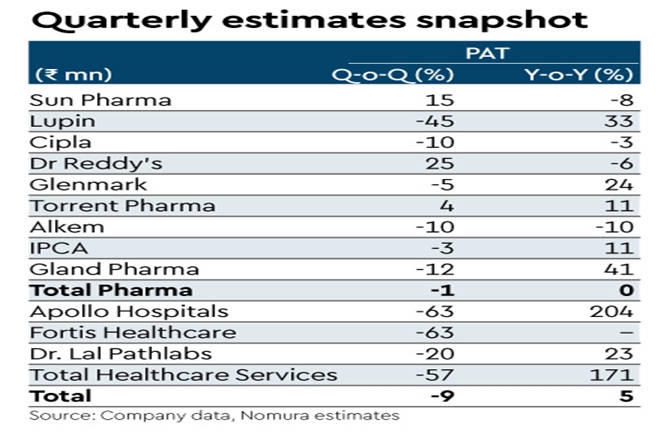

For our coverage universe, we forecast Q2 revenue/Ebitda/PAT growth of 10%/6%/5% y-o-y. Sequentially, we expect a slowdown as COVID-19-related demand receded during the quarter. We expect our coverage universe to record a decline of 3%/9%/9% in revenue/ Ebitda/PAT on a q-o-q basis. The key trends that we expect during the quarter are as follows:

We expect strong double-digit growth in domestic formulation. The y-o-y growth is supported by a relatively weak base last year. Our analysis suggests that sales of drugs positively impacted by COVD-19-related demand declined 22% q-o-q, but are still at an elevated level compared to the past trend. The demand for non-COVID-19 products has largely recovered to the level seen in the past. Within chronic therapies, we see a recovery in cardiology and neuro/CNS but diabetes has been a laggard. The y-o-y growth is likely to be particularly strong for SUNP, DRRD, IPCA, and ALKEM, in our view.

Our interaction with most companies suggests that the pricing environment in US generics remains challenging. However, there seems to be some stability after the lower adjustment in prices in H1FY2021, following a relatively benign 2020. Trx volumes in segments impacted by COVID-19 are gradually gaining traction. We expect DRRD to report an improvement in US sales q-q on the back of product-specific opportunities. SUNP should see a continued traction in specialty (except Absorica), in our view. Stable currencies and improving demand post easing of COVID-19 curbs should drive growth in most other markets y-o-y and q-o-q, in our view.

We expect a slowdown in diagnostics q-o-q, with a substantial decline in COVID-19 testing demand and lower RT-PCR pricing. We expect hospital revenues to record a drop q-o-q with lower COVID-19 occupancy and average revenue per occupied bed (ARPOB). However, y-o-y growth remains strong given a weak base.

The sector faces some cost pressure for raw materials and higher freight cost. Overhead expenses are expected to rise but are likely to remain below normal levels, in our view. We think travel and sales/promotion expenses are yet to normalise for companies.

Result plays

We are positive on DRRD and SUNP. After a relatively weak Q1FY22, we expect DRRD to report an improvement in growth and Ebitda margin. SUNP reported a strong Q1FY22, and we expect the outlook on specialty and India formulation to remain strong post Q2FY22 results. We also expect steady quarterly results from IPCA and TRP. The services segment benefited from COVID-19-related demand and it is likely to subside materially in Q2FY22F, which could lead to a downward revision of earnings. We are most cautious on DLPL given its relatively rich valuations. We believe its growth and Ebitda margin can surprise on the downside with a fall in COVID-19-related revenues.