")

India’s organised fashion retail growth has a familiar hero: Trent.

This Tata Group retailer has become the market’s favourite consumer story over the past few years, largely driven by the explosive growth of its value-fashion brand, Zudio.

With hundreds of new stores opening every year and strong same-store sales growth, Trent has emerged as one of the most obvious recipients of India’s post-pandemic consumption recovery.

But under the limelight that tracks Trent lies a silent story unfolding through the country.

Among Tier-2 and Tier-3 cities, a few regional retailers are progressively expanding store networks, improving balance sheets, and operating margins.

Many of them run on lower costs, have effective regional brand recall, and an innate understanding of local spending patterns.

Among the most notable examples are Cantabil Retail India and Sai Silks (Kalamandir), companies that are scaling swiftly but aren’t as well-known as their larger peers.

Yet the question most investors now have is simple: could the next Trent arise from these regional chains instead of national?

The Trent Standard: Why Zudio changed India’s fashion retail

To know why local retailers are getting attention, it is important to see why Trent has worked so well.

Trent’s Zudio stores solved a crucial retail equation: fashion at exceptionally affordable prices provided through strictly controlled supply cycles.

Unlike established apparel chains that trade with high design complexities and high inventory risk, Zudio focuses on limited seasonal collections, quick inventory turnover, low store fit-out costs, and is present in high-footfall value retail hubs.

The result has been remarkable for a fashion retailer.

This low-cost model produced strong store finances as the network expanded, and, more significantly, showed that organised value fashion could scale commercially far beyond India’s metros.

That realisation substantially broadened the identified growth runway for apparel retail, creating a compelling tailwind for regional chains that were already operational in these markets.

The Tier-II & III Consumption Boom

India’s consumption story is moving beyond the country’s largest metros.

For decades, organised retail expansion was concentrated in cities like Mumbai, Delhi, Bengaluru, and Hyderabad. But over the past five years, demand growth has increasingly moved toward Tier-II and Tier-III markets.

Several fundamental factors are leading this shift.

First, rising incomes in smaller cities, due to infrastructure spending, manufacturing clusters, and services growth, are increasing discretionary expenditure.

Second, retail infrastructure is improving swiftly. New shopping malls, retail streets, and high-footfall business complexes are appearing across cities like Indore, Surat, Lucknow, Coimbatore, and Vizag.

Third, digital exposure is restructuring consumer behaviour. Social media and e-commerce have accelerated the understanding of fashion, driving the demand for branded clothing even in smaller towns.

For fashion retailers, this combination creates a smart equation: expanding demand with controllable operating costs.

The Economics Behind Fashion Retail

Fashion retail can be highly lucrative, but only if the economics work.

Successful chains tend to optimise three key variables:

1. Inventory turnover: Fashion inventory quickly loses value if it remains unsold. Retailers with constant design refresh cycles and tighter supply chains usually sustain healthier margins.

2. Store productivity: The revenue per square foot determines if the growth turns into profitability.

3. Private label sourcing: Retailers with robust private-label brands maintain higher gross margins and pricing control.

Trent’s Zudio format proved how powerful these economics can be when executed at scale. These same philosophies are now being employed by smaller regional chains.

Cantabil Retail India: Building a value fashion network

Cantabil Retail India has spent the past two decades creating a presence in the reasonably-priced fashion segment, targeting middle-income buyers in smaller cities.

The company operates hundreds of stores across India, offering men’s wear, women’s wear, and accessories under its own brands.

Cantabil’s growth plan focuses on growing its store footprint while keeping strong inventory control.

Over the past few years, the company has firmly increased store count while improving operating margins.

A franchise-led store increase that lowers capital requirements, a sharp focus on Tier-II and Tier-III cities, and a wide product portfolio within price segments are the key drivers behind the company’s expansion.

Financial performance has also improved, besides expansion.

For Q3 FY26, Cantabil’s revenue was ~₹264 crore, up ~19% YoY, while net profit grew ~31% YoY to ~₹45 crore excluding exceptional items.

Operating leverage has played a key role. The earnings before interest, taxes, depreciation, and amortisation (EBITDA) for the quarter increased to ₹95 crore, with margins increasing 36% YoY.

These numbers were aided by larger ticket sizes during the winter season and disciplined operating costs.

Equally important are the operational metrics.

Cantabil now operates around 646 stores across India, with management continuing to focus on expansion in smaller cities where rental costs are still convenient.

As per the latest investor presentation, the average bill value for 9M FY26 was ₹4,387 compared to ₹4,017 for 9M FY25, while the volume grew ~14.80% during the same period, implying that current stores continue to see steady growth in demand.

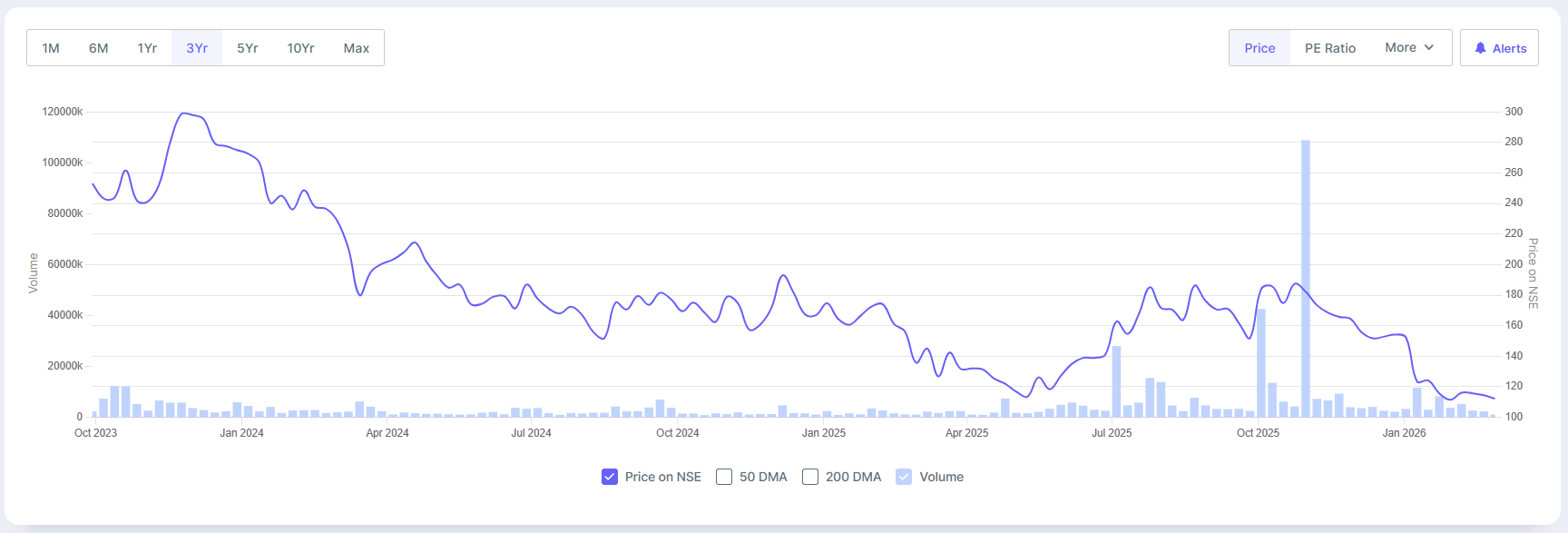

The average return on equity over the past three years was 21%, while the stock price grew at a CAGR of 11% during the same period.

Cantabil 3-Year Stock Price Trend

For a retailer focused essentially on Tier-II markets, those numbers show a business that is growing without losing store productivity.

For investors, the company signifies a scaled but still under-researched mid-cap retail story.

Sai Silks (Kalamandir): Leveraging the wedding economy

While Cantabil focuses on daily fashion, Sai Silks (Kalamandir) works in a different segment of India’s clothing market, ethnic wear and wedding fashion. It is one of the largest clothing retailers offering premium ethnic and value fashion in Southern India.

The company runs multiple brands, including:

- Kalamandir

- Mandir

- Kanchipuram Varamahalakshmi Silks

- KLM Fashion Mall

- Valli Silks

The business is built around a simple but compelling demand driver: India’s wedding economy.

Traditional wear remains fundamental to wedding celebrations across much of the country, guaranteeing constant demand for silk sarees and festive apparel.

Sai Silks has reacted by focusing on large-format stores that offer large bridal collections.

The company had a revenue of ₹411 crore in Q3 FY26, falling 8.32% YoY compared to the same quarter the year before. The consolidated net profit declined ~17% YoY to ~₹38 crore, excluding exceptional items.

While the quarterly revenue and profits declined slightly year-on-year, partially due to festival timing changes and softer footfalls, the 9M FY26 revenue rose~16% YoY to ~₹1,235 crore.

The growth indicated continuous demand regardless of quarterly volatility. This position has supported strong revenue growth in recent years. The company is present in 22 cities with 79 stores.

The average return on equity over the past three years was 13%. However, the stock price fell 23.8% during the same period (253 in Oct 23 to 112 in Feb 26).

Sai Silks 3-Year Share Price Trend

The Indian wedding economy, estimated to be worth billions annually, offers a comparatively steady demand base for such retailers.

As organised retail penetration increases in cultural wear, companies like Sai Silks are projected to benefit from the change away from unorganised neighbourhood stores.

Trent vs Regional chains

However, the scale of difference between Trent and regional retailers is still significant, but the underlying growth drivers are similar.

Retail comparison snapshot

| Company | Q3 FY26 Revenue | Business Focus |

| Trent Ltd. | ₹5,345 crore | National value fashion (Zudio, Westside) |

| Cantabil Retail | ₹264 crore | Affordable apparel chain |

| Sai Silks (Kalamandir) | ₹411 crore | Ethnic & wedding fashion |

While Trent operates at a much larger scale, regional chains often grow faster in their central markets because they understand local demand patterns more deeply.

For investors, this trend raises an important question: can regional chains in time replicate Trent’s scaling trajectory?

Why Regional Chains Often Succeed in Smaller Cities

Regional clothing retailers often function with a different playbook from national chains.

Instead of rapid nationwide expansion, they usually build dense store clusters within specific regions.

Doing so allows them create a stronger brand recognition while keeping logistics and supply chains manageable. Local retailers also tend to identify regional demand cycles better, from wedding seasons and festival calendars to differences in fashion preferences across states.

This expertise offers operational benefits like low marketing costs, improved stock planning, and a structured expansion plan.

In an industry where inventory mistakes can mean lower margins, such knowledge can make a lot of difference.

The Risks Behind Fashion Retail Growth

Despite the growth opportunity, apparel retail is still complex.

Fashion trends change quickly, forcing store owners to refresh collections all the time. Unsold inventory means discounting, which can eventually reduce profit margins.

Moreover, the demand tends to change around festive and wedding cycles. Even a change in festival timings can affect the sales momentum.

Competition is another factor. Large retailers are supported by strong supply chains and large marketing budgets, which may not be the case with regional players.

However, if regional retailers wish to dominate the market, then maintaining differentiation through pricing, product selection, or local brand equity will be crucial.

A retail industry entering its next phase

India’s organised retail sector is still rather young compared to global markets.

Despite rapid growth over the past decade, organised players still account for a minority share of the country’s overall clothing market, which is still ruled by unorganised retailers and local stores.

But that balance is gradually moving.

Rising incomes, urbanisation, and the spread of modern retail infrastructure are steadily pushing consumers toward organised formats.

Boston Consulting Group and the Retailers Association India’s latest report shows the Indian apparel retail market is poised to grow to ₹200 trillion over the next decade.

National brands will undoubtedly remain central to that expansion.

Yet the next phase of growth may also bring a different set of winners, companies that build scale within regional markets before expanding outward.

Retail history in India has often followed this pattern. Some of the country’s largest consumer businesses began as regional brands before evolving into national players.

Today’s regional retailers may be following a similar trajectory.

Most investors are left wondering: As India’s retail boom spreads beyond the metros, will the next big retail success story come from a national giant, or from a regional player silently building scale where the market isn’t yet looking?

Even as this story unfolds, consider adding these stocks to your watchlist to keep a track on India’s fast growing regional retailers.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling and, in particular, investor education. In a previous assignment, at Equentis Wealth Advisory, she led innovation and communication initiatives. Here she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.