")

Mukul Agrawal is one of the most highly followed and looked upon super investors of India, or as we like to call him, a Warren Buffett of India. He is not someone very fond of being on camera and prefers his results do the talking.

Currently holding 72 stocks in his portfolio worth over Rs 6,600 cr, Agrawal is one of the most followed investors in India.

While I was looking for stocks with solid dividend yields and a strong grip on capital efficiency, 2 stocks came in the results and one of them has been a part of Agrawal’s portfolio since about 8 years. Let us look at that stock along with another one that fulfils the same criteria but still hasn’t grabbed the attention of any super investor like Agrawal.

MPS Ltd: High Yield vs. Structural Reset

Incorporated in 1970, MPS Ltd is a B2B learning and platform solutions company powering education, and research for corporates.

With a market cap of Rs 2,554 cr, the company has 700+ customers, with 33% revenues being generated from top 5 customers and 46% from top 10. In the last 10 years, the company has acquired 8 companies.

Mukul Agrawal has held a stake in the company since the exchange filings for the quarter ending September 2018. Currently, he holds a 4.5% stake in the company worth about Rs 114 cr.

The company has a current ROCE (Return on Capital Employed) of 41%, which is almost double than the current industry median of 22%. In simple words, MPS generates a profit of Rs 41 on every Rs 100 it uses as capital for business, while its peers average about Rs 22.

Add to this that the company is has a debt-to-equity ratio of just 0.02, which which means the company is virtually debt free. So, no big interest payments eating into profits.

And the company isn’t keeping these wins to themselves but also sharing them with its stake holders by means of Dividends. The current dividend yield of the company is 5.6% while the industry median is a flat 0%, and it maintains a dividend payout ratio of 78%.

Let us look at the core financials of the company to see if it has what it takes to sustain this performance.

The sales of the company grew from Rs 332 cr to Rs 727 cr between FY20 and FY25, which is a compound growth of 17%. At the end of Q3FY26 (quarter ending December 2025), the sales recorded by the company were Rs 562 cr.

The EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) went from Rs 79 cr in FY20 to Rs 211 cr in FY25, which is a compound growth of 22%. At the end of Q3FY26, the EBITDA logged is Rs 168 cr already.

The net profits climbed from Rs 60 cr in FY20 to Rs 149 cr in FY25, which is a compound growth of 22%. And by the end of Q3FY26, the profits logged were Rs 126 cr.

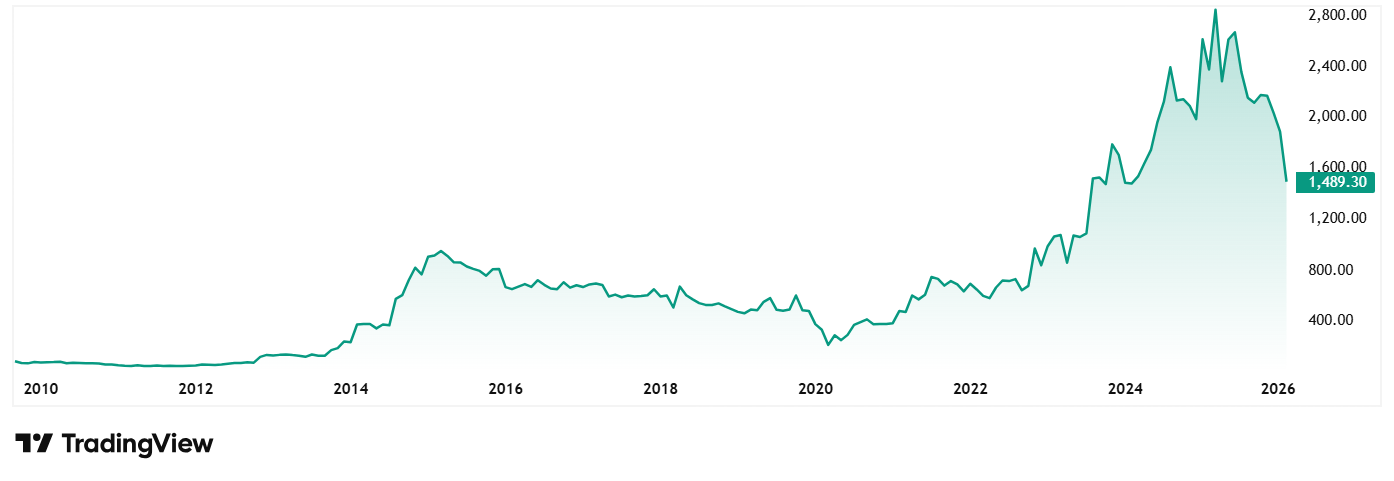

The share price of MPS Ltd was around Rs 475 in February 2021 and as of closing on 13th February 2026 it was Rs 1,493 which is a jump of 214% in 5 years. Rs 1 lakh invested in the company 5 years ago would have been over Rs 3.2 lakhs today.

Regarding the valuations, the stock is trading at a PE of a 16x which is less than the current industry median of 21x. The 10-Year median PE for MPS Ltd is 17x and the industry median for the same period is 27x.

The stock is currently trading at a 52% discount from its all-time high, having suffered a sharp 32% correction in just the last six months.

This drop is fuelled by multiple factors, mainly 13% YoY drop in Q3 net profits, margin compression in the Corporate Learning segment, and the recent resignation of a non-executive director, suggesting that while the balance sheet is strong and secure, the business is navigating a challenging structural reset.

Alldigi Tech Ltd – A Global Outsourcing Leader with a 7% Yield

Incorporated in 1998, Alldigi Tech is a global leader in outsourcing solutions offering future-ready, resilient business transformation services to industry heavy-weights, Fortune 100 companies, and growth-focused organizations.

With a market cap of Rs 1,265 cr the company provides services in areas like data verification, processing of orders received through telephone calls, telemarketing, monitoring quality of calls of other call centres, customer services and HR and payroll processing.

The company has a current ROCE of 32%, which is higher than the current industry median of 13%. Add to this that the company has a current dividend yield of 7.2%, while the industry median is once again a flat 0%.

Looking at the financials of the company, the sales of the company jumped from Rs 294 cr in FY20 to Rs 546 in FY25, recording is a compound growth of 13%. At the end of Q3FY26, the sales recorded by the company were Rs 444 cr.

The EBITDA jumped from Rs 75 cr in FY20 to Rs 130 cr in FY25, which is a compound growth of 12%. And Q3FY26, the EBITDA logged is Rs 119 cr.

The net profits logged in a sustained growth pattern and grew from Rs 45 cr in FY20 to Rs 83 cr in FY25, which is a compound growth of 10%. And at the end of Q3FY26, the profits recorded by the company were Rs 54 cr.

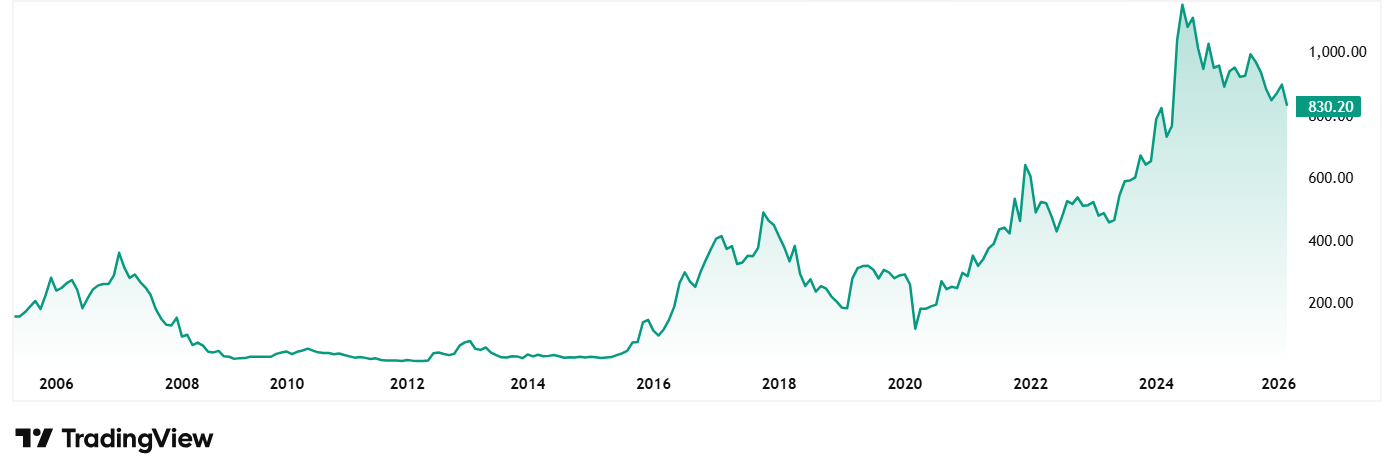

The share price of Alldigi Tech Ltd was around Rs 350 in February 2021 and as of closing on 13th February 2026 it was Rs 830, which is a 137% jump.

At the current price of Rs 830, the stock is trading at a discount of 34% from its all-time high of Rs 1,252.

The company’s stock is trading at a PE of 17x, and the current industry median is 26x. The 10-year median PE for the company is 15x while the industry for the same period 16x.

In December 2025, the Office of Commissioner of GST issued a demand for Rs 9.31 cr plus an equal penalty of Rs 9.30 cr for the period April 2018 to March 2023. The demand relates to alleged irregularities in Input Tax Credit (ITC) and cross-charge services between the head office and branches. While the company intends to appeal, this represents nearly 22% of their entire FY25 net profit, creating a substantial contingent liability.

While the international segments are growing for the company, international revenues now account for 67% of total revenue. While this provides better margins, it also increases vulnerability to global economic slowdowns and currency fluctuations.

Can Dividends Protect Against Small-Cap Volatility?

Both Alldigi Tech and MPS Ltd have a unique combination of aggressive dividend yields and high capital efficiency, which could function as a protective buffer in the erratic small-cap market. But the market’s recent punishment of their stock prices, which are down more than 30%, shows that dividends are insufficient to cover up the underlying concerns about regulatory friction and margin sustainability.

Rather than concentrating on short-term price action, super investors like Mukul Agrawal in MPS appear to have a long-term belief in the company’s core strengths. However, the instability of the small-cap segment is highlighted by the recent resignation of key personnel, the compression of corporate learning margins for MPS, and the significant GST contingency for Alldigi.

These structural tests, and not the statistical anomalies, will establish whether these companies can continue to be dividend kings or whether they are about to enter a protracted period of consolidation. It would be a good idea to add these stocks to a watchlist and follow them closely.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.