By A K Verma

The reduction in power demand during the Covid-19 lockdown explains that the demand of power depends largely on the level of socioeconomic activities. Meeting the full demand would be a function of available generation, access to load centre and also the health of electricity distribution companies (discoms). India had a total generating capacity of about 368 gigawatts (GW) as on January 2020, whereas the maximum peak demand reached so far was around 183GW. The renewable energy capacity has also doubled over the last five years—to become almost 23% of the installed capacity of utilities—even though electricity generated from renewable energy sources is still only 9%, due to the low capacity utilisation factor (CUF) of about 14-15%.

The current extent of flexibilisation in conventional thermal plants cannot efficiently make up for variability induced by must-run renewable energy plants. As a result, discoms have done more power purchase agreements (PPAs) than required, and now end up paying excess fixed charges. The problem has further been compounded by the current downside in consumption and peak load due to the lockdown. The comparison of peaks of certain dates shows that the peak load was growing compared to the previous year demand, but started to reduce from the day of the Janta Curfew (see graphic).

The system of aggregate demand projection has not been robust in the country. The aggregate power demand is directly connected with the growth rate of the gross domestic product (GDP). The GDP growth rate of 8-10% was used in demand projection of the 18th Electric Power Survey (EPS; 2012-17) and, consequently, actual demand remained much below the projected one. Income elasticity of electricity demand is found higher in the relatively less-developed eastern region, leading to higher growth in electricity demand with increasing income. Relatively slower growth in electricity demand has been observed in developed states, i.e. industrialised states, although in absolute value they are quite high.

The impact of Covid-19 on power demand would be better understood once the lockdown is lifted. If industrial activities in developed states suffer from reverse migration of workforce, and the public consumption does not pick up in developing states due to deprivation of domestic remittance, then it may affect demand adversely. It would, therefore, be desirable to hasten industrial production in developed states and ensure adequate income to strengthen consumption in developing states.

Demand estimates of 19th EPS (2017-22) also face great challenges and may go haywire in the wake of global slowdown and Covid-19. Energy-efficiency schemes such as solarisation of agri-pumps, Perform, Achieve and Trade (PAT) for designated industries, LED bulb campaign, and the Standards and Labelling programme (Star rating) are likely to reduce electricity demand on the grid.

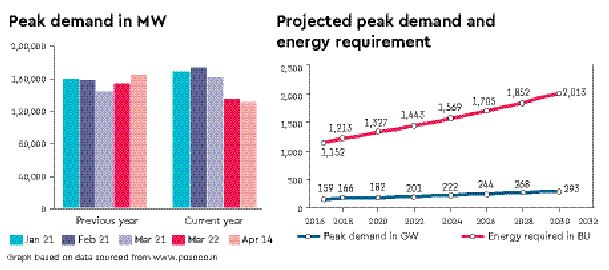

According to Energy Outlook 2020 of the International Energy Agency (IEA), India avoided an additional 15% of annual energy demand and 300 million tonnes of carbon dioxide emissions due energy efficiency efforts during 2000-18. These are consumer and climate-friendly activities and must continue. The demand for electricity is also influenced by season, rainfall, population growth, climatic variations, technological changes, consumer preferences, availability of alternative energy sources, etc. Schemes such as Make in India, Dedicated Freight Corridor, FAME, and so on are likely to increase electricity consumption and should be implemented faster. On a conservative estimate, the Central Electricity Authority (CEA) has projected peak demand to be 201GW and 293GW in 2022 and 2030, respectively. So, a mid-course-correction in power demand would be necessary in the aftermath of the Covid-19 crisis.

Generation planning in the country has also not conformed to international best practices. Review and enforcement of resource planning have been missing at the tariff regulation stage, too. Generation capacity in the country stands much above the expected peak demand. The IEA recommends reserve margin of 15%, but reserve margin in India has been as high as 50.94% in 2011-12 and 71.78% in March 2017. It now stands at 100%. Renewable energy installation target of 175GW is expected to be met, nevertheless it may not generate more than 225-250 BU (billion units) by 2021-22 due to low CUF (capacity utilisation factor), but new demand for long-term procurement of conventional power is unlikely to rise in the near future, unless old and inefficient plants are retired.

The problem of plenty was unknown to the power sector in India. Post-2014, all pending projects were expedited and India could add more than 100GW capacity in three years. With surplus installed capacity, India needs to accelerate electric cooking, electric mobility and electrification of railways. They may add up to consumption of additional 200 BU of electricity. India is now committed to 450GW of renewables. We must, therefore, search new opportunities of cost-effective storage technology, diversified usages and overseas trade of electricity to utilise full capacity.

Tax concession for establishing MSMEs in identified pockets can enhance demand as well as remove regional inequality and create local employment. The Covid-19 crisis should be leveraged as an opportunity for introducing tariff reforms. Rationalisation of industrial and commercial tariff; reducing cross-subsidy regime in coal, railways and power sector; introduction of demand-linked tariff slabs; preferential tariff to energy-intensive industries; introduction of time and type of use tariff; and incentivising electric vehicles through lower tariffs can boost power demand and resolve the dilemma.

(The author is ex-joint secretary, Ministry of Power. Views are personal)