More non-banking finance companies (NBFCs) are likely to pursue co-lending partnerships going ahead, in a bid to grow their balance sheets at a time when these entities are expected to post a double-digit growth in credit in 2022-23 (April-March).

“While NBFCs’ assets will grow in double-digit levels in the medium term, their balance sheets may not grow to that extent on account of the asset-light business strategy that a number of NBFCs plan to follow,” Krishnan Sitaraman, senior director and deputy chief ratings officer, Crisil Ratings, said.

“In this strategy, mechanisms like co-lending and assignments are expected to increase, especially for medium and small-sized NBFCs,” Sitaraman added.

This need for these partnerships also arises from the fact that the sustained demand for credit brings risks on the asset quality front.

Additionally, these partnerships can provide a boost to non-bank lenders’ liquidity as unlike banks, most NBFCs are not permitted to raise public deposits, say bankers.

At a recent event, Godrej Capital MD & CEO Manish Shah highlighted that the non-banking financial sector needs to relook at underwriting credit not just by sharing key borrower data but also by sharing credit risks.

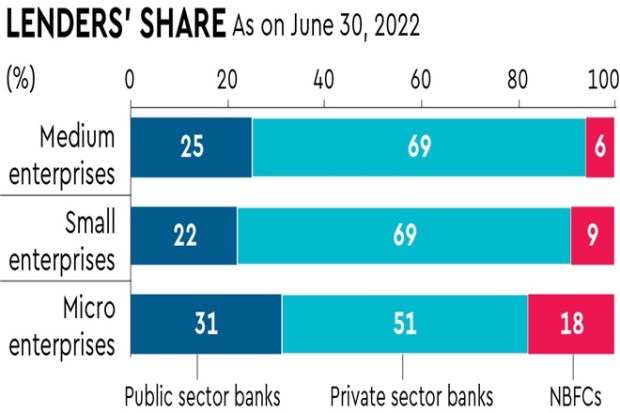

In fact, a recent KPMG report showed that NBFCs’ outstanding credit to the default-prone micro, small and medium-sized enterprises(MSME) sector stood at Rs 3.6 trillion on June 30.

In such a scenario, co-lending partnerships with banks can help non-bank lenders manage their assets and liabilities better, say experts.

Also read: Axis Bank eyes rural pie; ICICI Bank, HDFC Bank lead

Typically, a co-lending partnership is an 80:20 arrangement wherein 80% of the loan would be booked on the bank’s balance sheet, whereas the remaining 20% would be booked on the NBFC’s balance sheet.

The borrower would pay interest at a weighted average lending rate, which is lower than the interest rate of a typical NBFC loan.

The non-bank lender originates the loan and makes collections of the same on a monthly basis for a servicing fee paid by the bank. Here, the NBFC is cushioned from the impact of a loan default as a majority of the loan exposure in borne by the bank.

Also, these partnerships help non-bank lenders preserve capital as they will not be required to provide capital for the portion of that loan that would be on the books of the partner bank. This is a key benefit, given that the borrowing costs of NBFCs are expected remain high going ahead.

“It (co-lending partnerships) will aid in assets and liability management. It allows NBFCs to earn differential interest, which increases their profitability and strengthens their balance sheet,” Kishore Lodha, chief financial officer, U GRO Capital, said.

On the other hand, these partnerships enable banks to save on operating expenditure and help them grow their loan books at a faster pace, a senior director at a credit rating agency said.

Due to the benefits, co-lending pacts between banks and non-bank lenders are frequent.

Also read: Regulatory forbearance offered to IDBI Bank buyer

In March, India’s largest lender State Bank of India (SBI) announced co-lending agreements with five housing financiers including PNB Housing Finance and IIFL Home Finance.

In fact, SBI has also inked co-lending agreements with U Gro Capital and Capri Global Capital in order to lend to MSMEs.

In December 2021, U GRO Capital MD & CEO Shachindra Nath told FE in an interaction that co-lending volumes will likely hit Rs 30,000 crore by the end of 2022-23.

But the onus under these arrangements falls on originator non-bank lenders to ensure that the asset quality of the co-lending loan pool does not deteriorate, say experts.

“While co-lending is primarily a risk-sharing model in which each partner shares risk in the agreed-upon portfolio ratio, NBFCs should be aware that lenders will be closely monitoring the portfolio behaviour of the co-lending pool,” Lodha said.

“If any of the partners’ pool performance falls short of expectations, large lenders will be hesitant to do additional co-lending through those partners.”