Ashish Dhawan, a very well-known and highly followed super investor of India just made two big moves in his portfolio. Dhawan, known for his fondness for fast-growing sectors with strong outcomes, just bet more on an infrastructure company he already held, while moving out of a famous bank.

Dhawan now holds only 12 stocks worth Rs 2,045 cr in his portfolio. And he has maintained this portfolio with the help of his strategic approach put together with value investing. So, when he makes moves, the market takes notes.

Let us look at the two stocks in question to try and find a reason for these moves.

Bluspring Enterprises: The infrastructure turnaround play

Incorporated in 2025 after a demerger from Quess Corp, Bluspring Enterprises Ltd is in the business as an infrastructure services company.

With a market cap of Rs 957 cr, the company is an integrated facility management service provider offering end-to-end solutions like Soft Services, Hard Services / Engineering Services, Production Support Services, Hygiene Services, Technology Enabled Services.

Dhawan, who had held a 4.1% stake as of June 2025, has since added another chunk of shares to his holding. As per the quarter ending December 2025, he now holds 5% of the company worth Rs 48 cr.

Let us look at the financials to see if we can find out why he decided to raise the stakes.

Screener.com only has consolidated data for the company from FY24 probably due to the demerger, which is what we will be analysing today.

The sales of the company have grown at a rate of 30% from Rs 2,682 cr in FY24 to 3,484 cr in FY25. And for H1FY26, the sales have been Rs 1,655 cr.

EBITDA jumped from Rs 78 cr to Rs 83 cr in the same period, logging a growth of just 6.4%. For H1FY26, the EBITDA recorded is close to Rs 30 cr

When it comes to net profits, the company was reporting losses since the quarter ending December 2024. However, the September 2025 filing reported profits of Rs 3.5 cr. This looks like the company is on the way to a turnaround, which Dhawan is planning to cash in on.

The share price of Bluspring Enterprises Ltd after demerger was around Rs 85 in June 2025 and as on 22nd January 2026 was Rs 65, which is a 24% drop in about 7 months.

The company’s stock is trading at a negative PE due to the losses recently, and the industry median is currently 21x.

Following the successful demerger and listing in June 2025, Bluspring is planning for big changes.

With a diversified portfolio across Facility and Food Service, Telecom and Industrial Services, Security Services etc the company is well-positioned to capitalize on a Rs 170,000 cr market opportunity with a projected 13% CAGR over the next three years.

Ashish Dhawan buying more of Bluspring could be a classic “value-unlocking” demerger thesis, where a specialized business is finally allowed to operate without the weight of a larger parent entity.

While the stock has seen a steep post-listing correction, a seasoned investor like Dhawan often views such volatility as an entry point into a market leader at a discounted valuation.

IDFC First Bank: When valuations outpace fundamentals

IDFC First Bank Ltd is engaged in the business of Banking Services. IDFC FIRST Bank was founded by the merger of erstwhile IDFC Bank and erstwhile Capital First on December 18, 2018

With a market cap of Rs 71,791 cr, the bank is India’s largest FASTag issuer with 17.8 million live tags and a 37% market share.

Ashish Dawan had a 1.2% per the December 2024 exchange filings, which went to 1.35 the very next quarter. His initial stake was in IDFC Limited, which was subsequently converted on its merger with IDFC First Bank. However, as per the recent exchange filings for the quarter ending December 2025, this holding has dropped below 1% signalling a complete or partial exit.

For an investor like Dhawan to exit a bank that has been growing steadily has raised some good questions. However, the key to understanding this exit lies in the recent quarterly figures. Let us look at the core financials.

The bank’s revenues grew at a compounded rate of 18% from Rs 16,240 cr in FY20 to Rs 36,502 cr in FY25. For H1FY26, the revenues logged were Rs 19,580 cr.

According to the company’s latest investor presentation in October 2025, the bank’s loan book grew by 20% on a YoY basis to Rs 267,000 cr.

The NII (Net Interest Income) grew from Rs 16,451 cr in FY24 to Rs 19,292 cr in FY25, which is a growth of 17%. The NIM (Net Interest Margin) however witnessed a small drop from 6.36% of FY24 to 6.09% in FY25. The bank noted that this was due to decline in the micro-finance business.

The net profits of the bank also saw a 50% decline in FY25. This was on account of write off largely related to the micro finance book.

| Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Profits/Rs Cr | -2,843 | 483 | 132 | 2,485 | 2,942 | 1,490 |

And for H1FY26, the net profits logged by the bank were Rs 801 cr, which is lower than the figure of Rs 855 cr for the same two quarters last financial year.

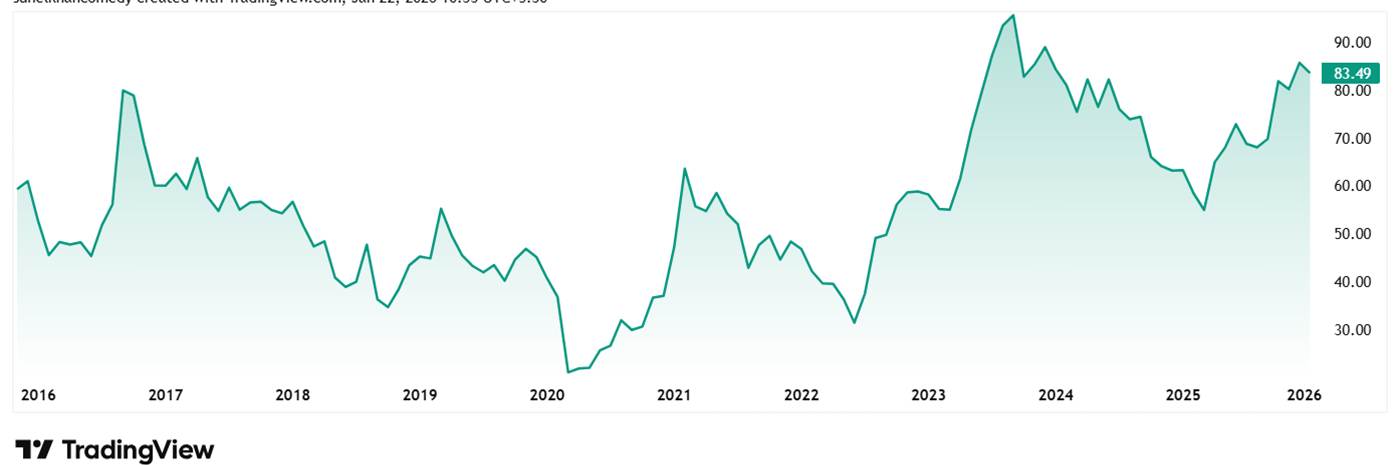

The share price of IDFC First Bank Ltd was around Rs 50 in January 2021 and as on 22nd January 2026 it was Rs 84, which is a 68% jump in 5 years.

The bank’s share is trading at a PE of 50x, which is much higher than the current industry median is 15x. The 10-year median PE for the bank is 20x while the industry median for the same period is around 16x.

Ashish Dhawan’s exit from IDFC First Bank is likely a strategic move to book profits after the stock’s successful re-rating from its pandemic lows.

With the bank’s valuation now trading at a premium of 50x, relative to larger peers, and recent earnings showing margin pressure from the microfinance segment, the turnaround premium appears fully priced in.

For a value investor like Dhawan, this transition from a high-growth recovery story to a mature, margin-focused consolidation phase likely signalled the right moment to move capital into more undervalued opportunities.

Portfolio hygiene or sector rotation?

Ashish Dhawan’s recent changes serve as a reminder for portfolio hygiene. By trimming IDFC First Bank, he isn’t necessarily betting against the bank’s future but rather acknowledging that the market’s expectations may have finally outpaced reality.

Meanwhile, his conviction in Bluspring suggests that under the recent losses lies a possible scalable infrastructure machine waiting to go big. In a market where many are chasing momentum, Dhawan’s shift back toward deep-value demergers raises some questions. Has the easy money in banking been made, and is the next decade of alpha hidden in Infrastructure?

Only time will tell. For now, the only way to see how it all works out is to add these stocks to a watchlist and keep a vigilant eye on them.

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.