More than a year after the defaults at IL&FS, not too many Non Banking Financial Companies (NBFC) and Housing Finance Companies (HFCs) can be said to be in good health. With access to credit constrained, a couple of them have defaulted, and some remain vulnerable to a default. Given this, it is surprising that an asset quality review, much like it was done for banks by Reserve Bank of India (RBI) in the last quarter of 2015, has not been done for NBFCs.

Between them, they owe banks a packet—about 50% of their loans are sourced from banks—so, it is important they stay solvent. The ones more vulnerable to a default are those that have big exposures to real estate developers; the financial condition of India’s tier II builders is no secret. Most NBFCs appear to be adequately capitalised, but credit quality apart, there are instances of fraud and violations, which make it harder for the banks to recover their money. Resolution has evaded lenders to DHFL for almost a year now, and, with an SFIO probe into the diversion of funds being considered, it is anyone’s guess how soon banks will see their Rs 38,000 crore.

What has done in non-bank lenders is the lack of liquidity support. This is probably hurting as much as the poor exposures. Altico Capital, for instance, wasn’t very highly leveraged when it found it wasn’t able to meet some of its obligations. In the absence of access to short-term liquidity from mutual funds, NBFCs and HFCs today are seriously constrained for cash. While it is nobody’s case that these lenders should be bailed out—they shouldn’t because it would create a moral hazard—RBI and government need to step in and find a way out. Let the government support stronger state-owned lenders—with capital in the form of bonds perhaps—to help them take over the NBFCs and HFCs. Should private sector lenders want to buy out the businesses, the process should be speeded up. Some quick consolidation is needed, else, even the good loans on their books could go bad, and the capital would be wasted. CRISIL wrote on October 24 that NPAs in the wholesale loan books of non-banks are tipped to rise in the near to medium term as the moratoria lapse. The wholesale book of non-banks is close to `4 lakh crore. Even if half of this goes bad, the system will get a big shock. This warning must be heeded. As as we have seen with DHFL and HDIL, recovering the loans will not be easy.

Simultaneously, there needs to be a lot more urgency in putting stressed real estate projects into the hands of stronger builders so that these can be completed; homebuyers who make a nuisance of themselves need to be dealt with firmly. The turnaround in the real estate sector is the key to the revival of the economy, and the sooner the staggering four or five lakh units of inventory are disposed of, the better. The government’s scheme to support projects that are 60% complete and are non-NPAs needs to be tweaked. The stressed projects need to be supported and handed over to stronger builders.

An analysis by Jefferies reveals that the commercial real-estate segment exposure of 36 banks to developers fell 8% y-o-y in FY19 over FY18 while the last four-year CAGR has been a mere 6.6% y-o-y. That’s good news, but the exposure at the end of March 2019, was nonetheless close to Rs 3.4 lakh crore—not be sneezed at.

To be sure, not every developer is a potential defaulter, but large-scale default cannot be ruled out, and neither can action by the investigative agencies.

The fact is banks, especially state-owned banks, aren’t out of the woods given the NPA cycle doesn’t seem to be ending anytime soon. Sectors such as power, telecom, and real estate continue to be pain points, apart from MSMEs and agriculture. While they may have some capital, the rising number of corporate defaults suggests they are going to need much more than they had probably. Without capital, it is going to be difficult to lend.

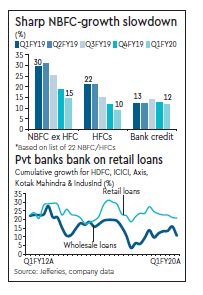

Already, loan growth at banks has been decelerating sharply over the past couple of months, when it was 14-15% y-o-y, and went below 9% y-o-y in the fortnight to October 11 because banks become so risk averse. They are choosing to lend only to top tier firms, and this has resulted in the spread of AAA bonds over the G-Sec narrowing. Meanwhile, the spread of the lowest-investment grade bonds over the AAA-rated bonds has now widened almost to levels last seen in 2008-09.

It is going to be hard, if not altogether impossible, to revive growth without freer flow of credit. Already, we seem to be getting into a vicious cycle where slowing loan growth—as seen in Q2FY20—could exacerbate the pain in industry, making lenders even more risk averse than they are today. SBI’s corporate book grew just 2% y-o-y in the September quarter. The government can persuade the state-owned banks to lend to the mid-micro-mini corporates, but their appetite will be limited; unless they are forced to, which of course is possible, it is unlikely they will risk exposure to weaker entities. And, if they take some hits on NBFC or HFC loans, they would end up short of capital, too. The DHFL resolution has taken way too much time, and threatens to remain elusive. There can’t be another DHFL.