SBI Card, India’s second-largest credit card issuer, is expected to experience a 23% CAGR in card spends from FY2023-26 by taking advantage of its large customer base and co-branded card tie-ups. Net interest margins (NIMs), are predicted to hit their lowest point in the first half of FY2024 but should then improve over the next few years as the mix of credit card balances that are carried over from m-o-m increases and interest rates stabilise. This should lead to healthy profit growth and a ROE of at least 23% from FY2024-26. The recent underperformance of SBI Cards compared to the NIFTY, may be due to concerns about NIMs. However, the Jefferies recommends buying SBI Cards shares with a PT of Rs 900.

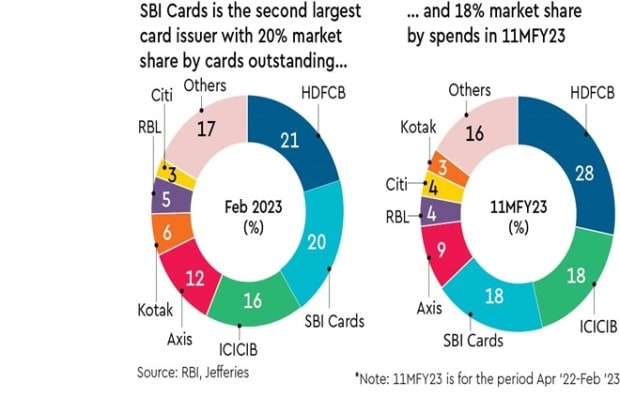

Penetration into SBI base, co-branded card tie-ups to drive market share gain: Rising digital payments and low card penetration (5% of population > 15 yrs) should support 21% CAGR in card spends over FY23-26E. The threat from fintechs has eased. SBI Card should gain share in card spends, as scope to increase penetration within SBI’s large customer base is large; credit card to debit cards ratio (ex PMJDY) is 14% below peer average of 29% and penetration within SBI’s addressable customer pool is only 6%. Co-branded card tie ups are c.2x peers. Its open market channel is larger than most peers’. We forecast SBI Card card spends to grow at 23% CAGR over FY23-26e.

NIMs to bottom in 1HFY24 and could inch higher over FY24-26e: SBI Card has faced NIM pressure due to fall in mix of higher yielding revolvers from 35%+ pre Covid to 24% and rise in funding costs. Increase in sourcing of customers with higher propensity to revolve (eg. self-employed, tier 2-3 cities) can lift revolver mix slowly by 150bps over FY24-26e, though it should still stay well below pre-Covid levels. Interestingly, industry card receivables to trailing 3M spends inched up in Jan. The recent push to convert transaction spends to EMI can lift margins. Risks are that it may cannibalise some revolver spends. A 1% change in EMI mix changes EPS by 1.5%. Funding costs should stabilise as rates peak. 65% of its liabilities are linked to repo/T bill rates, which reprice faster.

Also read: Online GST registration 2023: Here’s how you can easily register your MSME unit step-by-step

SBI Card is expected to experience strong financial growth between FY23 and FY26. The company’s profit is projected to grow at a CAGR of 23% during this period. The top line, — revenue, is expected to grow at a CAGR of 22% over the same period. This growth will be driven by a 24% CAGR in NII and a 21% CAGR in fee income.

Tighter norms for processing over limit transactions by RBI has hit over limit fees. With asset quality pressures easing, stage 3 assets and credit costs should be stable. Possible caps on MDR and revolver yields, by RBI are key risks. Threat from potential new entrants like BAF and higher spend share gain by UPI are the key risks.