By Sharad Kumar

The pandemic has spoilt the plan’s for this year and burnt a hole in the pockets of many. The otherwise festive season of the year has turned into a period of negative growth and pessimism. Although many analysts are pessimistic about India’s growth prospects and economic outlook, I remain an optimist.

As has been the case with many other economic downturns, India will surely return stronger. However, this may bring in a behavioural change in the minds of consumers, entrepreneurs and investors. Businesses have used this period to redefine strategies, bring a change in processes, diversify products and even brainstorm over revamping their systems and procedures with an eye on the future.

A 2018 HBR paper says, ‘two great forces are transforming the very nature of work: automation and ever fiercer global competition. To keep up, many organisations have had to rethink their workforce strategies, often making changes that are disruptive and painful.’

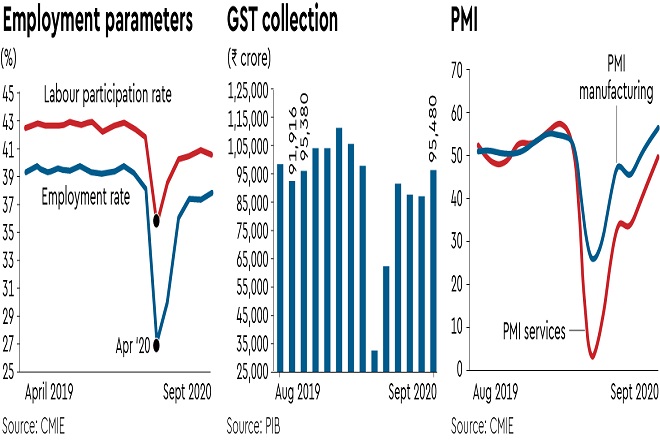

While companies are heading towards automation, the concept of “lean operations” still stands out. Toyota remains the most revered example of this. Business leaders annually tour Toyota’s facilities to gather insights on lean production and learn the hows of adopting operational and organisational innovations. However, what is worrying is how the majority defines ‘lean’. Is it that businesses, instead of focusing on ‘difficult but doable’ raising of operational efficiency through ‘lean,’ are looking at the convenient option of reducing the labour force or attendant costs? A CMIE report says, “If this proportion (of the labour force that is represented by the labour force participation rate) keeps falling as it evidently is, it does not bode well for India’s growth story. It renders all stories of a revival in the economy as a myth”. It highlights that urban India saw a shrinking of labour force and employment in September.

Consider a business operating at full capacity coming close to shutting down suddenly. With increasing demand, full capacity may get restored, but with lesser labour. If, on the pretext of turning lean, lay-offs, cuts, etc, happen, things turn sour for many.As per a survey by Manpower Group, hiring sentiment in India is the weakest in 15 years; only 3% of firms are looking to hire and only 7% anticipate an increase in payrolls in the next three months. Indian employers are among those who were the least optimistic globally about bringing back all furloughed workers.

The doom rhetoric becomes more painful when improving numbers give you a sense of recovery. Auto sales have improved, GST revenue is up, the majority of industrial units have resumed operations, railway freight collection has increased, exports have grown by 5%, and power consumption is improving. Manufacturing PMI is at its best since January 2012, and the service PMI at 49.8 is also at its best in the last five months. Though not a complete recovery, it may be construed as a start. Labour, an important factor of production, deserves to be part of the revival journey.

In this recovery-oriented environment, why are the employment numbers not giving a concrete recovery statement and why are surveys not indicating a return of employment. It is time that businesses also contribute and drive up demand. We need to remember that eventually, it is the employment-driven income that creates demand and allows the production cycle of the economy to move faster.

(Kumar is Head, Economic Research Function, Bajaj Finance Ltd. Views are personal)