Investors often track the portfolios of seasoned market participants to understand where opportunities may be emerging. Their investment choices can offer cues on sectors and business models that are gaining traction before they become widely discussed. At the same time, these portfolios should be seen as indicators, not instructions.

For instance, in recent analyses such as Ashish Kacholia’s small-cap bets in niche segments and healthcare stocks in the Jhunjhunwala portfolio we highlighted how following such disclosures one can identify broader trends rather than just individual stock ideas.

In this context, we look at the portfolio of Dolly Khanna. Known for maintaining a low public profile, she has built a reputation for identifying lesser-known small-cap companies across sectors such as manufacturing, chemicals, and consumption. Her portfolio, which is said to be managed by her husband – Rajiv Khanna, is closely tracked because it often reflects early positioning in businesses that are not yet in the spotlight.

What stands out in the latest disclosures is a clear tilt. The focus appears to be on old-economy businesses and niche manufacturing segments. These are companies that are closely linked to the real economy. They are often cyclical in nature and tend to be under-analysed compared to high-growth or narrative-driven sectors.

There is a pattern in the selection. Most of the companies are from sectors like metals, refining and industrial materials. These are all part of the core economy. Their performance usually depends on demand cycles, commodity prices and overall economic activity.

The approach also looks balanced. Investments are spread across a few names and positions are not very large. In some cases, the holdings have been there for a few quarters, which suggests a steady approach rather than frequent buying and selling. For retail investors, such portfolios can give a sense of where attention is shifting in the market.

#1 Prakash Industries: Steel Expansion and the Bhaskarpara Coal

Prakash Industries is engaged in the business of manufacturing and sale of steel products and generation of power.

Dolly Khanna held 2.26% stake in Prakash Industries as of March 2026. This is her shareholding pattern in Prakash Industries for the past eight quarters.

Dolly Khanna Shareholding Pattern in Prakash Industries (June 2024 – March 2026)

| Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| 1.19% | 1.17% | 1.28% | 2.07% | 2.27% | 2.94% | 2.57% | 2.26% |

How the Bhaskarpara Coal Mine Integration Protects Margins

Prakash Industries continues to operate as an integrated steel player with backward linkage into raw materials. The business is closely tied to commodity cycles, particularly steel and coal. The company has been focusing on improving operational efficiency through captive resources and scale expansion.

For the December quarter (Q3 FY26), revenue from operations stood at Rs 798.6 crore, compared to Rs 925.9 crore in the same period last year. Net profit came in at Rs 86.9 crore, marginally higher than Rs 83.7 crore. The divergence between revenue and profit reflects cost management and operating leverage during the quarter.

The company’s strategy is anchored around integration. It has commenced coal extraction from its Bhaskarpara coal mine. This is a key development. The mine is expected to scale up to around 1 million tonnes annually in FY26. The availability of captive coal is likely to reduce input costs and improve margins in steel operations.

Scaling to 1 Million Tonnes: Preparing for the Infrastructure Upcycle

Steel production is also expected to cross 1 million tonnes, supported by improved raw material access and plant efficiencies. This positions the company to benefit from any upcycle in domestic steel demand, which is linked to infrastructure spending and industrial activity.

The broader industry remains cyclical. Steel prices have seen volatility due to global demand concerns and raw material fluctuations. However, companies with backward integration tend to be better placed during such phases. Prakash Industries’ focus on captive resources aligns with this trend.

The near-term outlook remains dependent on commodity cycles. Cost control and execution of the mining ramp-up will be key. Over the medium term, the integration strategy could support margin stability if demand conditions improve.

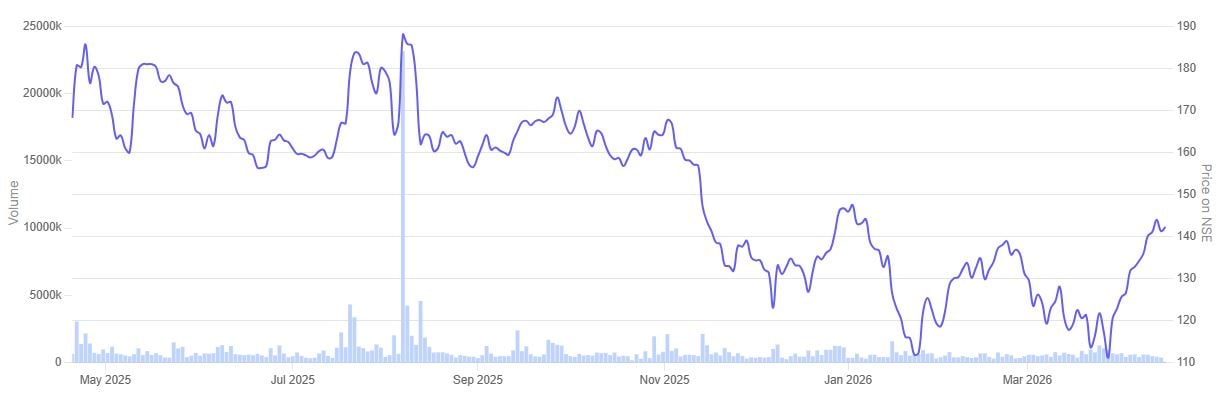

In the past year, the share price of Prakash Industries is down 15.4%.

Prakash Industries 1 Year Share Price Chart

#2 Chennai Petroleum Corporation: Leveraging 103% PAT growth and greenfield expansion

Chennai Petroleum Corporation is in the business of refining crude oil to produce & supply various petroleum products and manufacture and sale of lubricating oil additives.

Dolly Khanna held a 1.3% stake in Chennai Petroleum Corporation as of March 2026. Her shareholding stood at around 1.09% to 1.03% between June 2024 and March 2025. However, the holding was not disclosed in the next three quarters, which suggests it may have fallen below the 1% reporting threshold during that period.

Dolly Khanna Shareholding Pattern in Chennai Petroleum Corporation (June 2024 – March 2026)

| Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| 1.09% | 1.09% | 1.09% | 1.03% | – | – | – | 1.30% |

Chennai Petroleum Corporation (CPCL), a downstream oil refining PSU and part of the Indian Oil group, reported a strong performance in the December quarter, supported by improved refining margins and operational efficiency. Revenue from operations stood at Rs 20,134.8 crore in Q3 FY26, up around 27% year-on-year (YoY). Net profit rose 103.5% YoY to Rs 3,137.7 crore.

The improvement was aided by better gross refining margins and higher throughput. The company continues to operate in a cyclical refining environment, where earnings are closely linked to crude price movements and product spreads. Its integrated refining setup allows flexibility across fuels, lubes, and petrochemical feedstocks, which helps cushion volatility to an extent.

The Nagapattinam Greenfield Project: A 9 MMTPA Growth Engine

On the growth front, CPCL is moving ahead with capacity and integration plans. The company, along with Indian Oil, is setting up a 9 MMTPA greenfield refinery at Nagapattinam with integrated petrochemical capabilities. This project is expected to strengthen forward integration and improve value capture across the chain over the long term.

Decarbonizing Operations: Record RLNG Consumption and Renewable Shifts Placement

Operationally, CPCL is also focusing on efficiency and cleaner energy usage. RLNG consumption touched record levels, indicating a shift towards cleaner fuel mix. Water usage has been reduced through desalination and recycling initiatives. Renewable energy additions, including wind and solar capacity, are being scaled up to reduce the carbon footprint.

The company remains a typical old-economy, capital-intensive player. Earnings visibility depends on refining cycles rather than structural demand growth. Expansion into petrochemicals and retail integration could support medium-term stability. However, near-term performance will continue to be driven by margin cycles and crude price dynamics.

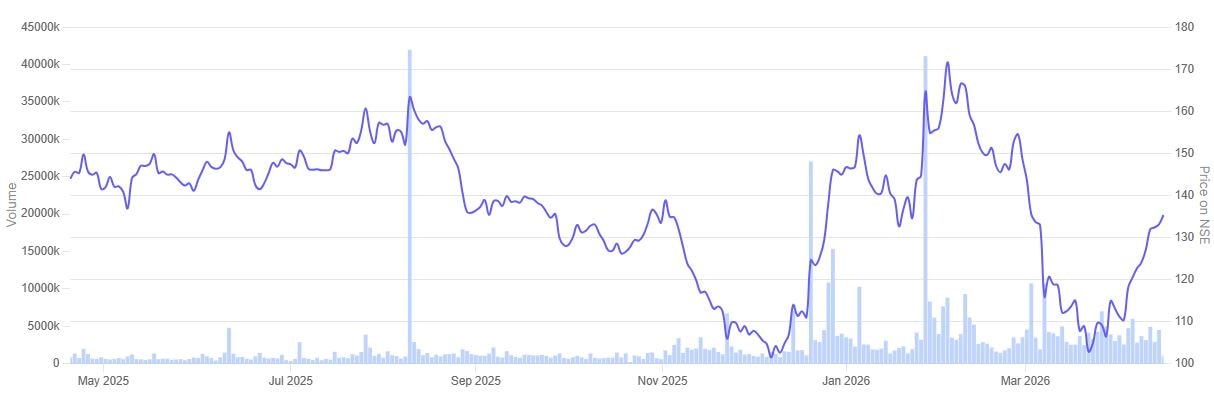

In the past year, the share price of Chennai Petroleum Corporation rallied 60.4%.

Chennai Petroleum Corporation 1 Year Share Price Chart

#3 Rain Industries: Carbon Leadership and the 2026 Ontario Graphite Milestone

Rain Industries (RAIN) is a leading vertically integrated producer of carbon, cement and advanced materials products. Headquartered in India, RAIN has manufacturing facilities in eight countries across three continents.

Dolly Khanna held 1.05% stake in Rain Industries as of March 2026. She previously did not hold any stake in the company or the stake may be below 1%.

Rain Industries, a global player in carbon products and advanced materials, continues to operate in a cyclical business environment linked to the aluminium and energy value chain. The company’s performance remains closely tied to movements in raw material prices and downstream demand from smelters and industrial users.

The Q3 Turnaround: Better Spread Management Drives Profitability

For the December quarter (Q3 FY26), consolidated revenue stood at Rs 4,301 crore reflecting a growth of around 17% YoY. Net profit came in at Rs 38 crore, marking a turnaround from a loss of Rs 134 crore a year ago. The improvement was driven by better spread management between raw material costs and finished product pricing, along with tighter cost control across operations.

The core carbon business continues to benefit from steady demand in the aluminium sector. Global smelter expansions, particularly in the US and Southeast Asia, are expected to support demand for calcined petroleum coke and coal tar pitch. At the same time, volatility in energy markets and feedstock availability remains a key factor influencing margins.

Beyond Carbon: Scaling Spherical Purified Graphite for the EV Battery Chain Placement

The company is also taking steps to diversify into higher-value segments. A recent development is its collaboration through Rain Carbon Canada with Green Graphite Technologies to advance production of coated spherical purified graphite, a key input for lithium-ion batteries.

The pilot phase has been completed successfully, and a demonstration plant in Ontario is expected to become operational in early 2026, with a longer-term plan to scale up to commercial production.

Rain’s global footprint across North America, Europe, and Asia provides operational flexibility. This helps the company manage supply chain disruptions and serve customers across regions. Management has indicated that its diversified sourcing and logistics capabilities offer some insulation against geopolitical and energy-related uncertainties.

The industry outlook remains mixed. While demand from aluminium and emerging battery materials offers support, input cost volatility and global uncertainties continue to weigh on near-term visibility. The company’s ability to balance its legacy carbon business with investments in new-age materials will be key to sustaining growth over the medium term.

In the past year, the share price of Rain Industries is down 6.9%.

Rain Industries Year Share Price Chart

Valuations

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | 5-Year Average EV/EBITDA | Industry Median | ROCE | ROE |

| 1 | Prakash Industries | 5.0 | 5.2 | 12.1 | 11.2% | 11.2% |

| 2 | Chennai Petroleum | 4.7 | 4.8 | 8.0 | 4.3% | 2.5% |

| 3 | Rain Industries | 5.6 | 5.6 | 6.8 | 8.3% | 0.6% |

Prakash Industries is relatively better on returns. Its return on capital employed (ROCE) and return on equity (ROE) are both at 11.2%. Rain Industries has a ROCE of 8.3%, but ROE is very low at 0.6%. Chennai Petroleum is lower on both, with ROCE at 4.3% and ROE at 2.5%.

Valuations are below industry levels for all three. Prakash Industries is at 5 times EV/EBITDA, slightly below its 5-year average of 5.2 times and far below the industry median of 12.1 times.

Chennai Petroleum is at 4.7 times, close to its 5-year average of 4.8 times, but still below the industry median of 8 times. Rain Industries is at 5.6 times, in line with its 5-year average and below the industry median of 6.8 times.

These businesses are cyclical. Returns usually depend on how the cycle moves. Prakash Industries looks better placed for now. Chennai Petroleum is cheaper but returns are weak. Rain Industries is somewhere in between.

Valuations are not high, but improvement in returns will be important to watch.

Conclusion

These are all cycle-driven businesses and that seems to be where Dolly Khanna’s recent portfolio is positioned. When the cycle is good, numbers improve. When it turns, returns fall quickly. That is already visible here. Valuations look low, but returns are still not strong across the board.

There is also a larger point. Seeing what known investors are buying can be useful. It gives ideas. But that is where it should stop. It is not a buy signal.

For retail investors, it is better to pause and check the basics. What does the business do? Where is the cycle right now? Only after that should a decision be made. Blindly following anyone, no matter how successful, rarely works in the long run.

It also helps to look at consistency. Are returns improving over time or still uneven? Is the business dependent on external factors like commodity prices? These questions matter more than just names in a portfolio.

In the end, conviction has to come from one’s own understanding. Markets tend to reward patience and clarity, not shortcuts.

You can track how these are progressing by adding stocks to your watchlist.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.