By Amarendu Nandy & Jasmeet Singh Bindra

The pandemic has triggered a debate as to whether the global value chains (GVCs), which are production networks that seek to exploit gains from hyper-specialisation across countries, may lead to increased fragility of economies actively participating in them. As the experiences during the ongoing pandemic suggest, major demand- and supply-side shocks to value chains, and lack of redundancy planning in such networks, have posed considerable challenges to just-in-time manufacturing activities, arguably accentuating the economic vulnerabilities for countries, including India.

Over the last decade, the system of international production has been grappling with challenges arising from Industry 4.0; growing economic nationalism, and sustainability concerns. The ongoing pandemic has fuelled calls for further de-globalisation of such production networks to reduce industry- and economy-level vulnerabilities.

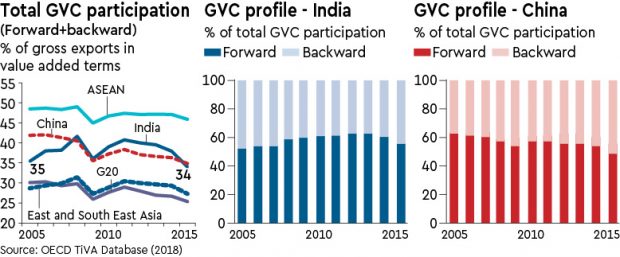

The accompanying graphic shows the overall GVC intensity across selected economies and groupings in terms of percentage share of the total value added (backward plus forward) in gross exports. It is clear that between 2005 and 2015, there has been a steady decline in GVC intensity across all major economies. For India, GVC participation peaked at 41.6% in 2008, but has dropped ever since, hitting a low of around 34% in 2015.

The stagnation of GVC trade since the global financial crisis, and the unfavourable impact of the ongoing pandemic on GVCs notwithstanding, there are substantial merits of widening and deepening link to GVCs, particularly for a developing country like India.

First, as the World Bank’s World Development Report 2020 (WDR 20) suggests, contingent upon deeper reforms in developing countries and policy continuity in industrial economies, GVCs can help reduce poverty, and continue to augment growth and employment. Cross-country estimates suggest that a 1% increase in GVC participation can boost per-capita income by more than 1%, particularly when countries engage in limited and advanced manufacturing. The growth is much higher than the 0.2% income gain from standard trade.

Second, GVC participation can precipitate significant firm-level productivity improvements. WDR 20 suggests that GVC firms engaged in manufacturing activities show higher labour productivity than one-way traders or non-traders, after controlling for firm-level capital intensity. In particular, firms that engage in both import and export are 76% more productive than non-trading firms, compared with a 42% difference for export-only firms and a 20% difference for import-only firms.

Third, backward participation in GVCs can be particularly beneficial for economies—a 10% increase in the level of GVC participation could increase average productivity by close to 1.6%. As the accompanying graphic shows, while China has seen a rise in its forward GVC participation and a corresponding drop in the backward participation, the trend has been just the opposite for India. India’s share of foreign value-added content in total GVC trade has steadily increased from 53% in 2005 to 61% in 2014. If India can seize FDI looking to relocate from China, and create conditions for firms to leverage the labour-cost arbitrage opportunities, it can capture much of the value addition at the midstream stages. This will, however, necessitate deeper reforms in labour markets, trade infrastructure, and improvements in the overall business environment. Policies directed towards facilitating vertical GVC linkages between domestic SMEs and larger foreign and domestic firms can go a long way towards strengthening India’s relative position in GVC trade.

Fourth, the OECD METRO Model shows that localised regimes (less reliant on foreign suppliers) are more vulnerable to shocks, and result in a significantly lower level of economic activity and fall in national incomes as compared to the interconnected regimes. While interconnected regimes build resilience, stability and flexibility in the production networks, localised regime offers fewer channels for adjustment to shocks. Estimates for India suggest that a shift towards a localised regime can decrease real GDP by 1.1%, and reduce import and export demand by 11.4% and 14.8%, respectively. Recent policy pronouncement for an Atmanirbhar Bharat may be antithetical to the spirit of efficiency-seeking economic interdependence typified by GVCs in the long-term.

In the aftermath of the pandemic, regional value chains (RVCs) are expected to gain momentum to strike a balance between localisation and globalisation. However, if the recent RCEP experience is any indication, facilitating RVCs is difficult and requires intense regional coordination, geopolitical stability and conducive systemic conditions. If India intends to strike a balance between managing vulnerabilities in GVCs (similar to those arising from the pandemic), and building resilience, it may need to reassess its regionalisation strategy to take advantage of the accelerated momentum towards RVCs.

That said, long-term gains from globally connected value chains can far outweigh the benefits from RVCs. Not to forget, much of the recovery post-GFC was led by GVC-intensive exports. RVCs could be stepping stone and enabler for more global participation.

Instead of a piecemeal approach, India needs to adopt a holistic perspective focused on ‘whole of the supply chain’, by driving strategic changes in its investment-development paradigm, and through greater integration into the GVCs.

Nandy is Assistant Professor & Bindra is a gold medallist, PGP (2018-20), IIM Ranchi. Views are personal