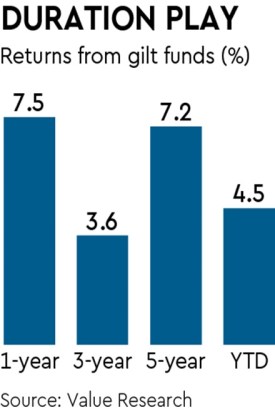

As gilt funds have started looking attractive, investors are gradually betting on them for higher long-term returns. In the six months to June this year, these funds have reported net inflows of Rs 5,530 crore as compared with net outflows of Rs 1,254 crore during the same period last year.

Gilt funds are a type of debt mutual fund schemes that invest in government securities issued by the central and state governments of varying maturities. They do not have credit risk but carry interest rate risks. Yields on the longer end are attractive for long-term allocators and investors with suitable profiles can gradually start building such duration exposure to also benefit from the interest rate reversal cycle.

Nirav Karkera, head of research, Fisdom, says gilt funds have started looking attractive for longer term allocators considering the elevated yields offered. “As we move closer towards the expected terminal rates and expect a stretched pause in the rate regime, now may be a good time for investors to capitalise on the duration play offered by gilt funds. While there are inflows, the quantum reflects a cautious approach as investors attempt to allocate towards the longer end gradually,” he says.

Similarly, Sonam Srivastava, founder, Wright Research, an investment advisory firm, says it is a good time to start investing in gilt funds as the interest rate is expected to remain stable or even decline in the coming months, which will make gilt funds more attractive to investors. “However, it is important to remember that gilt funds are not immune to interest rate risk. If the interest rate were to rise sharply, the NAV of a gilt fund would fall. Therefore, it is important to invest in gilt funds with a long-term horizon and to diversify your portfolio with other asset classes,” she says.

Look before you leap

Investors must understand that while credit risk is relatively on the lower side in gilt funds, there is a fair deal of interest rate risk and any adverse turn in the interest rate regime could affect returns negatively. Investors must also look at the duration of the fund, the expense ratio and the track record of the fund.

Gilt funds typically are most lucrative when interest rates have room to decline significantly providing opportunities for capital gains. Vivek Banka, co-founder, GoalTeller, a financial advisory firm, says a lot of investors look at gilt funds considering the fact that there is no credit risk and then presume that at any point of time they would be accruing a minimum return totally discounting the tenor and interest rate movements. “Gilt funds need to be examined and understood carefully before making an investment, especially the impact of interest rate hikes on the fund returns,” he says.

Investors with a short-term investment horizon should consider short-term maturity gilt funds. These funds are less sensitive to interest rate changes than long-term maturity gilt funds. However, they also offer lower returns. “If you have a long-term investment horizon, you may want to consider long-term maturity gilt funds. These funds offer higher returns, but they are also more sensitive to interest rate changes,” says Srivastava.

A better alternative

Dynamic bond funds are a good option for retail investors who want to invest in gilt funds but do not want to worry about managing their portfolios. They are open-ended schemes that invest across durations and have a flexibility to invest in short-term instruments such as commercial paper and certificates of deposit, or medium to long-term instruments such as corporate bonds and gilt securities.

These funds automatically adjust their asset allocation based on the market conditions. As a result, investors do not have to worry about whether they are invested in the right type of gilt fund and the investment horizon. “Retail investors with limited access to insights on the interest rate regime and know-how required to align investment strategies with such insights are better off investing with a credible dynamic bond fund. This way the investor stands to gain from fund management expertise across cycles,” says Karkera.

DEPENDABLE BET

* Gilt funds typically are most lucrative when interest rates have room to decline significantly providing opportunities for capital gains

* Investors with a short-term investment horizon should consider short-term maturity gilt funds

* Dynamic bond funds are a good option for retail investors