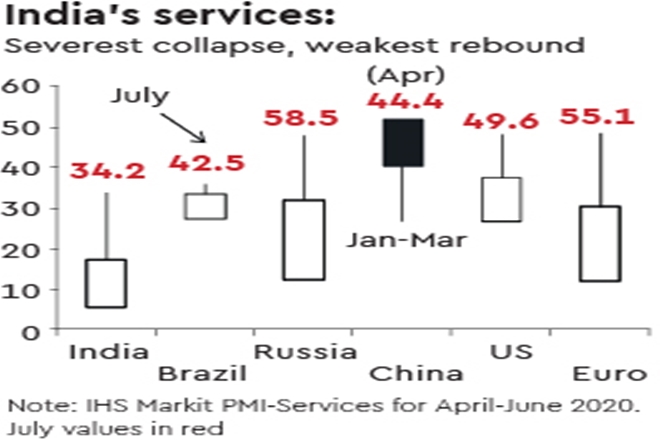

India’s services activity barely improved in July at 34.2 points from 33.7 in June according to the Purchasing Managers Index-Services (Nikkei/IHS). The weakness from April onwards compares very poorly with stronger performances elsewhere—in either the peak pandemic quarter or upon unlocking, and with countries with near similar infection paths. Brazil and the US, where infections are rising like in India, have observed lesser declines for example, with stronger unlocking rebounds; the falls and pick-ups in services of other countries too are nowhere as steep or weak as India’s. The intense, persistent contraction in services is deeply worrying. It requires greater policy attention taking serious note of the Covid-19 crisis’ unique composition, which affects services more than other sectors. For India, this could be a big problem as much of the output originates from services.

A coarse, PMI-based global comparison of services performance in April-July (China—January-April) illustrates how India’s services stand out as one of the worst-hit by the Covid-19 crisis. India had one of the steepest falls in the world in April (5.4) with a full national lockdown; the unlocking rebounds too are the weakest compared to the strong resurgence observed elsewhere, with some countries back into expansion territory.

The reasons for the weakness in services, although the PMI may be an incomplete or a narrow measure of the whole sector, are not hard to identify. If virus infections aren’t fully suppressed or rising, public fears about contagion remain entrenched; so do containment restrictions that are harsher for most services.

Consumers fear to venture out to crowded public places or avail contact-intensive services, holding back a large part of consumption. Services segments such as mass public transport, travel, tourism, hospitality, restaurants, recreation, education, and numerous social and personal services are disproportionately affected by Covid-19 crisis than say, the financial crisis in 2008.

A major reason why India’s PMIs reflect the deepest shrinkage globally is the stronger policy support in other countries: that in the US and Eurozone have been the most generous and explain the robust comeback in services, but all other emerging markets (EMs) have also increased public spending far more. In contrast, India has been trapped by the absence of fiscal space. Differences in fiscal responses and the relatively harder impact of Covid-19 crisis upon services are the two probable explanations for the deep contraction in India’s services.

That said, should the government worry about this depressing evolution?

It should as the negative output impact from such deep and persistent decline in services could be brutal in a stretching pandemic. A tipping point in infection growth rates is yet not visible, indicating that containment measures and safety fears will likely keep most services’ activities below potential for quite some time. Indicators of mobility, fuel demand, amongst others, also display some co-movement with infection outbreaks as well as lower activities than pre-Covid levels.

Last year, growth of services or half of India’s aggregate output, dropped sharply by 2.2 percentage points from the previous year (FY19); excluding government (public administration, defence and other services or PADO), the decline was as much as 3.1 points, with 4.1% growth (FY20). The fall is understated, or the slowdown more pronounced, because PADO includes ‘other services’ not covered elsewhere. Think of services like human health, sporting, recreational and sporting activities, hairdressing and other beauty treatment, private household employment, custom tailoring, and many more such not falling into the THTC or FRP groups (‘Trade, hotels, transport, communication and broadcasting-related services’, and ‘Financial, real estate & professional services’ respectively).

What would be the drag upon production and consumption if the disproportionate, harder impact of this crisis upon services persists without support? On the supply-side, overall services contributed above 70% or 3.06 percentage points to 3.9% real GVA growth in FY20; ex-PADO addition was 1.7 percentage points, but adjusted for ‘other services’ this would be higher. The vulnerability of consumption demand can be inferred from employment effects gauged by the proportion of urban workers (as MGNREGA support is provided for the rural segment) engaged in services. This is not insignificant as the Periodic Labour Force Survey Report (PLFS, Annual, 2018-19) shows that in terms of their usual work status in 2018-19, a respective 25.2% and 14% of male and female urban workers were engaged in ‘trade, hotel and restaurant’ services; 22.3% of male and 45.6% female workers were engaged in ‘other services. In all, 59.7% of male and 63% of female urban workers were engaged in ‘trade, hotel and restaurant’, ‘transport storage and communications’ and ‘other services’.

Now, some of these service activities have returned, but may not have been restored to pre-Covid strengths. Some, but not all, of these can be provided remotely or through teleworking. Most of the poorer workers or low-paid jobs fall into this group, and therefore, are the most vulnerable to layoffs and pay cuts; moreover, many of the ‘other services’ are self-sourced employment in India. Recent cross-country research by the IMF shows that workers in hospitality, food, construction and transportation segments are at most risk.

At present, there isn’t much information about the extent of the fallout of Covid-19 crisis upon services, although there are some household surveys by non-government organisations, other private agencies and abundant distress reports of permanent or temporary closures of eateries, restaurants, other services outlets, etc. But, an aggregate picture remains elusive.

What can and should the government do under the circumstances?

For one, it must reassess its policy support framework and step-up fiscal response to the affected urban segment. The virus has travelled much since the Rs 20 trillion support package was announced. In this interval, there have been reports of a second-round fiscal response in the wings for a post-pandemic recovery, including by the government’s chief economic advisor. If that is the policy plan, it would be useful to advance it in the light of the changed infection dynamics that appears to be extracting a larger output cost than foreseen even a month ago. The government must also note that such support is only part of replacement demand to recoup some losses and not a stimulus.

Two, it is regrettable there has been no effort to estimate the employment effect of the Covid-19 crisis. This lapse should be urgently addressed. Recall that in 2008, the Labour Bureau initiated a series of quarterly quick employment surveys from January 2009—in less than a quarter from the advent of the crisis—to capture the employment impact of the economic slowdown in eight major industries. There is an existing model of innovative use of the expertise and experience of public agencies available. The government should now deploy it to estimate the employment effects of the Covid-19 crisis. This was not done after demonetisation, but such surveys should be done at least now for sectors most affected by the Covid-19 economic crisis.

The author is New Delhi based macroeconomist

Views are personal