")

The US Federal Reserve, in its latest monetary policy statement (March 15, 2017), Abhishek Anand decided to raise the interest rate by 25 basis points (bps). The statement also projected two more rate-hikes this year. It is just the third time in a decade that the Fed has raised rates. Remember that the Federal Reserve cut its key policy rates close to zero in the aftermath of the financial crisis of 2008 to help reinvigorate the flagging economy. After hitting the zero lower bound (ZLB) it resorted to unconventional policy of quantitative easing. The interest rate was hiked for the first time as late as in December 2015 and again in December 2016. Both the time, the key rate was hiked by 25 bps.

So, what does this shift in the stance of the Fed, from an ultra-easy monetary policy to a gradual approach to

a “tighter” monetary policy mean

for emerging Asian markets (EAM) like India?

Standard economic theory would suggest that a tight monetary policy stance of the Fed should lead to capital flowing back from EAMs to the US, dollar appreciation and upward pressure on inflation. So, will we see a change in RBI’s policy stance to deal with the adverse consequences of the hike?

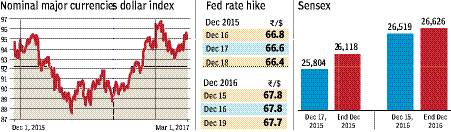

A closer look at the key high frequency economic variables present some interesting trend. Consider, for example, nominal Broad Dollar Index. The Dollar Index, after appreciating marginally in the first couple weeks after the hike, depreciated considerably. The Index depreciated by roughly 2.5% by the end of the second month after December 2015 hike as well as the December 2016 hike.

Economists Reuven Glick and Sylvain Leduc, in their 2013 paper titled The Effects of Unconventional and Conventional U.S. Monetary Policy on the Dollar, show that the dollar generally appreciates in response to rate-hikes, more so with increases greater than 25 bps and depreciates in response to rate-cuts of greater than 25 bps. However, the response of the dollar to rate-cuts of 25 bps is an exception to the pattern with the dollar appreciating on average.

Next, we look at some key financial variables for India. As the accompanying graphic shows, the rupee appreciated against the dollar after the December-2015 as well the December-2016 rate-hike. The rupee appreciated from 66.8 to the dollar on December 16, 2015—the date from which the December 2015 rate-hike was effective—to 66.4 to the dollar on December 18, 2015. Similarly, it appreciated from 67.8 to the dollar on December 15, 2016—the date from which the December 2016 rate-hike was effective—to 67.7 on December 19, 2016.

One possible reason for the appreciation could be RBI intervention in the foreign exchange market. Remember that RBI can sell dollars and other major currencies from its reserves to arrest the rupee’s depreciation beyond a limit. However, RBI data reveals that the central bank in fact made a net purchase of 1,987 million dollars in December 2015 and 586 million dollars in December 2016.

Not only did the rupee appreciate against dollar, capital inflows too did not slow down, as reflected in the Sensex. Both the times the rate-hikes were announced, the Sensex ended up at a higher level by the end of the month.

So, will the first rate hike by the Fed this year have an adverse impact on our economy? So far, the interest rate hike has not created much volatility in Indian markets. Not only has the exchange rate remained stable, capital inflows continue to remain robust. Given these initial results, the policy stance of RBI may continue to remain “neutral” in its forthcoming monetary policy.

The author is an Indian Economic Service officer, and is with the department of economic affairs, ministry of finance. Views are personal.