In many a sense, exporters have an easier time of FX risk management as compared to companies with imports because the market structure is skewed in their favour—with rupee interest rates higher than those in most invoicing currencies, there is a nice forward premium available for selling forward and eliminating (or reducing) risk. That many exporters choose not to sell, or sell inadequately—always waiting for the Godot of a rupee collapse—is another matter.

For importers, the situation is reversed—they have to pay the premium to eliminate risk. And, of course, nobody likes to pay. And while there is always the threat of a sharp rupee decline at any point, history shows that on average the rupee falls by less than the forward premium, so, there is an intuitive reason for staying unhedged.

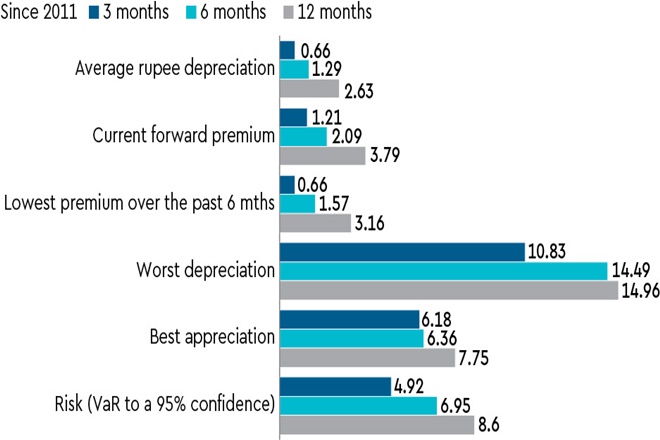

Of course, staying unhedged exposes the company to risk and, to my reckoning, few companies build any estimate of this risk into their business plans. The accompanying graphic shows the risk carried by unhedged import exposures to different tenors.

The numbers indicate that while the premiums are, in general, higher than the average depreciation, they are substantially lower than the worst depreciation (to tenor) that we have seen over the past 10 years, and quite a bit lower than even the risk on an open exposure. Value at Risk (VaR) to a 95% confidence is a well-established risk measure; it is a number that tells you that there is a 5% probability that an unhedged exposure will end up costing more than the VaR figure. Thus, the analysis shows that there is a 5% chance that an unhedged 6-month exposure would lose more than 6.95.

Thus, in developing its business plan, companies should use [spot + VaR] to price its imports to different tenors; in my experience, few companies do that. An alternate approach would be to set a risk limit above the forward rate on the date of formation of the business plan AND have a disciplined risk management process in place to use this risk limit as a stop loss. Contrariwise, we have found that most companies use ad hoc processes for pricing their imports in their business plans.

Most importantly, few companies link their risk management process to their budgeted FX rates for imports. Indeed, operationally, too many companies identify their import risk only on the basis of confirmed purchases – which are generally not much further out than 3-4 months. This results in 8-9 months of exposures being unmonitored at any point in time, which, as we see from the table represents a huge risk of 7-8 rupees, or around 10%! It’s hard to imagine any board being comfortable with that, and audit committees need to review their hedge policies to ensure that the risk being carried is within the board’s comfort level.

Of course, identifying exposures as risk beyond 3 months doesn’t mean simply hedging them out. Given the reality that on average the rupee falls less than the premiums provides an opportunity to save at least some part of the hedging cost while ensuring that the risk is contained.

For exposures identified out to 6 months, we have developed a sliding stop loss model that has saved around 1% a year in hedging costs on average. To be sure, the results are volatile and, as often as 60% of the time, the model loses money as compared to hedging on Day 1; however, its worst case loss is an increase in cost of 4% pa which is way lower than its best gain, which was nearly 15% pa. Like any stop loss model, the goal is to limit losses and enable the exposure to ride rupee strength for maximum gains.

For 12 month exposures, the model also works but results are a bit weaker—average gain is just 0.65% pa; negative performance 55% of the time; worst case cost increase 2.7% pa; best savings 7.5% pa. However, given that risk on a 12-month exposure is nowhere near twice the risk on a 6-month exposure, it may make sense to stay unhedged for 6 months with a, say, 3% pa stop loss and shift to the trailing model after that.

For shorter tenor exposures, our regular MHP-I (Mecklai Hedge Program – Imports) provides excellent value, racking up cost savings of 1.77% pa since, again, 2017; importantly, at this tenor the program is negative just 25% of the time. Given the continuing huge volatility of the rupee, these are, to my mind, excellent savings.

The author is CEO, Mecklai Financial