For years, State Bank of India’s big numbers felt like declarations, not chapters. Profits could excite in isolation, asset quality could become stable for a quarter or two, yet markets seldom regarded any result as evidence of sustainability.

Each strong run was read as performance in the moment, not proof of a robust cycle.

That pattern broke in the December 2025 quarter.

In Q3 FY26, SBI had a net profit of ₹22,176 crore, up 13% YoY from ₹19,484 crore in the same quarter in FY2025, marking its highest quarterly profit ever.

But the impact was not the headline number.

It was the chronological sequence in which it came: sustained 15.44% YoY loan growth, deposit enlistment that helped to manage funding costs, and an asset-quality enhancement with few qualifiers and no dependency on one-off gains.

The market noticed. Shares jumped 6–7% to a fresh high on results day, outperforming broader indices.

This did not feel like a strategic bounce.

For the first time in several banking cycles, SBI’s size appeared to be working with its fundamentals.

What investors are now grappling with is not whether the bank can produce a big quarter; it clearly can, but whether this marks a testable shift in how SBI utilizes scale, and whether that change can continue beyond a single earnings season.

Credit growth came first — and it held

This quarter was not superficial, and the loan book expansion, was the first sign of it. State Bank of India’s domestic advances expanded to ₹39.90 lakh crore, translating into 15.44% YoY growth, while international gross advances grew 13.41% YoY to ₹6,93,332 crore.

At this scale, the numbers matter less as a percentage and more as intention. Large banks often slow down lending late in a cycle to safeguard asset quality or protect margins.

SBI did neither. It grew, and it grew firmly, even as credit metrics continued to expand. That performance marks a break from its earlier cycles.

Historically, SBI’s credit growth managed to speed up before asset quality steadied, driving clean-ups later.

In Q3 FY26, the order reversed. Growth followed repair. That is a subtle shift, but it is precisely the change investors wait for before re-rating a bank of this size.

Just as notably, this expansion was not protective. It was not propelled by refinancing, rollovers, or opportunistic short-term lending. It was a real incremental implementation, which is harder to support, and so more important as a signal.

Breadth, not a single growth lever

The components of growth counted as much as its speed. Retail lending continued to grow steadily, but the sharper push came from other industries and agriculture, where year-on-year growth stayed in the high-teens.

Corporate lending also picked up, but without overwhelming the product mix. No single segment ruled the balance sheet.

This shift matters because SBI’s past cycles often tilted too heavily on one engine at a time, large corporates in one phase, unsecured retail in another.

Concentration made growth look powerful until it didn’t. In the third quarter, the book extended across multiple vectors, easing the odds that pressure in one pocket would upset the whole trajectory.

For a bank of SBI’s footprint, distributed growth is not just safer, it is operationally challenging. It needs underwriting depth, local execution, and coordination between thousands of branches.

That SBI presented this extensiveness implies institutional alignment rather than opportunism.

Funding did not sabotage the story

Growth only matters if it is financed correctly. SBI’s deposits rose to ₹57 lakh crore, broadly keeping pace with loan expansion. This growth stopped the need for aggressive repricing or short-term wholesale funding.

The Current Account & Savings Account (CASA) ratio hovered near 39%, lower than peak levels, but still fundamentally strong for a bank of SBI’s scale. This is where SBI’s competitive lead silently reaffirms itself.

Private banks can grow sooner in pockets, but few can muster deposits at SBI’s pace without raising costs sharply. SBI’s funding profile allowed it to grow without squeezing margins, a critical distinction between growth that looks good on paper and growth that survives inspection.

The deposit behaviour also suggested something deeper: trust. Depositors did not move money on quarterly earnings; they reacted to the stability and brand confidence displayed.

The ability to expand deposits with credit is a sign that SBI’s franchise depth continues intact even as competition increases.

Asset quality improved, without theatrics

Asset quality did what it needed to do: improve silently. Gross NPAs fell to ₹73,637 crores (1.57% of assets) from ₹84,360 crores (2.07%) the year before. The net NPAs fell to ₹18,012 crores (0.39%) compared to ₹21,378 crores (0.53%) in Q3 FY25. [AC6]

Slippage ratio stayed 0.54%, and provision coverage (PCR) stayed above 75%, giving the balance sheet a way to absorb surprises without pulling down future earnings.

This is not the phase where asset quality impresses. It is the phase where it stops interfering with the story. For SBI, that difference matters.

Past recoveries were often disrupted by one-off stress events that made investors re-price risk continuously. Q3 FY26 showed no such disruption.

Certainty is underestimated until it disappears. This quarter reminded the market why its return matters.

Profits followed the balance sheet

When growth, funding, and asset quality line up, profits stop being shaky. That is why the ₹22,176 crore profit excluding exceptional items mattered.

It was not driven by exceptional treasury profits, write-backs, or favourable accounting. It was the natural output of a balance sheet working as intended.

This distinction is critical. SBI has delivered large profits before. What it has struggled with is proving to investors that those profits are repeatable across cycles.

Q3 FY26 did not solve that question permanently, but it eased the burden of proof.

Markets are far more tolerant of earnings instability when the fundamental mechanics are evident. This quarter made those mechanics easier to trust.

Why the stock moved, and why it wasn’t a trade

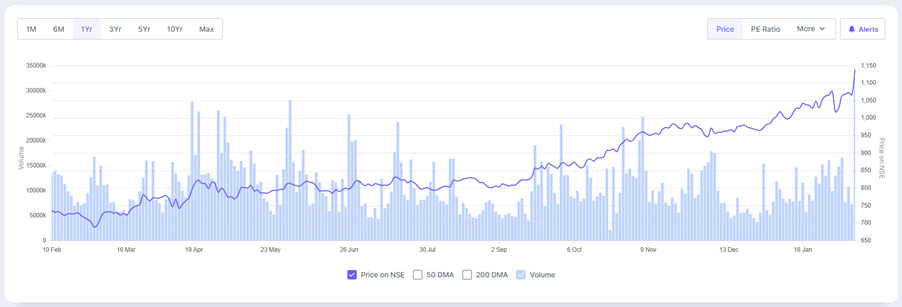

The 6–7% jump in SBI’s share price was not a momentum reaction. For a bank of this market capitalisation (₹10,55, 337 crore), such a move shows a change in outlook, not sentiment alone. The stock price grew 45% over the past year.

SBI 1-Year Share Price Trend

Investors were not reacting to upside surprise; they were responding to the probability that this earnings profile can continue.

This is the distinction between a rally and a re-rating. Rallies react to numbers. Re-ratings respond to stories that start to feel reliable.

The market’s reaction suggests SBI crossed a threshold, not into certainty, but into possibility.

That difference counts because it changes how future quarters are judged.

Strong numbers will now strengthen belief instead of interrupting uncertainty.

The industry cycle matters, but it doesn’t rationalise everything

The broader banking background is encouraging. System-wide credit growth has been running in the mid-teens, steered by retail demand, infrastructure spending, and a measured revival in private capital expenditure.

In such periods, even ordinary banks can post decent numbers. What separates SBI’s quarter is not its involvement in the cycle, but how it contributes to it.

Many banks grow fastest when the cycle turns loose. Few manage to grow while keeping their funding costs steady and credit quality improving. That is implementation, not macro.

The cycle explains opportunity. It does not explain control.

Scale is finally acting like an advantage

For years, SBI’s scale was a double-edged sword. It provided reach, but also slowed decision-making. It enabled deposit supremacy, but masked wastefulness.

In weaker phases, scale diluted liability. Q3 FY26 hinted at a change in this trend.

Scale began to expand strengths rather than soften limitations. Growth turned into profit without margin loss. Asset quality improved without giving up on growth.

That is what real scale is supposed to do, and what the market had stopped assuming SBI could still manage.

This is not a revolution. It is orientation. And alignment is often more valuable.

Where the real risks sit now

This is not a risk-free story, and they are no longer hidden.

Margin pressure is still the most important threat. As credit demand remains strong, deposit competition will increase. If funding costs rise faster than income, margins will compress, testing the sustainability of current profitability.

Asset quality is the second fault line. Agriculture and SME lending are still vulnerable to external shocks, weather, commodity prices, and regional disruptions. While provisions provide a buffer, slippages that mount across multiple subdivisions would instantly revive old doubts.

Execution risk is the silent but powerful risk. Growing at mid-teens on a growing loan book requires institutional stability. Systems, underwriting discipline, and regional oversight must scale perfectly. Optimism cannot replace the process.

What would actually break the narrative?

Two developments would significantly change how this story is read.

First, a persistent mismatch between loan growth and deposit growth will force SBI to chase expensive funding. That would weaken the margin stability that supports current confidence.

Second, a visible re-acceleration in slippages within multiple segments. One-off stress can always be rationalized. Broad-based stress cannot.

Absent these, the market will continue to give SBI the benefit of incremental belief.

The real test begins after the celebration

Q3 FY26 did not complete SBI’s progress. It re-framed it.

The bank has demonstrated that scale can now work with its fundamentals rather than obscure them. That is progress.

The next phase will be harder. Repetition always is.

Continuing growth without margin erosion, preserving asset quality without growth retreat, and doing both at scale is the real test of maturity.

This quarter did not answer every question.

But it changed the questions investors are asking.

And that, more than the profit number or the stock move, is why this quarter matters.

Disclaimer

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.