Welcome to the first edition of Dividend Hunter. In this series, we go deep into the numbers to find companies that have the potential to continue paying out a lucrative dividend in time to come.

For investors, dividend income is often a regular source of income. Dividend hunters look for companies that can pay sustainable dividends for years to come. Such companies are hard to find, but we can certainly try to estimate their future dividend-paying potential.

High-dividend-paying companies often have stable businesses, potentially strong cash flows, and, in many cases, a sign of management’s confidence in the business. In uncertain markets, these regular payouts serve as a steady anchor, providing returns even when stock prices fluctuate.

But not all dividend-paying stocks are created equal.

Some companies sustain high yields at the expense of future growth, while others establish a track record of consistent distributions supported by improving earnings. Even with lower base earnings, companies are generating high cash returns for shareholders.

For those seeking to balance income with reliability, a closer examination of select dividend plays becomes essential. In this context, we have selected this small-cap stock that can award a dividend in the upcoming quarters. This stock is selected using a screen that meets the following broad criteria. We have excluded InVITs and REITs in our selection.

- Dividend yield above 2%.

- Payout ratio below 100%.

- At least one of 3, 5, or 7-year profit growth above 5%.

- Five-year average dividend greater than zero.

- The latest dividend is higher than the five-year average.

- The latest profit is at least 80% of the previous year’s profit.

- Market capitalization above ₹1,000 crore.

The first company to meet these criteria is Alldigi Tech. At current prices, the company offers an exciting 7.3% dividend yield (based on historical payouts, of course).

Let’s dig into the company to see how the company is performing and whether that can give us any clues about future payouts.

Core Business: EXM and CXM Segments

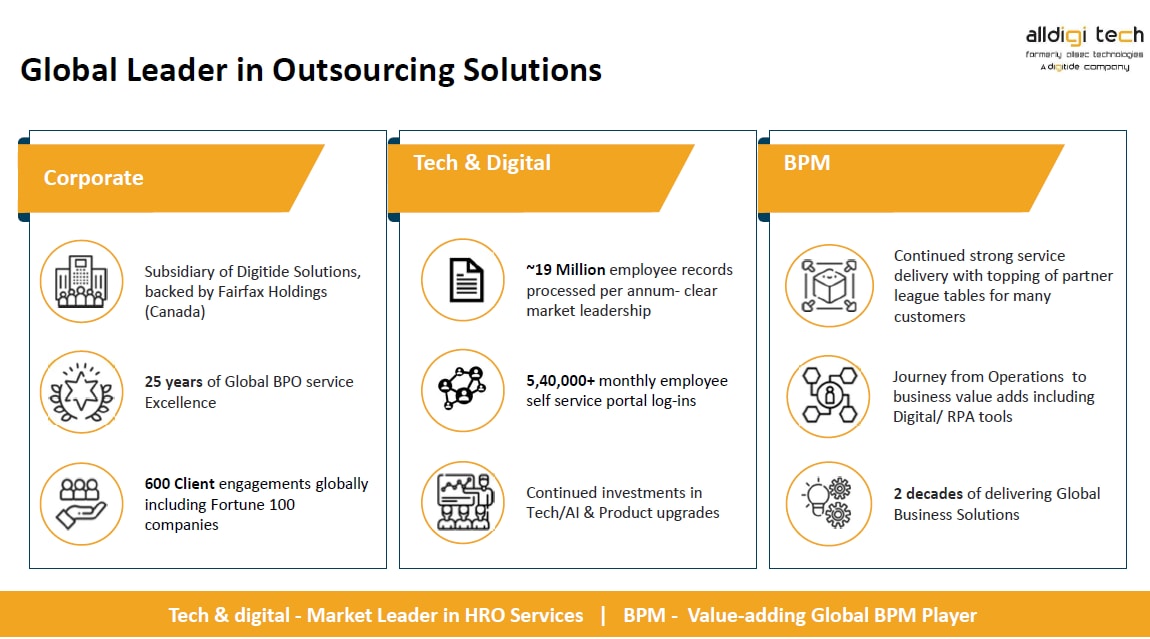

Alldigi Tech is a business process solutions company. Incorporated in 1998, it offers digital and technology-driven services across various industry verticals. It operates as a subsidiary of Digitide Solutions and is backed by Fairfax Holdings. Alldigi serves clients in up to 69 countries.

Global Footprint: Servicing 600+ Clients Across 69 Countries

Alldigi operates globally with two primary segments: Employee Experience (EXM) and Customer Experience Management (CXM). EXM provides Human Resource Management Systems, payroll, time-and-attendance management, and statutory compliance services.

Its flagship platforms include SmartHR (enterprise HR solutions), SmartPay (payroll delivery), Smart Stat (payroll compliance), and Buzzily (an HRMS for SMEs). It processes over 40 lakh payslips each quarter (around 14.5 to 16.2 lakh employee records per month) for more than 600 clients worldwide.

Alldigi Outsourcing Solutions Business

CXM services encompass lead generation, customer retention, back-office services, transaction processing, collections, fraud detection, and relationship management. This vertical serves BFSI (Banking, Financial Services, and Insurance), Retail, FGT (FMCG, Government, Telecom), and Healthcare sectors.

The CXM segment leverages Artificial Intelligence capabilities, including robotic process automation, chatbots, and omnichannel support, to enhance service delivery. Additionally, it recently integrated General Ledger accounting support for end-to-end financial reconciliation. CXM accounted for the majority of its revenue mix, 74.1%.

The Revenue and Net Profit Benchmark

The company’s market cap is ₹1,255 crore, as of 27 February 2026.

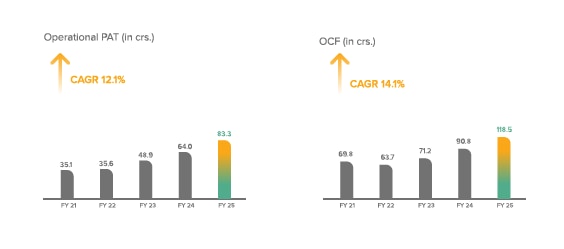

Over the last 3/5/10 years, net profit has grown at 27%/10%/21% CAGR. Recent numbers are also strong. Revenue rose by 16% year-on-year to ₹546 crore in FY25. EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) was 129.6 crore, with margin of 24%. Net profit was up 30% to ₹83.3 crore.

Net Profit and Operating Cash Flow Trend

In Q3FY26, the financials remained strong as well. Revenue rose by 9.5% year-on-year to ₹152.7 crore. EBITDA rose 41.7% to ₹45.9 crore, indicating strong operational efficiency. Margins expanded by 680 bps to 30.1%. Net profit was 4.5% higher at ₹20.8 crore.

The ₹168.7 Crore Cash and Cash Equivalents

The company generates strong operating cash flow, which supports its ability to pay dividends. Operating Cash Flow increased by 87.2% to ₹45.3 crore. Cash and liquid funds increased to ₹168.7 crore, driven by margin accruals and improved collections.

Dividend Sustainability: Beyond the 7.3% Yield

On the back of such cash flow, the company has already paid an interim dividend of ₹60 in FY26 year-to-date. This comprises ₹30, announced on 30 July 2025, and ₹30, announced on 28 January 2026. As I shared earlier, the dividend yield is 7.3% as per the current price of ₹824 per share.

Also, this dividend (₹60) is well above the 5-year average of ₹25.8 per share. Dividend payout ratio stands at 84%, remaining below the 100% threshold required by the screener. The company’s dividend-paying track record suggests the dividend could continue.

The 29.4% ROCE and 32.7% ROE Moat

Return on Capital Employed stands at 29.4% (up from 13.6% in FY24) and Return on Equity at 32.7% (up from 25.9%). The management attributed this growth to better margins generated by an increased share of international revenues and a laser-sharp focus on cost management.

The Growth Roadmap: AI-Driven Efficiency and Global Expansion

Future outlook further solidifies this assumption. The company aims to grow its top-line growth at mid-to-high teens. Specifically, management expects the EXM segment to maintain a high-teens CAGR, projecting that it could double the size of the EXM business over the next 4 to 5 years.

Alldigi aims to improve its EBITDA margins by 100 to 150 bps year-on-year. This expansion is expected to be driven by a three-tiered strategy. This includes increasing the share of higher-margin international revenues, improving operational efficiencies (such as the number of payroll records processed per employee), and maintaining tight control over indirect costs.

A core focus remains expanding the company’s global footprint, particularly in the USA, UK, and ANZ (Australia and New Zealand) through hybrid delivery models. Growing the proportion of international business across both its BPO and HR segments remains a primary objective.

The company is focusing on advancing platform intelligence. A major upcoming initiative is the utilization of PulseEXM.ai, an AI personal assistant deeply integrated into their EXM platforms. It aims to provide smart self-service and a unified employee experience.

Valuation: Is Alldigi Trading at a Discount to Peers?

Valuation-wise, Alldigi trades at a price-to-earnings multiple of 16.5X, a discount to the 5-year historical median of 20X. Relative to eClerx (22.6X) and Firstsource (21.4X), the valuation is at a discount.

Is Alldigi Tech a stock that Dividend Hunters should track?

Alldigi Tech meets the key Dividend Hunter filters, backed by steady profit growth, strong cash flows, and a payout ratio within limits. With a 7.3% yield and improving margins, dividend continuity looks reasonable.

However, sustainability will depend on earnings momentum and disciplined capital allocation going forward. Dividend hunters should add this stock to their watchlist and see if it conitnues to deliver what can only be described as a lucrative dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was unavailable have we used an alternative, widely used, and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.