")

The global shipbuilding industry is currently experiencing significant growth, driven by naval modernization, decarbonization, and green shipping.

While the industry is concentrated in East Asia, with China, South Korea, and Japan dominating global output, India is working to capture a much larger share of this growing market.

Currently, India accounts for less than 1% of global shipbuilding production.

However, the sector is of profound strategic and economic importance to the country, as approximately 90% of India’s trade by volume moves through maritime routes.

Shipbuilding also provides massive economic benefits, boasting a high employment multiplier of 6.5 and an investment multiplier of approximately 1.8.

India also aims to become one of the top five shipbuilding nations by 2047.

A catalyst for the sector is the Indian Naval Indigenisation Plan 2015-2030, which aligns with the national “Make in India” initiative.

The Indian Navy aims to expand its fleet to approximately 234 ships and submarines. Currently, over 60 warships and submarines are under construction in Indian yards.

With 67% of the Navy’s procurement sourced domestically, Indian shipbuilders enjoy robust, multi-year order visibility.

Turning to exports, defence exports reached an all-time high of Rs 384.2 bn in FY26 and are expected to reach Rs 500 bn by FY29.

Against this backdrop, which shipbuilding stock, GRSE or Mazagon, is the better stock?

Let’s take a look…

Premier Defence Shipyards: A Comparison of MDL and GRSE

Garden Reach Shipbuilders & Engineers (GRSE) and Mazagon Dock Shipbuilders (MDL) operate with distinct but complementary business models within India’s defence shipbuilding sector.

They are both premier public-sector shipyards.

MDL executes high-complexity, technologically intensive naval platforms.

Strategic Focus: High-Tech Complexity vs High-Volume Scaling

MDL is the only Indian shipyard to construct both destroyers and conventional submarines (like the Scorpene class). It focuses on capital warships, stealth frigates, and submarines, which are long-gestation projects that drive margin accretion and offer stable, multi-year revenue visibility.

Consequently, MDL derives more than 95% of its revenue from the defence sector.

GRSE, on the other hand, builds frigate-sized platforms. Its strength lies in small and medium-sized vessels, such as corvettes, anti-submarine shallow-water craft, fast patrol vessels, and survey vessels.

GRSE operates on a volume-based growth model. It relies on a pipeline of patrol boats and auxiliary vessels for the Indian Navy and the Coast Guard. Its defence exposure is slightly lower but still dominant at 70-75%.

Infrastructure Philosophies: Heavy Capex vs Asset-Light Partnerships

MDL relies on a large-scale, brownfield and greenfield infrastructure expansion strategy.

The company is executing an ongoing capital expenditure (capex) program of around Rs 64 billion (bn) to develop the Nhava Greenfield Shipyard and utilize newly acquired Mumbai Port Authority land.

This massive infrastructure investment allows MDL to concurrently build 10 warships and 11 submarines, keeping all major critical construction in-house.

GRSE employs an “asset-light” capacity scaling strategy.

Instead of spending on infrastructure in isolation, GRSE relies on modular shipbuilding, outsourcing, and strategic partnerships.

To overcome the limitations of its physical capacity (such as dock size, which prevents it from bidding independently for the massive ‘Landing Platform Dock’), it utilizes the ‘Public-Private Partnership model.

It outsources partial construction to private shipyards and signs Memoranda of Understanding with yards such as Hindustan Shipyard and Swan Defence to leverage their infrastructure.

Revenue Diversification Beyond Traditional Shipbuilding

GRSE has aggressively diversified its business model beyond shipbuilding. It generates a meaningful 25-30% of its revenue from commercial and auxiliary markets.

The company operates specialized divisions that manufacture portable steel Bailey bridges, marine diesel engines (in collaboration with MTU, Germany), deck machinery, and even 30 mm Naval Surface Guns.

Furthermore, GRSE has entered the green and commercial shipbuilding market.

It delivered India’s largest zero-emission fully electric passenger ferry to the Government of West Bengal, securing follow-on orders for hybrid ferries.

MDL’s commercial exposure is lower.

Its primary non-defence diversification is in the oil sector, where it constructs highly complex marine and offshore structures, including wellhead platforms and jack-up rigs for clients such as ONGC.

MDL recently secured two major offshore contracts from ONGC worth Rs 46.76 bn and Rs 14.86 bn.

Global Ambitions and the Colombo Dockyard Acquisition

MDL acquired a majority stake in Colombo Dockyard (CDPLC) to strengthen its commercial shipbuilding footprint. CDPLC’s core operations are in shipbuilding and ship repair.

This acquisition marks MDL’s first international foray and is a cornerstone of its ambition to become a global shipyard. By integrating CDPLC, MDL intends to leverage the Sri Lankan yard’s strategic geographic location, proven technical capabilities, and strong regional presence.

This will position MDL as a key player in the South Asian maritime sector. This is a key part of MDL’s broader strategy to diversify its revenue streams and drive incremental growth.

The acquisition is expected to significantly expand MDL’s footprint in the commercial shipbuilding, ship repair, and refit markets

Both companies are actively pursuing the export market to transition from domestic reliance to global competitiveness.

Expanding the Export Playbook

GRSE has a strong historical foothold in exports. It is the first Indian shipyard to export a warship (an Offshore Patrol Vessel to Mauritius in 2014).

Its export strategy targets friendly foreign countries in SAARC, ASEAN, Africa, and Latin America.

GRSE frequently exports commercial vessels and dredgers to Bangladesh, fast patrol vessels to Seychelles, and portable bridges to Bhutan and Nepal. Recently, it has also expanded its presence in Europe by securing an order for eight multipurpose vessels from Germany.

MDL is revamping its global presence by leveraging its high-tech capabilities in weapon integration and complex platforms.

MDL has successfully broken into the European market, signing a US$ 85 million contract for six 7,500 DWT Multi-Purpose Hybrid Powered Vessels for Navi Merchants, Denmark.

Ship repair has emerged as a high-margin growth engine for India’s public-sector shipyards. This enables them to diversify their revenue streams beyond long-gestation shipbuilding projects.

Ship Repair: The New High-Margin Growth Engine

GRSE established its Ship Repair division as an independent business in FY22. The segment has witnessed exponential growth by capturing high-value refits. GRSE’s ship repair revenue surged from just Rs 0.2 bn in FY22 to Rs 1.1 bn in FY25.

This rapid growth was propelled by GRSE’s strategic move to take over three dry docks on long-term lease from the Syama Prasad Mookerjee Port in Kolkata.

To further enhance its capacity and workshare, GRSE has signed strategic Memoranda of Understanding with private firms, including SHM Ship care and Mercury Ship Repairs.

The dedicated vertical handles scheduled, unscheduled, and emergency repairs for the Indian Navy, Coast Guard, and commercial vessels.

GRSE also services fleets in Sri Lanka, the Maldives, Mauritius, and the Seychelles, including the guaranteed refit of the exported Fast Patrol Vessel’ SCG PS Zoroaster’.

MDL is now targeting the global ship repair and refit market to diversify its revenue. The acquisition of Sri Lanka’s Colombo Dockyard PLC (CDPLC) is specifically aimed at expanding its footprint in the regional ship repair and refit market.

The company has also entered the aviation Maintenance, Repair, and Overhaul segment by undertaking helicopter repair for the Nepalese Army.

What do the Numbers Reveal About Future Growth?

Is Mazagon Dock Entering Its Next Order Cycle?

MDL’s financial growth is slower than GRSE’s.

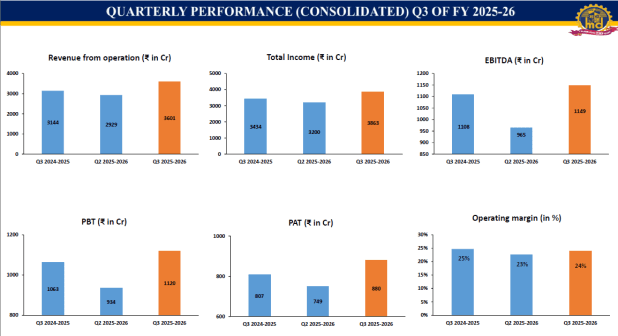

Revenue increased by 15% year-on-year to Rs 36 bn in Q3 FY26, driven by order book execution.

EBITDA grew 3.7% to Rs 11.5 bn, while margins fell 100 bps to 24%. Net profit jumped 9% to Rs 8.8 bn.

Source: Q3FY26 Investor Presentation

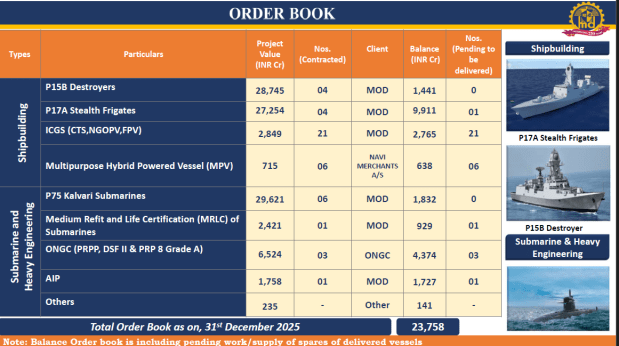

As of 31 December, 2025, MDL’s unexecuted order book stands at Rs 237.6 bn. This current order book is expected to be executed over the next two years, driving the company’s growth through FY26 and FY27.

Source: Q3FY26 Investor Presentation

While near-term growth is secured by the current backlog, MDL’s revenue growth from FY28 onwards will heavily depend on the timely placement of new mega-contracts.

The company has a near-term addressable opportunity pipeline exceeding Rs 3 trillion (tn) over the next decade.

Key upcoming mega-projects under negotiation or discussion include 3 units of P-75 Submarines (Rs 360 bn), 6 units of P-75 (I) (Rs 700 bn), 7 units of P-15 C (Rs 700 bn), and 4 units of P-17 (B) (Rs 500 bn).

MDL has signed a Memorandum of Understanding with Swan Defence to jointly bid for the upcoming Landing Platform Dock project, further expanding its market opportunities.

If MDL secures contracts from these programs, it would result in a 4–5 fold expansion of its order book, potentially increasing it to a range of Rs 1.1-1.3 tn by FY27.

To capitalise on this anticipated pipeline, MDL is pursuing a Rs 50 bn greenfield yard expansion in Tamil Nadu, alongside its ongoing Nhava yard development and Mumbai Port Authority land utilization.

Can GRSE Sustain Its High-Growth Momentum?

GRSE financials, on the other hand, have grown much faster.

Revenue increased by 49% year-on-year to Rs 19.2 bn in Q3 FY26, driven by order book execution.

Operating profit more than doubled (up 129%) to Rs 1.7 bn, while margins expanded by 300 bps to 9%. Net profit jumped by 74% to Rs 1.7 bn.

The management anticipates maintaining a strong growth rate of 25-30% in the current financial year. For the first time, GRSE’s order book has dipped below the Rs 200 bn mark, standing at Rs 184.8 bn as of 31 December 2025.

This provides revenue visibility for over 3 years, based on FY25 revenue of Rs 50.8 bn. This dip reflects an accelerated execution across its 42 platforms under construction.

The largest chunk of the current backlog is the P-17 Alpha frigates (Rs 82.4 bn). However, GRSE is targeting a fast replenishment of its order book.

The company is the declared L1 bidder for the Indian Navy’s Next-Generation Corvette (NGC) project, an order for 5 ships valued at approximately Rs 330 bn. GRSE expects to sign this contract soon, bringing the company’s order book to about Rs 500 bn by the end of FY26.

The Navy has accorded Acceptance of Necessity for 7 ships under the P-17 Bravo project, valued at about Rs 700 bn. GRSE is aggressively targeting an L2 position, which would yield a contract share of roughly Rs 300 bn.

GRSE is also targeting the Landing Platform Dock project (Rs 350 bn) and the Mine Counter Measure Vessel project (Rs 320 bn). Assuming successful contract wins, management aims to conclude FY27 with an order book exceeding Rs 700 bn.

To meet its execution targets, it has already expanded its concurrent shipbuilding capacity from 24 to 28 platforms and aims to reach 32 ships by the end of CY26 and 35 ships shortly thereafter.

GRSE is planning a state-of-the-art greenfield shipyard by 2028. It has identified two sites in Gujarat (Kandla and Bhavnagar) that will be developed over the next 3 to 4 years to handle the construction of up to 12 large-sized ships (such as 300-meter Very Large Gas Carriers).

To immediately bid for big platforms that exceed its current dock sizes, GRSE has signed an MoU with Hindustan Shipyard Limited to jointly bid for the LPD project. It also maintains an active MoU with Swan Defence to target large commercial vessels over 250 meters.

That said, the expansion will allow GRSE to eventually scale to a capacity of 40 ships per year by 2040 to absorb a structurally larger order pipeline.

GRSE is rapidly shifting from a traditional warship builder into a diversified, maritime engineering firm.

GRSE has secured orders for 13 hybrid ferries. It also received Approval in Principle for a 100-passenger Hydrogen Fuel Cell ferry and is developing Hybrid Tugs for the government’s Green Tug Transition Plan.

In the non-defence orders, management envisions a Rs 1 tn pipeline over the next few years, encompassing all small, medium, and large projects, and targets a minimum of 20% of order bookings from this opportunity.

The Valuation Check

In terms of valuation, MDL is trading at a Price-to-Earnings (PE) multiple of 38, which is on par with GRSE (37.5).

Both stocks are currently quoting at a modest premium to their historical median. GRSE’s 5-year median PE stands at 32.1, while Mazagon Dock’s historical median is 29.5.

Bottom line

Both GRSE and Mazagon Dock operate in a structurally strong sector backed by rising indigenisation, defence spending, and export opportunities.

While GRSE is currently witnessing faster execution-led growth and diversification, MDL benefits from its presence in high-complexity platforms with long-term strategic relevance.

At current valuations, both stocks are trading above their historical averages. This leaves limited room for error. Future performance could be driven by order inflows and subsequent financial growth.

On the other hand, given that shipbuilding is high gestation period business, execution miss, margin compression and financials slowdown are key risks to watch.

This is precisely why it is crucial to observe how the order flow progresses. Rather than relying solely on market chatter, investors should carefully analyze the company’s fundamentals, including its financial performance, corporate governance practices, and growth strategies.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary