Everyone in Indian markets knows the Bombay Stock Exchange (BSE).

Very few have ever stopped to ask what kind of business it actually is.

For most of its “listed” life, BSE was treated as a relic valued, measured, but strategically irrelevant. Trading volumes trailed while derivatives hardly had any takers.

Even as India’s equity markets expanded, BSE’s financial data failed to inspire belief.

In FY19, its revenues were still less than ₹900 crore, margins were uneven, and the exchange seemed stuck in the shadow of a far larger competitor.

That is why BSE’s present position feels practically counterintuitive.

Today, the same company produces over ₹1,807 crore in annual profits, operates with operating margins of 56% (trailing twelve months), and sits on over ₹7,583 crore of equity cash.

BSE did not reinvent itself. The market grew into it.

Understanding how that happened, and how far it can reasonably go from here, is what makes BSE a far more fascinating company than its familiarity implies.

Patience, Not Ambition Pays

Go back ten years, and BSE’s numbers told a very different story.

Revenues were modest. Profitability existed, but margins lacked momentum. Capital markets were growing, but the activity did not flow significantly through BSE’s platforms. From the outside, it looked like a business slowly moving into irrelevance.

But inside, something crucial was happening.

BSE continued to invest in infrastructure, trading systems, compliance, surveillance, and data platforms without overextending its balance sheet.

In general, it did not chase volumes through fee cuts (it did try to kickstart some of its businesses by offering attractive prices, though). It did not burn capital trying to obtain liquidity. It opted to stay operationally prepared, even when the utilisation was poor.

That decision looked cautious at the time. In hindsight, it was strategic.

The Market Matures to BSE’s Model

The inflection did not come from BSE transforming itself.

It came from India’s capital markets, growing quicker than expected.

After 2020, the retail participation in India surged. Derivatives activity grew exponentially. New listings accelerated.

And, suddenly, the infrastructure BSE had been sustaining for years began to see real throughput.

Here is where the numbers start to matter

Per Screener.in, between FY21 and FY25, BSE’s revenues rose from ₹630 crore to ₹3,212 crore. Even though impressive, an even more mindboggling shift was below the line.

Operating profit margins grew faster than revenue, pushing them from 32% in FY21 to 58% by FY25, while net profit crossed ₹1,800 crore on a trailing twelve-month basis.

In Q2 FY26, the revenue was ₹ 1,068 crore, while the net profit rose to ₹557 crore, excluding exceptional items.

This was not because BSE found a new product.

It was because the incremental activity stopped requiring additional investments from the company.

Earning Without Consumers

The most mistaken characteristic of BSE is who its customer really is. In general…

BSE does not sell to traders.

It does not market to investors.

It does not pay to acquire clients.

Its customer is the market itself.

Every trade executed on its platform, regardless of which broker initiates it, generates a fee. Every listed company pays compliance and listing charges. Data products and index services spawn continuous subscription-like income.

BSE has over 22.3 crore registered investors, while the total contracts traded in the equity derivatives were 114,100 crores between April and September 2025.

Per the latest company presentation, the average daily turnover in H1FY26 in derivatives was a massive ₹148 trillion.

The SME platform adds hundreds of companies that pay annual fees regardless of daily trading volumes.

This distinction explains why BSE’s earnings profile looks so different from brokerages or fintech platforms. Where others must continuously encourage activity, BSE handles what already exists.

Robust Revenue Mix

As volumes picked up, something else became clear in the financials.

BSE was no longer supported by transaction fees alone. In recent quarters, listing fees, annual compliance income, data and index services, and SME platform revenues together accounted for more than a third of total revenue, decreasing dependence on pure trading activity.

The SME platform, in particular, has crossed 600 listed companies, raising over ₹14,520 crore, creating a stream of recurring annual fees that does not change with daily market sentiment.

This is why BSE could report quarters where profits rose ~60% or more. The product mix had matured.

Cash Flows Tell the Real Story

If the income statement shows scale, the cash-flow statement shows its worth.

Over the past year, BSE generated strong operating cash flows, while capital expenditure remained limited to upkeep and system improvements.

As a result, free cash flows stayed strong, even after higher spending on technical tools.

This discipline reveals itself on the balance sheet. BSE carries no meaningful debt and holds ₹7,583 crore in equity-cash, giving it both strength and optionality.

These are not numbers related to companies struggling for relevance. They belong to businesses that have found their economic position.

Silent Shift: Understanding the Quiet Re-Rating

BSE’s sharp re-rating in the market is often credited to the retail boom.

That explanation is over-simplified.

The re-rating ensued because the market stopped treating BSE as a minor exchange and began respecting it as a market utility.

A business with anticipated cash flows, small execution risk, robust operating leverage, and slight capital intensity.

This shift is evident in valuation metrics.

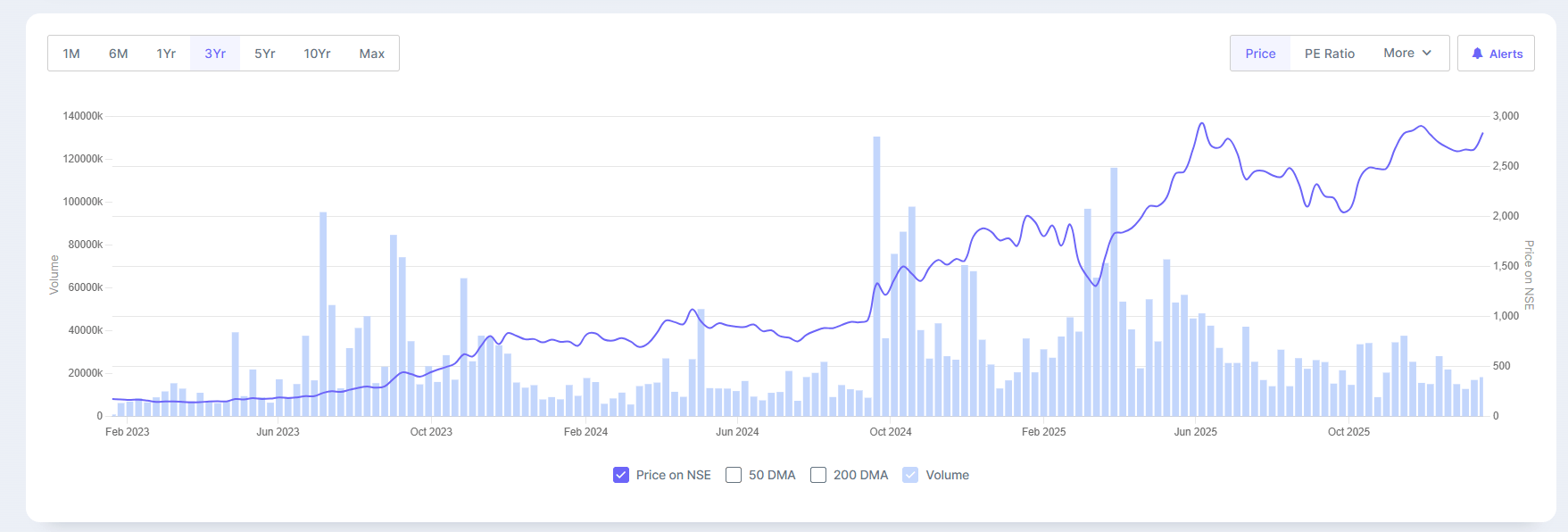

BSE now trades at a P/E multiple of 64.27x, at par with the industry median. The average return on equity over the last three years is 23%, while the profit grew at a compounded rate of 70%. The stock price grew at a CAGR of 152% during the same period.

BSE 3-Year Share Price Trend

BSE now trades at multiples that suggest stamina, not thrill. Investors are paying for earnings confidence, not for hyper-growth.

That also means the expectations are higher, while the tolerance for mistakes is lower.

Where the real risks lie

The risks around BSE are not extraordinary, but they are consequential.

The most immediate issue is the governance. Fee structures, particularly in derivatives, are not completely in the company’s control.

This was visible in 2024, when proposed policy changes prompted a sharp correction in the stock among estimates that incomes could take a mid-teens percentage hit if pricing flexibility tightened.

For a company with such high daily trade volumes, such interventions matter extremely.

Volume cyclicality is another. Transaction revenues still form a significant share of income, and extended periods of subdued market activity will affect topline growth. BSE’s consolidated transaction charges revenue in September 2025 was ₹794 crore.

The diversified revenue base, listings, transaction charges, service to corporates, treasury income on C&S funds, compliance income, data, investment income, and SME fees cushion the impact, but do not remove it.

Competition, especially in derivatives, remains fundamental rather than existential. BSE does not need to lead to continue its economics, but it must remain relevant.

Losing importance in high-margin segments would modify the earnings profile far more than short-term volume swings.

These risks do not threaten BSE’s survival.

They threaten the certainty premium the market currently assigns to it.

How much further can this go?

The easy gains in BSE’s story are behind it.

The operating leverage has done its job. The costs have normalised, and margins have expanded to levels that show maturity rather than acceleration. From here, growth will come, but it will be stable and less exciting.

It is where BSE’s personality matters.

Future performance will rest less on capturing market share and more on retaining discipline, safeguarding margins, expanding non-transaction income, and resisting the appeal of chasing volumes through pricing or incentives.

The moment incremental growth requires incremental spending is when the model will start taking on a different form.

In other words, BSE’s next phase will be defined by control, not ambition.

From Relevance to Constraints

BSE is no longer a turnaround story or a relevance story. That debate is settled.

It is now a market utility, a business that earns from investor participation without needing to manufacture it, transforms activity into cash with limited capital, and carries a balance-sheet strength that few financial companies can match.

The market has recognised this shift. Valuations already exhibit stability, consistency, and high returns on capital. What they do not leave much room for is dissatisfaction.

For investors, the question is no longer whether BSE works as a business.

It clearly does.

The real question is whether the company can preserve the characteristics that brought it here: cost discipline, revenue mix stability, and regulatory relevance, at a point when expectations are high, and margins are already rich.

That is not a trader’s question.

It is the kind of question long-term investors ask when a company moves from being undervalued to being fully understood.

And that is precisely where BSE now stands.

Interesting factoid: NSE will listing on the BSE shortly.

SEBI chief Tuhin Kanta Pandey on 16th January this year, said, “The no objection certificate for the NSE IPO may be given later this month.”

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.