est. ~Rs 44.8k), led by price increase and higher spare sales. Gross margins improved 220bp y-o-y (+110bp q-o-q) due to cost-cutting initiatives as well as commodity prices. Ebitda margins at 14.8% (v/s est. 13.8%), expanded 80bp y-o-y (+30bp q-o-q). Ebitda declined ~6% y-o-y (-6% q-o-q) to ~Rs 10 bn (v/s est. Rs 9.6 bn). Lower tax boosted adj. PAT to Rs 8.8 bn (v/s est. Rs 7.1 bn). The company also declared interim dividend of Rs 65 per share.

Highlights from management commentary: Expects recovery in volumes from 2HFY21. Rural outlook is improving as reflected in strong 10% growth in Jan’20 volumes in agri-dependent states like UP, Gujarat, Maharashtra, etc. Cost-saving initiatives will continue to benefit operating margins, but commodity-cost inflation may offset benefits.

Valuation and view: Near-term demand uncertainty, BS6 transition as well as increasing threat of electrification will keep earnings as well as valuations under check. The stock trades at 14.2x/12.9x FY21/FY22e EPS and it is a fair reflection of EPS growth estimates.