By Divakar Vijayasarathy

A shrinking GDP, ending moratorium and a spreading pandemic—a perfect recipe for large-scale chaos especially in a country already struggling with a falling growth rate and burgeoning public debt. Amidst this setting, there was a need for a framework to delay the inevitable, large-scale bad loans (NPAs). Every sector was crying for help, while the most affected one (banking) was considered to have the moral obligation to bail out businesses oblivious of their fiduciary responsibility towards small depositors and shareholders.

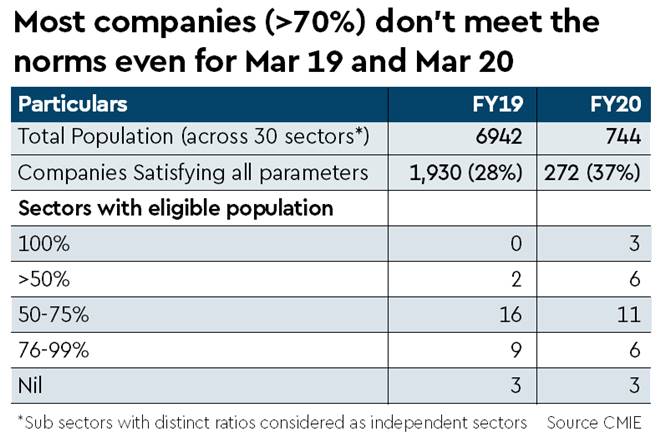

The KV Kamath Committee was thus formed. It did a commendable job with a resolution proposal in just 28 days. However, what was recommended as an indicative framework giving businesses time till March 2023 and bank boards some discretion came out as a fixed norm from RBI with literally no flexibility for banks. To put things into perspective, borrowers across 26 affected sectors should achieve five specified ratios by March 2022 to be eligible for restructuring. An analysis shows why this may not solve the problem but partially defer it till March 2022 (see graphics):

Classification of the sectors was broad-based: For instance, all auto ancillaries were grouped under one head without cognisance of the industry they catered to. While the tractor industry thrived, CVs had their worst time in decades. Deepak Reddy, MD, Nelcast, states, “Tractor business is bullish, we should close with 8% YoY growth with just 10 months of effective operations.” However, Arjun Parthasarathy, director, Metal Forms, adds “CV business is down 70% and for the first time in decades we are staring at a cash loss.”

Multiple businesses with diverse models have been clubbed as a single sector: Hotels, restaurants and tourism have been blended with common parameters, disregarding their distinct investment, scale and payback periods. Manav Goel, director, Adyar Gate Hotels, claims, “Occupancy rates are sub-20% and we expect another 18-24 months to normalcy. It’s impossible to achieve the ratios by March 2022 and the sector requires at least a five-year window for restructuring.”

Hotels are a real estate play and should have ideally been treated at par with commercial real estate.

Pooling businesses of all sizes under the same category: Commercial real estate was deemed to be hit the hardest with work from home continuing even post-Covid-19. In reality, the blue-chip clientele of Grade A spaces have been paying rents even during the lockdown, while those severely hit are the malls and Grade B/C properties.

Chandrakant Kankaria, director, Olympia Group, states, “Our collections are 98% on Grade A spaces; however, malls and smaller offices have been struggling.” Considering all the categories with a single yardstick does not benefit the really affected.

Impact of state-specific lockdowns has been ignored by adopting a uniform approach for the entire country: While it’s impossible to predict all contingencies, an accommodative framework providing for discretion would have addressed the issue.

Though the intention behind the circular is laudable, the outcome may not solve the problem for most. Business projections must show extraordinary growth to achieve the benchmarks by March 2022; for the sake of immediate resolution, however, banks should brace up for a larger NPA crisis by March 2022. Manickam Mahalingam, MD, Sakthi Sugars, adds, “The ratios are not possible for most of the sugar sector, except may be for the top few companies. Given the nature of our industry, we cannot even give optimistic projections.” Hari Thiagarajan, chairman, CII-TN, opines, “SME borrowers are yet to fully understand the ramifications, which is why trade associations have not raised their concerns vociferously.”

RBI would have done well to have accepted the recommendations of the committee, in both letter and spirit, by giving flexibility to bank boards to take well-informed, documented and micro-sector-specific decisions, instead of a one-size-fits-most guideline.

The author is founder & managing partner, DVS Advisors LLP