HDFC Ltd. (HDFC IN) reported net profit of Rs 30 bn, down 2% y-o-y and 6% q-o-q. AUM growth was entirely driven by the individual segment (+14% y-o-y/i+2% q-o-q), while non-individual segment AUM declined 9% y-o-y and 4% q-o-q. HDFC has restructured Rs 44.82 bn (0.9% of loan book) under OTR 1 and 2; of which, 38% consists of individual loans and 62% non-individual loans (one large account). Gross stage 3 assets rose 27bp q-o-q to 2.67%, led by a 38bp q-o-q rise in individual loan gross NPLs to 1.37%. Provision cover for stage 3 assets fell to 48.3% from 52.1% in Q4FY21.

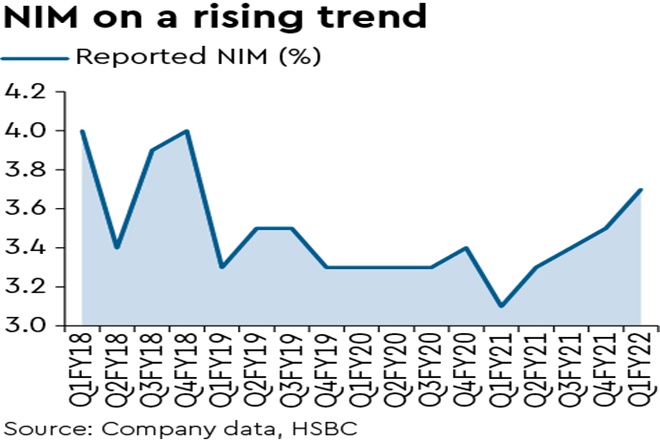

Commentary: Higher NIM during the quarter was driven by lower cost of funds, lower negative carry from excess liquidity, as well as transfer of liquid funds to higher yielding government securities. HDFC expects the low interest rate environment will continue to aid NIM; however, lower rates depress absolute interest income. It believes operating cost reduction in the housing loan business will take time despite digitisation as legal requirements and documentation are too onerous. It expects recoveries to improve once lockdowns subside and legal action can be taken against defaulters.

Earnings outlook improves; maintain Hold: We increase our earnings estimates to factor in higher NIMs as a result of declining funding costs. HDFC will likely deliver a stronger individual loan growth outlook in the medium term compared with developer loans or LRD. However, this will further skew the mix of individual loans from 78% of AUM currently and lead to NIM compression and subdued core-ROEs. As a result, we estimate that HDFC’s core ROEs will remain at c12% in FY21-24e. Hence, we maintain Hold rating and retain our Rs 2,850 TP, which implies 15.8% upside. We also increase our dividend estimates by 43% in FY22e, 18% in FY23e, and 38% in FY24e as we up our dividend pay-out assumptions.

Downside risks: (i) Prolonged impact of Covid 19 can dampen growth and asset quality outlook; (ii) higher competition from banks could impact margins.

Upside risks: (i) Better-than-expected recovery in non-individual segment; (ii) margin expansion due to favourable rate cycle or product mix.