reveals that Kerala is trying to achieve a revenue-led fiscal consolidation.")

Recent reports from RBI and Niti Aayog highlight the remarkable achievements of Kerala in education, health and nutrition; and the significant role of the state in ensuring such positive human development outcome. This makes Kerala different from rest of the country.

Of late, the state is facing fiscal problems in maintaining such levels of high human development and capital formation. The fiscal stress of the state is getting attention in Indian public finances, at the subnational level, in the backdrop of “fiscal rules” and Fiscal Responsibility and Budget Management (FRBM).

An analysis of the reports of Kerala State Public Expenditure Committee (chaired by Pinaki Chakraborty) reveals that Kerala is trying to achieve a revenue-led fiscal consolidation. However, the volatility in tax transfers and grants and the difficulties in Additional Resource Mobilisation (ARM) with respect to own revenue are matters of serious concern. There is lack of clarity in the apportionment of IGST, the portion given to the states is bound to affect state finances. The tax buoyancy is also affected due to the cyclicality of returns, and ease of filing GST returns.

There are also concerns about the phasing out of revenue deficit grants by the Finance Commission (FC). Clarity would emerge, by end-November, when 15th FC releases its report. The report shall also provide clarity on the issue of the new intergovernmental fiscal transfer mechanism since the phasing out of plan and non-plan distinction of grants.

What can be a flexible framework for borrowing requirements to finance the human development and capital infrastructure investment, within the FRBM Act? Oliver Blanchard, in his recent Presidential Address in American Economic Association, highlighted that as long as the real rate of interest (r) is less than real growth of economy (g), public debt is not bad. However, Indian states have been under pressure to adjust to the fiscal rules, with imposition of a fiscal deficit-GSDP ratio of 3% and phasing out of revenue deficit. Fiscal discipline is viewed as a pre-requisite for greater economic growth. Different states have responded in different ways to the public debt threshold. For instance, Telangana has preferred to elongate the maturity structure of public debt to overcome the stringent borrowing paradigm. Kerala has initiated trading of rupee-denominated “masala bonds” to finance capital infrastructure investment. Kerala, is the first state to go to international bond market for trading in rupee-denominated masala bonds.

“Off-budget liability” is becoming a significant element of state finances. The “golden fiscal rule” of zero revenue deficit is a significant challenge. The fiscal space for meeting revenue expenditure, especially the salary and pensions and interest payments, out of own revenue receipts is shrinking. The extra borrowing powers of the state is limited by central government. The Fourteenth Finance Commission did carve out a strategy for the states based on certain criteria to make them eligible for extra borrowing powers. These four criteria include zero revenue deficit, fiscal deficit –GSDP ratio at 3%, public debt-GSDP ratio at 25% and interest payments-revenue receipts ratio at 10%. Kerala has not been able to clear all the criteria for extra-borrowing powers permitted by the Fourteenth Finance Commission. The point to be noted here is that the States which have cleared all four criteria and are eligible for extra-borrowing requirements have also not availed that power, and prefer to get “over-adjusted” to the fiscal rules at the cost of capital expenditure.

The revenue receipts to GSDP in Kerala was around 12% in 2016-17. The tax revenue to GSDP was 9.23% in 2016-17. The revenue expenditure to GSDP ratio was 14.65%. The social service spending to GSDP ratio was 5%. The capital expenditure to GSDP ratio was only around 1%. Over the years, capital expenditure has declined from 1.12% of GSDP in 2012-13 to 0.83% in 2014-15, one can see a marginal increase to 1.63% in 2016-17. The state recently initiated rupee-denominated “masala bonds” for capital investment through public sector entity. These bonds are backed by state guarantee.

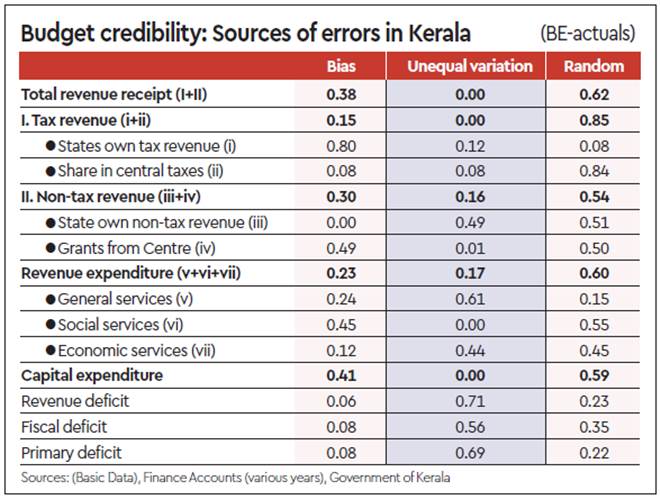

Kerala has fiscal deficit to GSDP ratio higher than the rule-based numerical threshold, which clearly shows the fiscal stress to achieve fiscal consolidation through revenue buoyancy and not through expenditure compression. Therefore, it is crucial to analyse the budget credibility of the State, disaggregating various macro-fiscal variables (see table).

Budget credibility, captured in the magnitude and sources of the fiscal forecasting errors, is found relatively challenging for tax revenue. The sources of forecasting errors can decomposed into bias, unequal variation and random components using Theils U methodology. These three components add up to one.

At the aggregate level, in case of total revenue receipt (both tax revenue and non-tax revenue), revenue expenditure and capital expenditure, the random component of the error is greater than the systematic component (i.e. it is greater than 0.5). More precisely, the random error for these components are 0.62, 0.85, 0.54, 0.60 and 0.59, respectively.

A disaggregated level analysis of revenue receipts, shows significant “systematic errors” in the own tax revenue projections in Kerala. In the non-tax revenue component, the systemic errors (0.49) in grants were found as high as the random errors (0.50). On the expenditure side, the errors in the social sector expenditure were found to have both systematic bias (0.45) and random errors (0.55). This might be the reflection of the adjustments in the State budgets in the social sector despite projecting high in Budget Estimate phase. The capital expenditure also incurred systematic errors (0.41) and random errors (0.59).

Ruzel Shrestha and this author in a paper published by NIPFP has estimated the fiscal forecasting errors with respect to Revised Estimates (RE) and Actuals, and the broad inference is that the proportion of error due to random component has been significantly higher than the systematic bias for all the macro-fiscal variables in Kerala, except for grants, own revenue (both own tax and own non-tax) and capital expenditure. This has policy implications as volatility in intergovernmental fiscal transfers can affect the stability of sub-national public finances.

Identifying innovative sources of financing the deficit is significant to maintain the high human development achievements of the state and also the growth-inducing capital infrastructure formation in Kerala.

(The writer is Professor, NIPFP. Views are personal)